Take an Active Approach to Selecting Your Active Manager

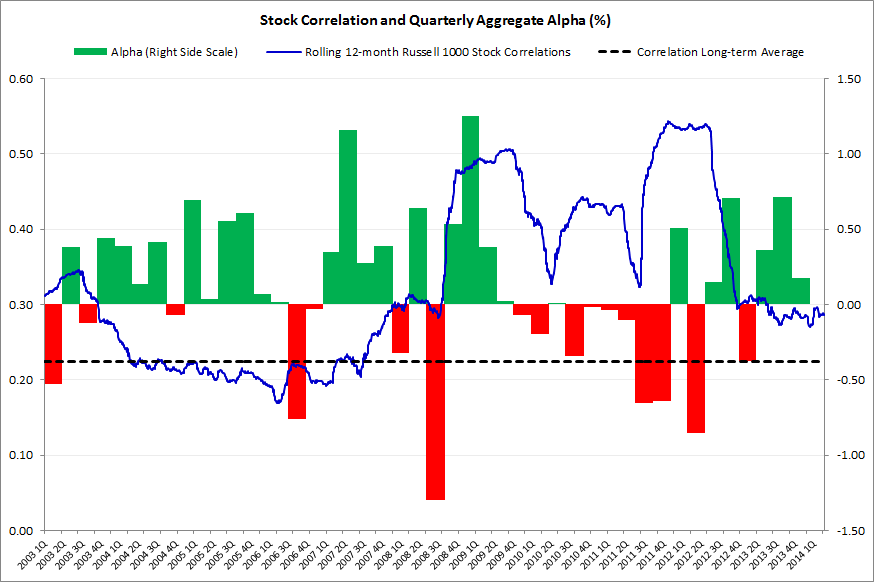

For some time, we have written about the challenges active equity managers face from a market with unusually high cross-correlations. We have also stated our belief that the correlation pendulum would swing back to more normal levels (at least) as the aftershocks of the 2008 financial crisis abated, with a corresponding benefit to active managers. That swing is well under way and a growing number of commentators have begun to echo our observation. In a comprehensive study of active managers competing against diversified U.S. domestic indices, the empirical evidence is pretty clear. Active managers have seen much greater success in a more normal cross-correlation environment while struggling to keep up with the passive competition in the historically high cross-correlation markets such as the one that resulted in the post-crisis years (Exhibit 1). We have already begun to see improving results from active managers as correlations have fallen to post-crisis lows (despite remaining above the longer term averages).

Exhibit 1:

Sources: Columbia Management Investment Advisers, LLC, S&P Capital IQ, Russell and Morningstar. The correlation long-term average timeframe is January 1990-March 31, 2014. Past performance does not guarantee future results.

All that said, normalizing cross-correlations is no panacea, and passive strategies remain a formidable performance competitor that many managers are likely to struggle to beat.

However, the rewards of adding alpha above the passive options can be extremely significant to achieving one’s long-term investment goals. Given the tremendous value of compounding positive active alpha over time, how can investors take an active approach to choosing an active equity manager? We offer a few suggestions.

1) Be sure the manager takes enough risk

Investing with an active manager reflects an inherent belief in the manager’s skill at exploiting market inefficiencies. Given that belief, you want to be sure the manager’s active risk is adequate to capture that skill over time. Active risk is a measure of a manager’s degree of divergence from his underlying benchmark. “Conservative” managers making only modest tweaks relative to benchmark may not see enough benefit from their insights to offset the inevitable frictional costs of management. As Hall of Fame NFL coach John Madden famously said on trying to play it safe, “The only thing the prevent defense does is prevent you from winning.”

