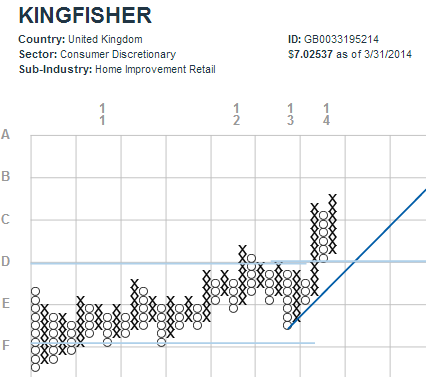

As notedyesterday, March was not an exceptionally positive month for European equities. One (non-Utility) sub-industry that stood out, however, was Home Improvement Retail. Considering that this group consists of just one company in MSCI Europe and that the company is in the U.K.-- where housing in general has been quite strong recently-- this might not be all that surprising. Nonetheless, we took a deeper look into the drivers of Kingfisher's outperformance versus the MSCI World Index after years of lackluster trading.

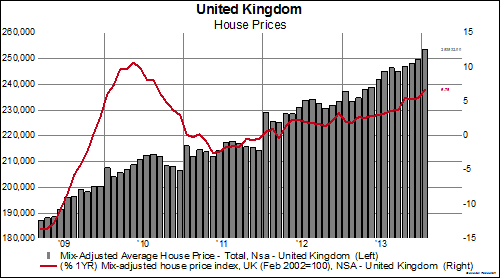

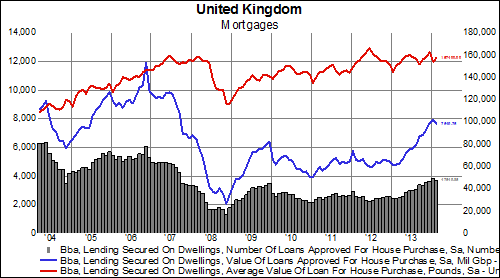

To be sure, the housing market in the U.K. has seen a decent recovery over the last few years, notwithstanding last month's small pullback in mortgage lending:

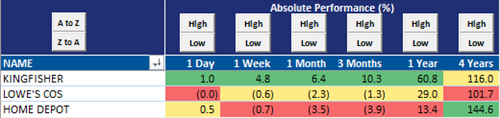

Whether programs like 'Help to Buy' are pushing U.K. housing into bubble territory or not, Kingfisher's strong performance is undeniable, even versus its sub-industry peers:

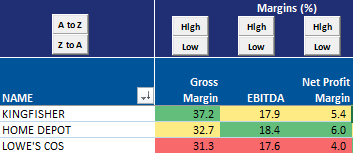

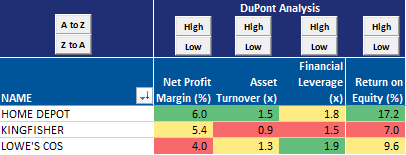

With the second highest level of cash as a percent of assets andnegativenet debt on its balance sheet, the company also generates the highest gross margins of the group-- all with the lowest financial leverage:

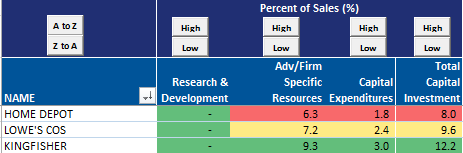

Of course, we are always eager to see the importance a company places on intangible investments. Kingfisher doesn't disappoint-- in fact, it invests more than Home Depot or Lowe's when it comes to intangible capital as a percent of sales:

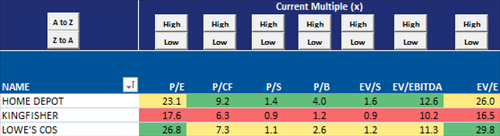

All of this and the company still trades at at valuations well below its peers: