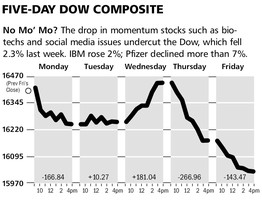

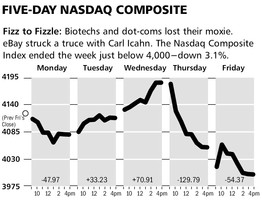

Stocks fell last week upset by the growth sectors of biotechnology and social media stocks. Energy issues and related infrastructure were largely unaffected. It is clear that hedge funds and others have become forced sellers as their macro bets on being long growth areas, but being short the bond market have blown up in their faces. Until this settles down the overall market is likely to continue its correction.

As the charts above illustrate both the Dow Jones Industrial Average and the NASDAQ Composite had rough weeks. The former dropped 2.4% while the latter lost 3.1%,

led by the previously best performing sectors.

The Markets & Economy

Early last week the markets rallied as the Federal Reserve minutes from their last meeting were released.

· The members tried their best to convince the markets that the economy is, at best, only ok and

· That Yellen misspoke a month ago when she implied the Federal Open Market Committee would move faster than expected to raise interest rates.

As you will appreciate from reading these weekly updates, the economy was never in danger of growing so fast as to make the FED move quicker to normalize policy. In fact, all of the evidence continues to point to another blasé year of economic growth. The first quarter, in fact, is likely to show just a 1% annual growth rate. Dreams of a 3% year will soon disappear and be replaced by a bullish growth forecast for 2015. It is a ritual which is too boring for words, but is now getting ready for its 5th year of acting out.

In Europe it is even more ludicrous to think in terms of growth. Over the weekend, the Chairman of the ECB stated bluntly that deflation is the problem and the central bank will act in even more aggressive terms. Many think this is a forecast of their own version of “Quantitative Easing”. Since it didn’t work here in America, why not try it in Europe?

The sad fact remains that global growth is not in the cards. Avoiding a step down to a no-growth economy is the risk and always has been. So far there is no evidence of that in the USA. Growth here will go on as our country’s growing energy independence is providing support to the economy. In Europe, stability is about all they can hope for. All one has to do is look at their record low borrowing rates to realize there is no near-term prospect for recovery there.

In fact, Europe’s interest rates are so low that it is a growing factor which limits any upward movement that rates can have in the USA. After all, if basket case countries such as Italy & Spain can borrow at yields less than here at home, then I will be knocked over with a feather.

What to Expect This Week

This will be a holiday shortened trading week. The stock market is closed on Friday in observance of Good Friday.

Earnings reports will pick up their pace this week, but really for us nothing is on the horizon for the next few days.

Thus, we are left with the unknown. What is going on in the Ukraine? When will the forced selling in the high growth names cease? How is the economy doing in April?

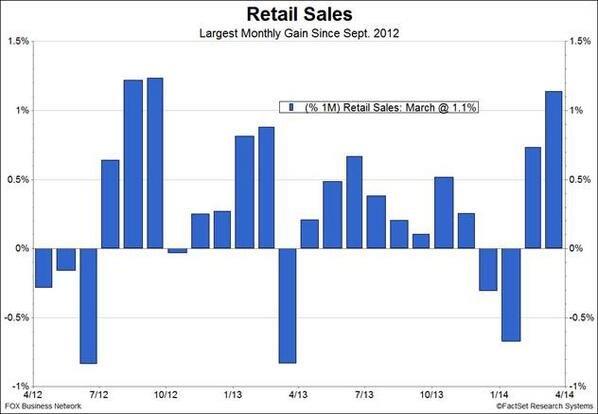

On this last question, the data is encouraging (within the parameters of a 2% growth economy). This morning’s retail sales report (see chart next page) showed a nice rebound in March led by the auto sector. The problem with this of course is that auto sales are being financed increasingly to the sub-prime sector over time frames up to 7 years. These financings are not likely to end well, but for now the coast is clear. Just read the news (that is sarcasm of course).

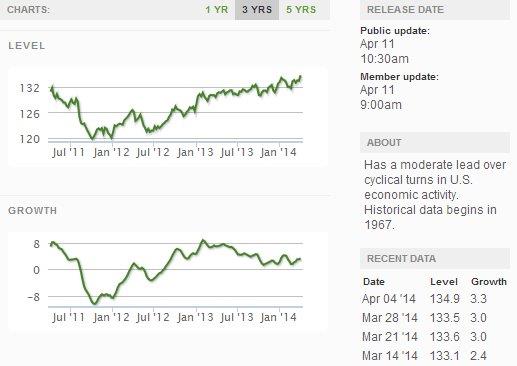

Finally, the weekly look at the leading economic indicators from the Economic Cycle Research Institute showed a pop this week, so perhaps the winter is finally ending here in North America.

My next Commentary update will be in two weeks.

By then we should have some of our own earnings reports to update for you.

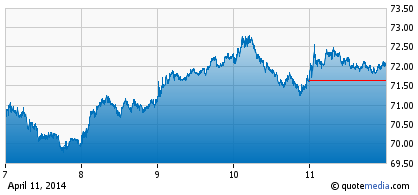

SYMBOL: EPD

Shares of ENTERPRISE PRODUCTS PARTNERS L.P. bucked the market trend last week hitting an all-time high, with strong performance which is continuing this morning. The energy services provider hiked its quarterly cash distribution to $0.71 cents, $2.84 per share on an annualized basis.

This is EPD’s 39th consecutive quarterly increase.

With the uncertainties in Ukraine and Russia helping to boost the energy sector here, we continue to view EPD as a powerful holding for our clients given its string of organic growth projects, potential acquisitions, strong balance sheet and solid liquidity position.

With its diverse set of natural gas, crude oil and refined products, the partnership possesses fundamental strengths which should continue to support distribution growth. ENTERPRISE reports quarterly earnings on May 1st.

The fact that EPD’s dividend yield is now below 4%, is a testament to its well-run operations in the L.P. space. Consequently, we would not be surprised if the board considers authorizing a secondary stock offering at these levels.