Why the U.S. Should Export Crude Oil

The Ukraine-Russia crisis, as well as Russia’s position as a major energy provider, has renewed the discussion on whether the US should export crude oil. A forty year old decree bans U.S. producers from exporting crude oil, and it needs to be repealed. It represents misguided protectionism and is a hangover from the days before the US embraced free trade. We think that exporting crude oil would be an economic benefit to the US, as it incentivises the full development of the US shale resource.

The 1973 Oil Embargo by several Arab Nations reduced oil imports into major consuming countries and caused oil prices to more than triple between 1972 and 1974. As a result, in 1975 a ban on crude oil exports was put in place by US Congress as one of the measures to reduce US exposure to global crude markets. Despite the measures, U.S. oil imports rose fivefold in the subsequent years to over 10 million(m) barrels(b)/day of crude oil today, making the U.S. the world’s largest oil importer.

Almost forty years after the oil export ban was enacted, the energy landscape has changed dramatically. In the last few years, US domestic oil production has increased to over 8m b/day, and is likely to exceed 11m b/day by the end of the decade, as a result of the development of shale oil. Oil imports have fallen sharply as a result of greater production of crude oil from the new shale plays and weaker US demand. This rapid turnaround has caused the price of US domestic light sweet crude oils (such as West Texas Intermediate, or WTI) to trade at a discount to international crude oils (such as Brent), and has raised the question of whether the U.S. should repeal the export ban and start exporting crude oil in order to defend domestic crude oil prices.

Despite importing nearly 8m b/day of oil, there is a strong case for exporting some of the rapidly growing light sweet crude oil supplies while continuing to import the medium crudes best suited for existing refineries.

There are many different types of crude oil. Broadly speaking, crude oil is often referred to as being ‘light’ or ‘heavy’ (depending on its density), as well as being ‘sweet’ or ‘sour’ (reflecting the level of sulphur it contains). The new crude oil being produced from the shale developments is entirely ‘light’ and ‘sweet’, similar in quality to Brent crude oil (a light sweet blend of crude oil traded in the North Sea), West Texas Intermediate (the light sweet oil traded at Cushing, Oklahoma) or Louisiana Light Sweet (LLS – the light sweet crude oil traded at the US Gulf Coast in Louisiana).

As the U.S. produces more light sweet crude oil, it needs to import less of that blend. At current growth rates, we project seeing domestic production of light sweet crude oil to exceed refinery demand at some point during 2014. As the U.S. is importing nearly 8m b/day of various crude oil blends, as required by the configuration of its refining capacity, the country has found itself oversupplied with light sweet crude oil, which is why we think the U.S. needs to start exporting.

Exporting crude could make a substantial difference to the future of the US energy market.

If crude oil is exported, WTI prices could potentially rise to meet global crude oil benchmarks. Additionally, the US oil industry would be better positioned to generate the cash flow needed to reinvest in oil production and develop the full potential of U.S. oil shale, which in turn could create new jobs.

We believe the U.S. ought to address this issue immediately. The WTI forward oil price in 2020 is only $77/barrel, ostensibly because the likely crude oil saturation in the country. At that price level, many of the non-core US oil shale plays would be marginal in economic terms and existing producers could not generate the necessary cash flow to reinvest and fully develop their acreage.

The US refining system is not set up to refine a higher volume of light sweet crude oil.

The US has the biggest refining capacity in the world. Like crude oils, every refinery is slightly different and has been constructed to handle a specific blend of crude oil. The US refining system has been upgraded significantly over the last decade to improve its ability to consume heavy and sour crude oil anticipated from Canada, Mexico and Venezuela. Many of these refiners are now making adjustments to their equipment to maximize their intake of the cheaper light, sweet WTI oil. However, many years and billions of dollars would be needed to make the wholesale changes required to consume the volume of light sweet oil that the US could produce. So, while the US refining system is running at full capacity and is exporting record levels of oil products to international markets, it is not configured to reap the maximum benefits of the shale boom.

If it is not refined or exported, US crude oil must either be consumed or stockpiled.

