Israel – Under the Radar

How Israel has ranked at #2

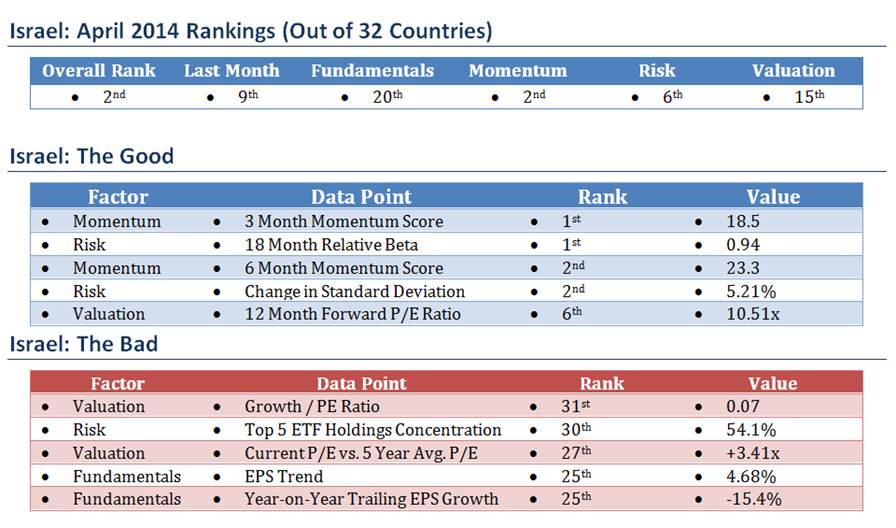

In recent travels and presentations, I was asked frequently about Israel. How is it that the Israeli market is #2 in our country ranking methodology? It seems as though the country is off the radar screen of most investors, so a quick overview of the market and why it ranks high currently seems to be in order.

Israel is a developed market. It constitutes only a 0.19% weight in the All Country World Index (ACWI) and is also part of EAFE at 0.52%. With these tiny weights, it is no surprise that the country is not in most investor’s playbooks. The Israeli market is mature and diversified, however, with the Israel MSCI Index being comprised of 24% banks, 24% pharma, 13% telecom, with other sectors below 10%. Teva Pharmaceuticals and Bank Hapoalim are the two largest positions in the Index. There are two Israel ETFs – EIS and ISRA. iShares’ EIS tracks the MSCI Israel Index which fits our methodology best and is larger in terms of assets. Since the June 2013 launch of ISRA, EIS has a fractionally higher return which may or may not be important. At least we know that the “Bluestar Israel Global Index” used in the Market Vectors implementation has produced similar results.

We recently traded approximately 480,000 shares in one block, $23 million in a single print. That represented 10x ADV (average daily volume) and 20% of the current shares outstanding. We were able to buy the block 5 cents inside the ask price and 10 bps above the then-current INAV (intraday net asset value). As we often say, there are no ETFs that benefit more from the wrapper than the single-country roster. There is no way to own Israel in such a diversified, low cost, easily-executed way except through an ETF; and to execute it for size inside the bid/ask spread with no market impact is exemplary.

But, back to the question as to why we own Israel in the first place. Some highlights from our country ranking model are presented below. Overall, the Israeli market could be characterized as fundamentally solid, fairly valued, with strong momentum, and reduced risk headwinds.

Israel’s economic growth has been resilient even amid a period of weak global trade expansion. The 3.3% 2013 number should be replicated in 2014 and 2015.* The country has seen a strong start to major natural gas production. As production expands it will moderately continue to contribute to growth. Even larger fields are expected to come online in 2018, providing another significant boost to GDP.

Exports have been volatile, but are outperforming in a difficult global environment. Israel exports are up 3% while global trade volumes have actually declined by 2.5% over the same three year period.* The Current Account is in surplus and is growing with more momentum likely as natural gas production expands. The country has seen FX reserves triple since 2008. Government debt ratios and fiscal deficits have declined.

The main risk to the country may be the potential strengthening of the currency which would diminish some of the competitive advantages currently in place. The Bank of Israel, however, has been highly aggressive with its monetary policy, lowering base rates 180bp over 18 months to 0.75% as well as intervening in the FX market and creating a sovereign wealth fund.* Inflation pressures remain very low and considerable flexibility is still afforded to the BoI.

Of course there are geo-political issues in Israel. The current cabinet remains split on what caused the recent breakdown of Palestinian-Israeli peace talks. Clearly some are committed to peace talks while others aren’t. Ongoing issues are likely in Israel as we all can imagine. “Event risk” is always present when investing in individual countries. There may be more likelihood of such events in Israel than other countries, but nothing currently causes us to back away from the other positives specifically related to the financial markets. And, as has been the case for ten years, we will reevaluate all of these factors every month. To the extent that there are changes that cause Israel to be less attractive or other countries whose profile improves in a relative sense to give us a more attractive opportunity, there can be moves in our rankings and portfolio allocations. Please check back often to our blog for updates on all of these issues.

Disclosures:

The opinions expressed in this report are those of the author. The materials and commentary are strictly informational and should be used for research use only. This brochure should not be construed as advertising material. The opinions expressed are not intended to provide investing or other advice or guidance with respect to the matters addressed in this brochure. All relevant facts, including individual circumstances, need to be considered by the reader to arrive at investment conclusions to comply with matters addressed in this brochure. Past performance is not indicative of future results. Remember that investing involves risks, as the value of your investment will fluctuate over time and you may gain or lose money. Investment risks are born solely by the investor and not by Accuvest Global Advisors (AGA). AGA is an independent investment advisor registered with the SEC. All disclosures, marketing brochures, and supplemental firm sheets are available upon request.

Charts and information used in this report are sourced from AGA. Commentary marked by “*” are sourced from Barclays, UBS, and Bloomberg, respectively.

(c) AdvisorShares