Mid-March 2014, and many market forecasts are already looking suspect. Most of the 2014 forecasts were positive on stocks, albeit at a lower return after such a strong year in 2013, and negative on bonds. However, January was a down month for stocks and a very strong month for bonds, February saw stocks rebound and bonds range-bound, and March thus far has stocks down more than up and bonds still range-bound. With apologies for altering the famous quote attributed to Audrey Hepburn in Sabrina, “Paris is always a good idea,” I would say that “ income is always a good idea,” and diversifying an income stream is also a good idea. Income can come from a variety of sources. Below, I discuss a few that might be timely for 2014 and beyond.

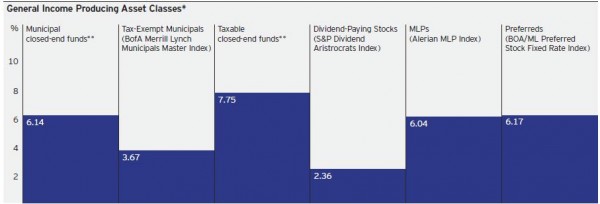

Dividend-paying stocks

One of the cornerstones of a portfolio that can provide potential growth of capital as well as increasing income is dividend-paying stocks. Income and total-return oriented investors who are suitable for equities may consider the potential benefits of investing in companies with long track records of increasing dividends annually. Dividend increases can also help investors keep up with inflation over time. Companies that increase their dividends on an annual basis may provide a better total return experience than companies with the highest-yielding dividends. Many high-quality companies were forced to cut or abandon their dividends after the financial crisis of 2007. But today, many companies have repaired their balance sheets and are in strong financial shape, with the ability to pay and grow their dividends.

Municipal bonds

In 2013, many municipal bond investors “threw the baby out with the bathwater.” High-profile credit and/or bankruptcy news from cities like Detroit caused fear among many retail investors, as evidenced by a 32-week period in which municipal bond funds experienced outflows. Today, however, investors may now be realizing the value of municipal bonds’ high-quality, tax-exempt income. Flows turned positive in January 2014, and prices have begun to recover.

Master limited partnerships (MLPs)

Equity shares in MLPs are traded on securities exchanges like shares of common stock. Most MLPs operate in the energy sector, with a particular emphasis on the midstream sector of the energy value chain, which includes the infrastructure necessary to transport, refine and store oil and gas. MLPs generally distribute nearly all of their income to investors in the form of quarterly distributions. They are not required to pay out a certain percentage of income but are able to do so because they do not pay corporate taxes.

Preferred securities

Many income-oriented investors have found that preferred securities can serve as a strong diversifier as well as a source of potentially consistent income for a portfolio. Simply put, preferred securities are a different class of ownership in a corporation that has a higher claim on the capital structure than common stock. Preferreds also typically have dividends or interest that must be paid out before dividends to common stockholders.

Source: Bloomberg L.P., FactSet Research Systems, Inc. Data as of Feb. 14, 2014. Past performance does not guarantee future results.

* Yield unless otherwise noted.

** Averages of Municipal closed-end funds and Taxable closed-end funds broad category groups in the Morningstar closed-end fund universe. Morningstar assigns categories based on average holding statistics over the past three years. Morningstar’s editorial team reviews and approves of all category assignments. Income is measured by the distribution rate for closed-end funds.

Important information

The Alerian MLP Index is a composite of the 50 most prominent energy Master Limited Partnerships (MLPs) that provides investors with an unbiased, comprehensive benchmark for this emerging asset class. The index, which is calculated using a float-adjusted, capitalization-weighted methodology, is disseminated real-time on a price-return basis (NYSE: AMZ) and on a total-return basis (NYSE: AMZX).

The S&P 500 Dividend Aristocrats Index is an index composed of 40 companies in the S&P 500 Index that have had an increase in dividends for 25 consecutive years. The S&P 500 Dividend Aristocrats Index tracks the performance of these companies. A dividend aristocrat tends to be a large blue-chip company. Indices are statistical composites and their returns do not include payment of any sales charges or fees an investor would pay to purchase the securities they represent. Such costs would lower performance. It is not possible to invest directly in an index.

