Building Shareholder Value through M&A: Valeant Pharmaceuticals

There has been a notable increase in merger and acquisition (M&A) activity in the specialty pharmaceutical industry over the past year. This has been driven by several factors including the relatively low cost of debt and the magnitude of cost savings that can be realized. But recently, tax savings have been an additional driver of deal activity. Several companies have been doing deals to re-domicile out of high-tax jurisdictions like the U.S. into lower-tax jurisdictions like Ireland. Not only does this have the potential to lower taxes on current profits, but it also allows these companies to buy additional highly-taxed assets, integrate them into their low-tax structure, and realize meaningful tax synergies. Valeant Pharmaceuticals International, Inc. (VRX) is a Diamond Hill holding that has successfully implemented this strategy for a number of years.

Valeant was one of the first to pursue this “tax inversion” strategy through its reverse merger with Canada’s Biovail Corp. in 2010. Formerly a U.S. company, Valeant re-domiciled in Canada and turned its focus to acquisitions. Helped by a single-digit tax rate, Valeant has since created a great deal of shareholder value by rolling up dozens of assets in the fragmented specialty pharmaceutical space. The 10x increase in stock price has not gone unnoticed by competitors, with several starting to implement similar strategies. Actavis PLC (ACT), Endo International PLC (ENDP), and Perrigo Co. Ltd. (PRGO) did similar deals to re-domicile in Ireland. These companies now have stated strategies to increasingly pursue M&A going forward. Most recently, Actavis announced the pending acquisition of Diamond Hill holding Forest Laboratories, Inc. (FRX). Because of its newly-lowered tax rate, Actavis expects $100 million in tax savings from the deal.

Valeant has proven its ability to create value with this M&A-focused approach, but its low tax rate alone isn’t enough to ensure success. While the company has been one of the most active acquirers in the specialty pharmaceutical space since Mike Pearson became CEO in 2008, management is very particular about the assets they acquire. Among other criteria, management targets markets that are growing, products that are durable, and areas that have less reimbursement risk via a high cash pay component. Valeant’s two largest businesses, Eye Care and Dermatology, are examples of such markets.

To help ensure attractive returns on investment, Valeant has a high 20% internal rate of return (IRR) hurdle, and they require a six-year cash payback period. The company also leaves plenty of room for upside relative to the price paid for an asset. Management counts on selling, general, and administrative (SG&A) and research and development (R&D) synergies, but they do not ascribe value to revenue, manufacturing, or tax synergies, nor do they place value on a company’s product pipeline. Management also over delivers on its cost reduction targets. From its three largest deals – Biovail, Medicis Pharmaceutical Corp., and Bausch & Lomb, Inc. – they will have realized materially more synergies than assumed in their original deal models. In other words, Valeant often gets more than what it paid for.

