Since hitting a low on June 1, 2012, the MSCI Europe Index has rallied 64.73%.1 In our view, there’s room for European equity markets to advance further, supported by strong fundamentals, positive flows and a steady uptrend from the June 2012 low.

European economic momentum outpaces US

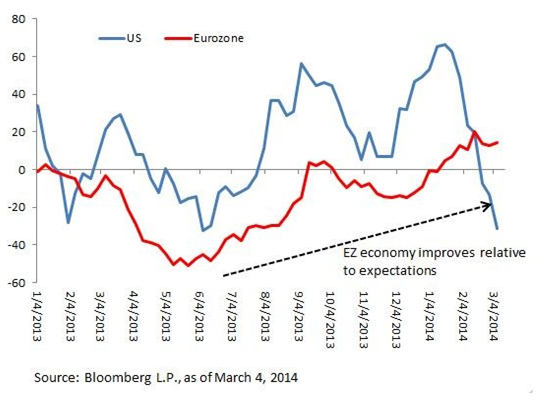

The US economy has shown loss of momentum in early 2014. As the graph below shows, the U.S. Citi Economic Surprise Index, which measures the actual outcome of economic data releases relative to consensus estimates — has tumbled from a peak of 65.5 in early January to a low of -13.4 in the week ending March 4, 2014. In contrast, the Eurozone (EZ) Citi Economic Surprise Index turned positive in 2014 and has been trending positively higher since the spring of 2013.

Citi Economic Surprise Index Shows Positive Eurozone Trend

European growth prospects have improved

In addition, manufacturing purchasing managers index (PMI) data indicate that economic growth is improving in the eurozone, despite volatility in early 2014, while it’s decelerating in the US, as the graph below shows. European PMI indexes are expanding after a period of contraction between 2011 and early 2013.

European Economic Growth Is Trending Positive

Other indicators point to positive

Beyond positive momentum and growth prospects, these indicators support our view that the European rally appears sustainable:

- Eurozone monetary policy is pro-growth and favorable for equity valuation. The European Central Bank is showing willingness to provide additional monetary accommodation and support economic growth as reflected in a sustained inflation rate below 1.0%. Moreover, low inflation is placing downward pressure on eurozone sovereign yields, creating lack of an alternative to equities. For example, the 10-year German Bund was recently quoted just above 1.60%, while the dividend yield on the Euro Stoxx 50 Index was roughly 3.40%.1 By comparison, in the US, the dividend yield on the S&P 500 Index is about 1.95% against a 10-year Treasury yield just below 2.70%.2

- Valuation for European stocks looks attractive. European equities look inexpensive compared with the S&P 500 Index. The Euro Stoxx 50 Index and the FTSE 100 Index are trading at 12.7x and 12.8x expected 2014 earnings per share, respectively2. In contrast, the S&P 500 Index is trading at 15.2x forecast 2014 earnings per share.2

- Finally, investment flow has been strong as investors take advantage of the favorable macro backdrop in Europe. According to Bloomberg, exchange-traded fund flows into the European region have totaled $5.1 billion year-to-date and $22.4 billion in the 52 weeks ending Feb. 26, 2014.2 Technically, robust inflows have supported the previously mentioned steady uptrend in the price of the MSCI Europe Index since the June 2012 low.

We believe that European equities are inexpensively priced, while economic conditions in Europe are improving. As a result, we believe that European equities are a compelling investment opportunity.

1 Source: Bloomberg L.P., data as of Feb. 26, 2014

2 Source: Bloomberg L.P., June 1, 2014, to Feb. 27, 2014

The MSCI Europe Index is a market-cap weighted index used to measure the performance of European equities. The Economic Surprise Index measures the trend in economic indicators relative to expectations. It is seen as a gauge of an economy’s economic strength. A positive value indicates that economic numbers are tracking above expectations, while a negative value indicates that economic numbers are tracking below expectations. The Manufacturing Purchasing Managers Index(PMI) is an indicator used to measure the strength of economic activity. The S&P 500®Index is a market-capitalization weighted index considered representative of the US stock market. The Euro Stoxx 50 Index measures the performance of blue-chip eurozone equities. The FTSE 100 Index is considered representative of the UK stock market.

About risk

Foreign investments may be affected by changes in a foreign country’s exchange rates, political and social instability, changes in economic or taxation policies, difficulties when enforcing obligations, decreased liquidity, and increased volatility. Foreign companies may be subject to less regulation resulting in less publicly available information about the companies.

Many countries in the European Union are susceptible to high economic risks associated with high levels of debt, notably due to investments in sovereign debts of European countries such as Greece, Italy and Spain. One or more member states might exit the European Union, placing its currency and banking system in jeopardy. The European Union faces major issues involving its membership, structure, procedures and policies, including the adoption, abandonment or adjustment of the new constitutional treaty, the European Union’s enlargement to the south and east, and resolution of the European Union’s problematic fiscal and democratic accountability. Efforts of the member states to further unify their economic and monetary policies may increase the potential for the downward movement of one member state’s market to cause a similar effect on other member states’ markets. European countries that are part of the European Economic and Monetary Union may be significantly affected by the tight fiscal and monetary controls that the union seeks to impose on its members.

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is a US distributor for retail mutual funds, exchange-traded funds, institutional money market funds and unit investment trusts.

Invesco unit investment trusts are distributed by the sponsor, Invesco Capital Markets, Inc. and broker dealers including Invesco Distributors, Inc. These Invesco entities are indirect, wholly owned subsidiaries of Invesco Ltd.

© 2014 Invesco Ltd. All rights reserved.