US Treasury yields registered their largest weekly drop since early February, driven by dovish minutes from the March Federal Reserve Open Market Committee meeting and equity market weakness. With the technology stocks at the epicenter of the equity storm, major indices fell nearly 3% last week. As Q1 earning season begins in earnest this week, equity performance is very much expected to remain in the headlines. Reaching yields last seen in early March, five year notes were the best performer across the Treasury curve, falling 12 basis points on the week to yield 1.58%.

Commentary from members of the Federal Reserve has been meaningful in shaping market direction in recent weeks, as they attempt to clarify the timing of their first interest rate hike and the economic thresholds that would need to be achieved in order to do so. We will likely be offered more insight this week (and potentially higher volatility), as Chair Janet Yellen is scheduled to make two high profile public appearances—notably, her address to the Economic Club of New York on Wednesday.

Additionally, this week offers two important pieces of data on the economic front: retail sales and the consumer price index (CPI). The retail report will be particularly important for the market, as participants look for signs that weary consumers have begun to pull themselves out of the winter vortex.

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

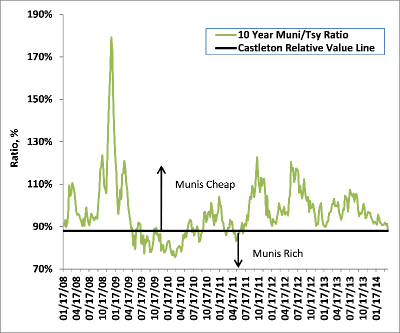

Ratio of 10Y Municipal Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

Taking direction from forces outside of the municipal market, primarily lower Treasury rates and weaker equities, municipals once again were able to produce strong price gains and falling yields. Continuing a yearlong theme of modest supply and steady demand, intermediate tax free rates fell another 13 basis points last week, to yield a 2.33%. Ten year high grade municipals are now at their lowest level of 2014 and the lowest at any point since last June.

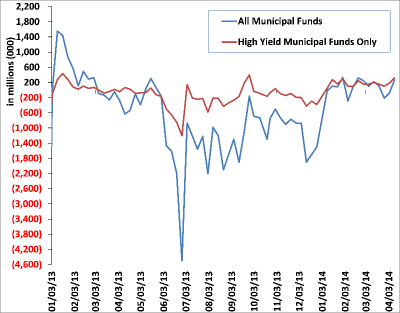

With tax season upon us, demand for tax exempts has been steadily rising over the last several weeks, as investors recognize both munis’ superior tax adjusted yields relative to comparably rated taxable alternatives, and the muted volatility relative to equity investments. Mutual fund flows rebounded sharply last week, rising to +$274 million. One area of the muni market that continues to show outsized demand is high yield tax free funds. With an additional +$323 million of new money last week, high yield funds have now recorded 14 consecutive weeks of positive fund flows—bringing the year to date total to over +$2.1 billion.

Strong relative performance in tax exempts is expected to continue, as less than $2b of new debt is expected to price in a holiday-shortened week. A $320 million loan for the State of North Carolina (AAA) and a $200 million loan for the Massachusetts Bay Transportation Authority (AAA) headline this week’s issues.

Municipal Credit News & Notes:

- California : owing to higher income and capital gains taxes, the state controller announced that California has taken in +$1.4 billion more than budgeted in taxes so far in FY2014.

- Detroit : the City reached a settlement with the monoline insurers regarding the $388 million in outstanding unlimited tax general obligation bonds (ULTGO). The City has agreed to pay the insurers 74 cents on the dollar—a substantial increase from the prior offer of 15 cents. Recognizing a long and protracted litigation process, all parties have agreed to the settlement. As part of the settlement, the City will file with the bankruptcy court that ULTGO bonds have a lien on the pledged ad valorem taxes and that the levy constitutes special revenue.

- New Jersey : Standard & Poors (S&P) downgraded the credit rating of the State of New Jersey to A+ from AA-, citing ongoing budget strain—even as revenues recover from the great recession and super storm Sandy. New Jersey’s recent economic performance is providing insufficient support to meet the growing demands of its long term pension liabilities.

- U.S. States : showing improved financial performance, the Census Bureau announced last week that states took in 6.1% more revenue in fiscal 2013 than fiscal 2012—the third consecutive yearly increase. Revenue increased in all states except Alaska and Wyoming. North Dakota, California, Hawaii, and Colorado registered the largest yearly percentage increases.

- Puerto Rico : budgeted revenues through the first 9 months of this fiscal year exceed plan by +$86 million, or 4.6%.

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

In rather impressive fashion, high grade bond spreads were able to contract another 1-2 basis points last week, despite stock indices selling off sharply. Corporate debt continues to outperform equities year-to-date. More notable however, is how well spreads have performed relative to US Treasuries, especially since intermediate Treasury yields have declined nearly 40bp so far in 2014.

With earnings season underway, issuance was relatively light last week, as most companies are in a “black out” period. With another +$1.7 billion of new cash hitting taxable funds last week, technicals remain favorable for investment grade spreads. Despite such favorable tailwinds in corporate bonds, we reiterate our caution, believing the rapid reduction in credit spreads over the last 6 months—particularly inside of 5 years—has made credit expensive and vulnerable to a rise in interest rates.

© 2014 Castleton Partners, LLC. All rights reserved.

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.