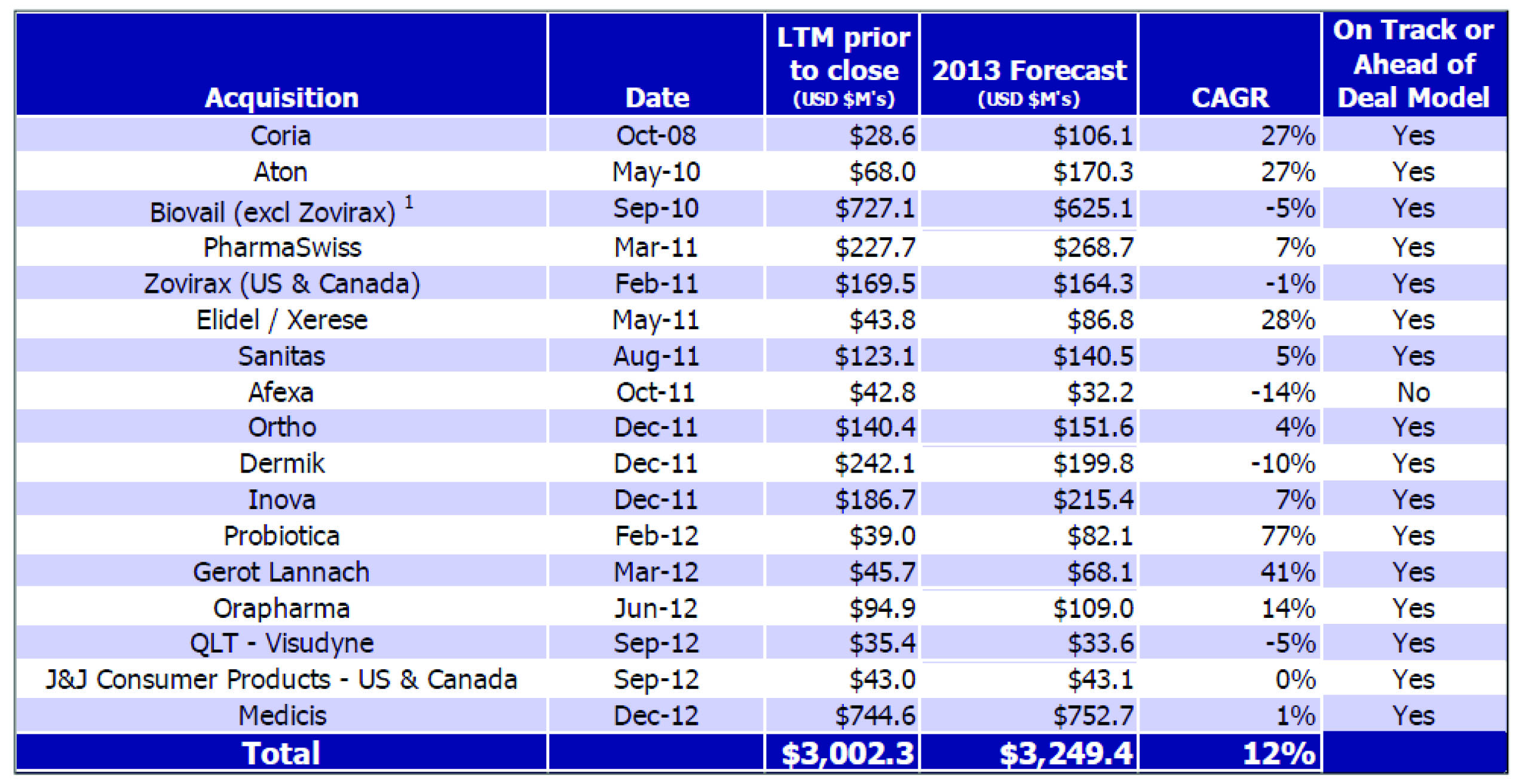

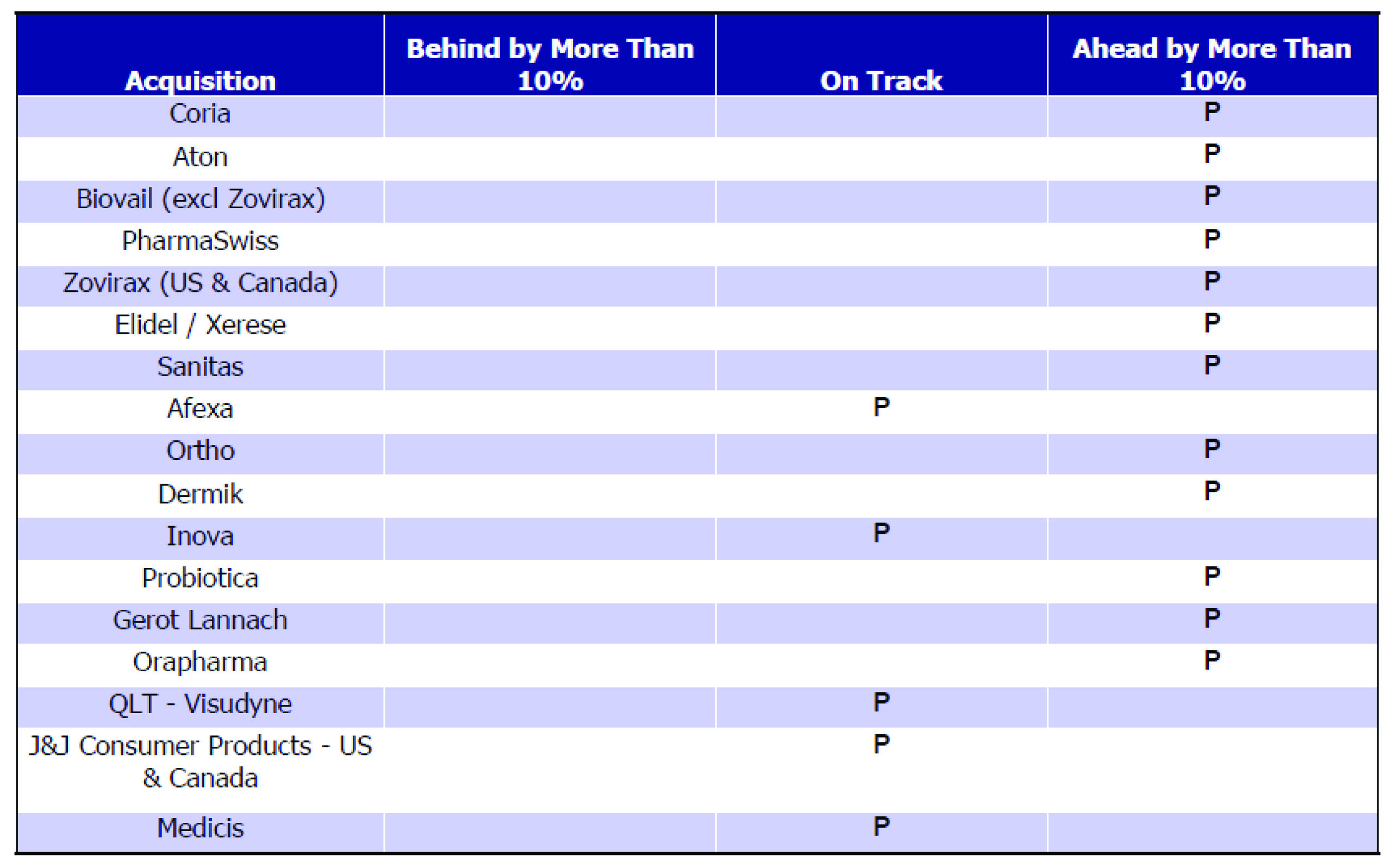

One way executives hold themselves accountable to both the Board and investors is by disclosing progress reports. The following charts are from Valeant’s 2013 second quarter earnings presentation. Not only is this level of public accountability rare, but it also highlights management’s impressive track record in acquiring assets.

Revenue Performance of Past Acquisitions

Note: Excludes deals under $75 million purchase price and transactions completed in 2013.

LTM prior to close as been adjusted to reflect 2013 foreign exchange rates.

1 Standalone Biovail, prior to its merger with Legacy Valeant

Source: Valeant Pharmaceuticals International, Inc. Earnings Presentation; August 7, 2013

Performance of Past Acquisitions Cumulative Cash Flow2 vs. Deal Model

Note: Excludes deals under $75 million purchase price and transactions completed in 2013.

2 Cash Flow from date of acquisition through Q2 2013

Source: Valeant Pharmaceuticals International, Inc. Earnings Presentation; August 7, 2013

Valeant is run by executives who put shareholders first and view capital allocation as their top priority. Much of management’s compensation is based on total shareholder return, and executives have meaningful personal investments in Valeant shares. CEO Pearson is even obligated to hold all of his shares (net of shares withheld for taxes) through 2017. Implementing its disciplined capital allocation strategy allows the company to reinvest its earnings at attractive rates of return, and there is no shortage of additional M&A opportunities. We believe management will be able to continue to identify assets it can better manage, creating meaningful shareholder value in the process. When coupled with a modest valuation, this makes for an attractive investment opportunity.

The views expressed are those of the research analyst as of April 2014, are subject to change, and may differ from the views of other research analysts, portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice. DIAMOND HILL® is a registered trademark of Diamond Hill Investment Group, Inc.

© 2014 Diamond Hill Capital Management, Inc. All Rights Reserved.

© Diamond Hill Capital Management