2) Be sure the manager takes intentional, well-informed risk

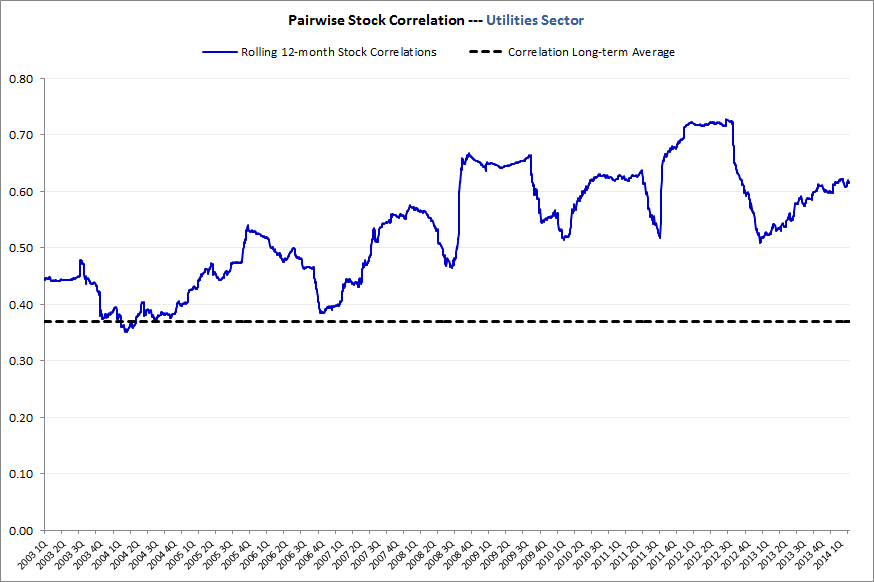

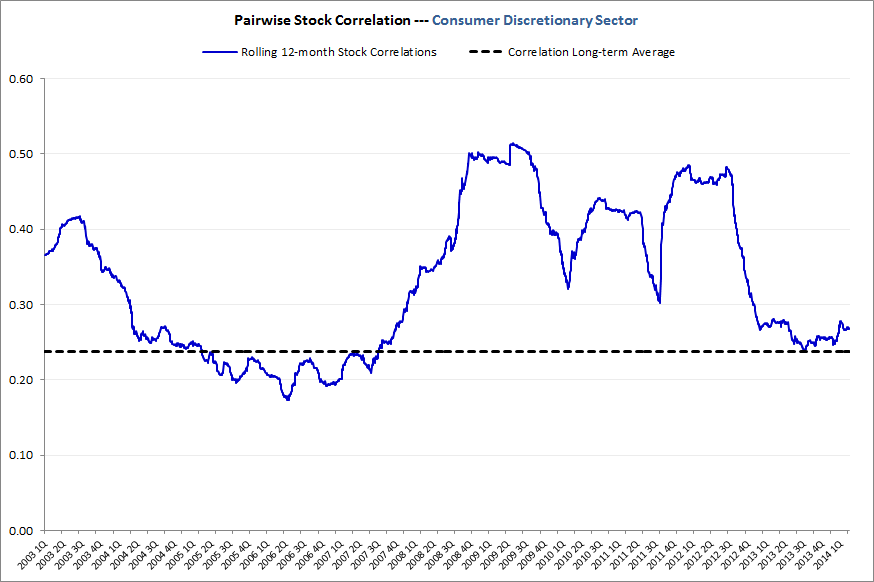

Of course, taking lots of active risk recklessly would be foolish. An investor wants to be sure that an active manager uses a risk budget precisely in areas that maximize the odds of success and in ways that avoid unintended residual risks that can undermine performance. Going back to the relationship between low cross-correlation (idiosyncrasy) and market inefficiency, it is worth noting that all corners of the market are not equally fruitful places in which to “fish” for insightful ideas. The differences between market sectors can be significant (Exhibits 2 and 3). While utilities, for example, have been acting as a homogenous, interest rate sensitive block (and increasingly so), sectors such as consumer discretionary encompass a wider range of idiosyncratic stories with a corresponding wider range of opportunities. While it is desirable for managers to target these areas, how they do so is also important. Without disciplined vigilance and high quality monitoring tools, a series of individually well-researched and logical bets in low correlation sectors might result in a cumulative residual bet on a factor the manager did not intend. We have observed many cases where managers thought they were betting on attractive sounding themes such as specific technology innovations that increase productivity, but unfortunately, a residual exposure to an unintended factor exposure such as currency fluctuation ended up being the primary driver of success or failure. A careful look at risk exposures and some basic questions can reveal whether the concentrated manager is placing bets deliberately or recklessly.

Exhibit 2:

Exhibit 3:

Sources: Columbia Management Investment Advisers, LLC, S&P Capital IQ, Russell and Morningstar. The correlation long-term average timeframe is January 1990-March 31, 2014.

3) Be sure the manager has delivered returns for that risk taken across multiple backdrops

The results of the past are no guarantee of future success. However, if an investor wants to gain confidence that an active manager can navigate the challenges of maintaining a high degree of active, intentional risk with success in a variety of market environments, it is certainly comforting to see if the manager has experience in doing so. Does the manager have the proven success in following market controversies into a variety of sectors to uncover alpha amidst uncertainty? Or did the manager happen to buy cyclicality bravely in one “risk-on” market surge? Taking a look at the characteristics and consistency of performance is telling. Metrics such as information ratios will help uncover whether the active manager is simply garnering higher returns with higher volatility or with skill. Looking at upside/downside capture over the longer run can help demonstrate skill as well as how the manager’s style might fit into your broader portfolio.

We believe that market inefficiencies remain and that there will continue to be active managers that can deliver value-added results over time. While an ongoing return to more normal market cross-correlation will reduce the headwinds for active managers, there will still be significant dispersion between the successful active managers and the also-rans. Taking a disciplined and informed approach to selecting an active manager can significantly improve your odds of achieving your desired results.

Disclosure

The views expressed are as of 4/7/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

897382