STANDARD & POOR’S, S&P, S&P 500 and DIVIDEND ARISTOCRATS are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”), a wholly owned subsidiary of The McGraw-Hill Companies, Inc. Standard & Poor’s Investment Advisory Services LLC (“SPIAS”) is a registered investment advisor and a wholly owned subsidiary of The McGraw-Hill Companies, Inc. SPIAS reviews the Invesco Capital Markets, Inc.’s investment selections for the S&P Dividend Sustainability Portfolio. SPIAS does not provide advice to underlying clients of the firms to which it provides services. SPIAS does not act as a “fiduciary” or as an “investment manager,” as defined under ERISA, to any investor. SPIAS is not responsible for client suitability. Past performance is not indicative of future returns.

SPIAS, S&P and their affiliates do not sponsor, endorse, sell, promote or manage any investment fund or other vehicle that is offered by third parties and that seeks to provide an investment return based on a SPIAS investment strategy or the constituents or the returns of any index. SPIAS, S&P and their affiliates make no representation regarding the advisability of investing in any such investment fund or other vehicle. With respect to recommendations made by SPIAS, investors should realize that such information is provided only as a general guideline. SPIAS does not take into account any information about any investor or any investor’s assets when providing its services. There is no agreement or understanding whatsoever that SPIAS will provide individualized advice to any investor. SPIAS does not have any discretionary authority or control with respect to purchasing or selling securities or making other investments. Individual investors should ultimately rely on their own judgment and/or the judgment of a financial advisor in making their investment decisions. There is no assurance that future dividend payouts will equal or exceed past dividend payouts. Standard & Poor’s parent company, The McGraw-Hill companies, Inc. may be one of the constituents of the S&P 500 Dividend Aristocrats Index and may be included in the portfolio based solely on quantitative measurements.

For additional disclaimers and disclosures for SPIAS, please seehttp://www.standardandpoors.com/regulatory-affairs/spias/en/us

The BofA Merrill Lynch Municipals Master Index measures total return on tax-exempt investment grade debt publicly issued by U.S. states and territories, and their political subdivisions, including price and interest income, based on the mix of these bonds in the market. This index is often used as a reference for the performance of tax-exempt U.S. municipal bonds.

The BofA Merrill Lynch U.S. Preferred Stock Fixed Rate Index consists of fixed rate U.S. dollar denominated preferred securities and fixed-to-floating rate securities that are callable prior to the floating rate period and are at least one year from the start of the floating rate period. Securities must be rated investment grade including the country of risk and must be issued as public securities or 144a filing and a minimum outstanding of $100 million. The index includes perpetual preferred securities, American Depository Shares/Receipts (ADS/R), domestic and Yankee trust preferred securities having a minimum remaining term of at least one year, both DRD-eligible and non-DRD eligible preferred stock and senior debt.

About risk

Common stocks do not assure dividend payments. Dividends are paid only when declared by an issuer’s board of directors and the amount of any dividend may vary over time.

In general, stock values fluctuate, sometimes widely, in response to activities specific to the company as well as general market, economic and political conditions.

Municipal securities are subject to the risk that legislative or economic conditions could affect an issuer’s ability to make payments of principal and/ or interest.

Preferred securities may include provisions that permit the issuer to defer or omit distributions for a certain period of time, and reporting the distribution for tax purposes may be required, even though the income may not have been received. Further, preferred securities may lose substantial value due to the omission or deferment of dividend payments.

Shares of closed-end funds (CEFs) frequently trade at a discount to their net asset value in the secondary market and the net asset value of closed-end fund shares may decrease.

Depending on a CEF’s underlying holdings, its distributions can include interest income, dividends, capital gains or a combination of these types of payments. In some cases, distributions also include a return of principal, sometimes referred to as a return of capital. That means the monies used to pay the distribution come from the fund’s assets rather than from any income generated by the investments in the fund’s portfolio. CEFs that return capital can carry a higher level of risk because the fund is eroding the asset base it has to generate income to pay distributions.

Most MLPs operate in the energy sector and are subject to the risks generally applicable to companies in that sector, including commodity pricing risk, supply and demand risk, depletion risk and exploration risk. MLPs are also subject the risk that regulatory or legislative changes could eliminate the tax benefits enjoyed by MLPs which could have a negative impact on the after-tax income available for distribution by the MLPs and/or the value of the portfolio’s investments.

Diversification does not guarantee a profit or eliminate the risk of loss.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

|

NOT FDIC INSURED |

MAY LOSE VALUE |

NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc., is the US distributor for Invesco Ltd.’s Retail Products and Collective Trust Funds.

Invesco Unit Investment Trusts are distributed by the sponsor, Invesco Capital Markets, Inc. and broker dealers including Invesco Distributors, Inc.

© 2014 Invesco Ltd. All rights reserved.