Quite simply, the excess light sweet crude will go into storage if it is not exported, refined or consumed. We expect some of the excess light oil volumes to be consumed as a result of refinery configuration changes (as much as 1m b/day over the next three years) or potentially exported in small quantities with one-off export licenses, but these will be small in the context of increasing light sweet oil production from the US over the next few years. Ultimately, inventories of light sweet crude oil could start to build in 2015, even if growth in domestic demand slows the inventory build rate.

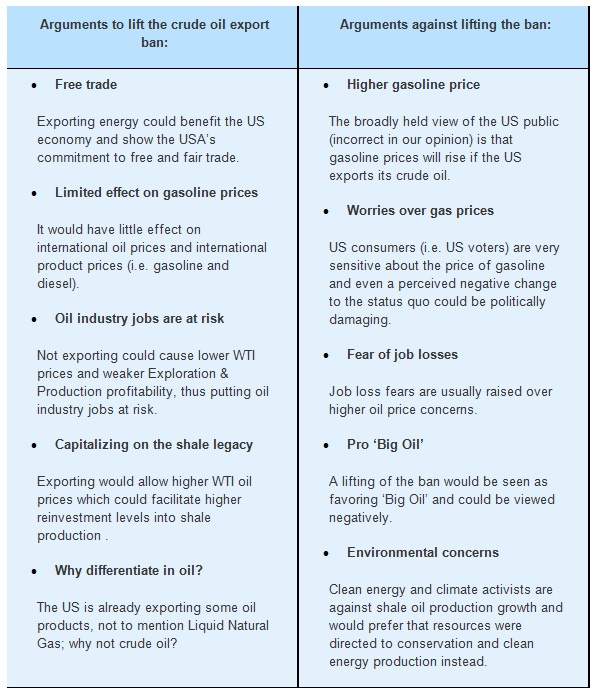

We believe that the export ban should be lifted.

Economic logic dictates that the ban should be lifted. However, political considerations will play a prominent role in this decision. In our opinion, the key point in this debate is that there is a closer correlation between US domestic gasoline prices and Brent oil prices than there is between US domestic gasoline prices and WTI oil prices. While US public opinion is that oil exports will cause higher gasoline prices, we believe that exporting as much as 1 million barrels a day of US crude oil into the global oil market of around 90 million barrels per day could temper Brent oil prices and therefore US gasoline prices.

Whether or not the ban is lifted, we expect to see a steady adjustment by the oil industry and lawmakers to relieve pressure in the system, until a time when it is politically palatable to lift the ban. Small scale one-off export approvals have started to occur, and we anticipate seeing more of them.

The issue is also gaining momentum in Congress, and the export ban could even be repealed by the President without Congressional approval, as long as it is deemed to be ‘in the national interest’.

The repeal of the export ban will be a hot topic in 2014, and we have high confidence that the correct action will be taken to ensure that the US fully develops its windfall of shale oil and that the US economy will benefit accordingly in terms of employment and balance of trade. When the market becomes satisfied that the issue has been resolved, we would expect WTI and LLS crude oil prices to reconnect with international crude oil prices. Resolving this issue and removing the uncertainty should greatly benefit the energy sector.

Tim Guinness, Will Riley & Jonathan Waghorn

Guinness Atkinson Global Energy Team

Opinions expressed are subject to change, are not guaranteed and should not be considered investment advice.

Mutual fund investing involves risk and loss of principal is possible. The Fund invests in foreign securities which will involve greater volatility, political, economic and currency risks and differences in accounting methods. The Fund is non-diversified meaning it concentrates its assets in fewer individual holdings than a diversified fund. Therefore, the Fund is more exposed to individual stock volatility than a diversified fund. The Fund also invests in smaller companies, which involve additional risks such as limited liquidity and greater volatility. The Fund’s focus on the energy sector to the exclusion of other sectors exposes the Fund to greater market risk and potential monetary losses than if the Fund’s assets were diversified among various sectors. The decline in the prices of energy (oil, gas, electricity) or alternative energy supplies would likely have a negative effect on the fund’s holdings.

This information is authorized for use when preceded or accompanied by a prospectus for the Guinness Atkinson Funds. The prospectus contains more complete information, including investment objectives, risks, charges and expenses related to an ongoing investment in the Fund. Please read the prospectus carefully before investing.

Cash flow is a revenue or expense stream that changes a cash account over a given period.

Distributed by Quasar Distributors, LLC.