By the middle of this year, the economic expansion in the U.S. will officially turn five years old. By comparison, the average of all business cycle expansions tracked by the National Bureau of Economic Research dating back to the mid-1800s is about three and half years. But like many five year olds, this cycle hardly seems mature. In particular, we have taken notice of three key elements of the business cycle that have distinct implications for bond investing today.

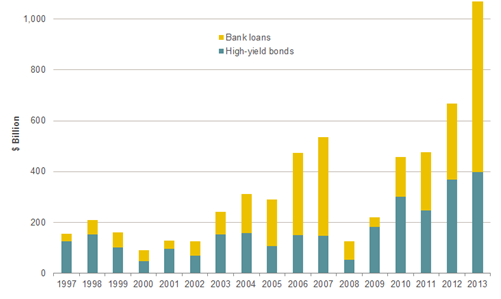

The credit cycle is the most advanced element of this business cycle in our view. In the depths of the financial crisis, the credit spigot was all but shut off for U.S. corporations. Since then, the market has meaningfully healed, and issuance today is robust with more than $1 trillion of high-yield corporate securities issued in the U.S. last year (see Exhibit 1). While we expect corporate health to remain stable and default rates low over the next year, we are definitely seeing a shift in corporate behavior in favor of equity enhancing transactions (dividends, share buybacks) at the expense of credit quality. In bond portfolios, we retain a core allocation to corporate sectors overall, but have started to reduce exposure both to high-quality bonds with limited upside potential as well as high-yield bonds and loans in which credit risk or covenants appear too aggressive.

Exhibit 1: High yield corporate new-issue volume

Source: JP Morgan

The economic cycle is favorable at this stage, but much less advanced than the credit cycle. While moderate growth continues, the economy has yet to recover all of the jobs lost during the recession, and unemployment is still above the Fed’s target. The U.S. housing market is improving on the back of reduced supply, labor market improvements and overall confidence. We believe this creates opportunities for bond investors in the non-agency mortgage market, as well as in certain corporate industries. Internationally, growth has generally lagged the U.S. However, we are now starting to see better growth in Europe and Japan which we expect to broaden to emerging markets as well. Following weakness last year, emerging market debt has posted gains this year, and we expect further strength ahead as volatility subsides.

The monetary policy cycle is the element of the cycle that remains in early stages. Technically speaking, monetary policy is still getting easier as the Fed continues to grow its balance sheet via asset purchases. However, the Fed has been tapering these purchases, and is on track to wind down this program completely by year end. Furthermore, recent comments from Fed Chair Yellen indicate that interest rate increases are quite possible by mid next year. From current levels, we think intermediate-maturity yields (3-7 year) should rise, and investors should reduce interest rate risk, or duration, in that part of the curve. We expect a flatter yield curve over the next few months as investors focus less on tapering, and more on the timing and pace of rate increases. However, we don’t think investors should avoid duration altogether. While short-term rates will eventually rise, the yield curve is exceptionally steep, and longer maturity yields are not obviously mispriced.

Over time, turns in the business cycle have significantly impacted financial asset performance. Now more than ever, we believe unique elements of the business cycle are proceeding at different speeds. As the cycle progresses, the Fed will spend less time committing to low rates, and more time responding to real changes in the economy. This will create uncertainty, but it will also create opportunities for flexible investors in the year ahead.

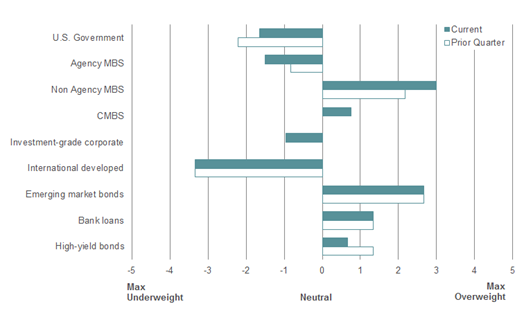

Exhibit 2: Representative fixed-income allocation

Source: Columbia Management Investment Advisers, LLC

Disclosure

The views expressed are as of 3/31/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

892611