Last week, at Janet Yellen’s first meeting as Fed Chair, the FOMC revised its forward guidance for the funds rate, dropping its reference to 6.5% unemployment and instead stressing the committee’s qualitative assessment of the economy. The change was a symbolically important step, but did not alter the broader outlook for policy rates, in our view. The existing guidance was already obsolete, which is why markets hardly reacted as the unemployment rate fell close to the threshold. What matters most for the outlook is not the details of last week’s statement, in our view, but the fundamental differences between the Fed’s forward guidance for 2014, and that for 2015 and beyond.

The styles of forward guidance provided by central banks differ along two main dimensions: (1) the degree of commitment and (2) the motivation for providing guidance in the first place. Both aspects can affect credibility, and therefore the importance of these statements for markets.

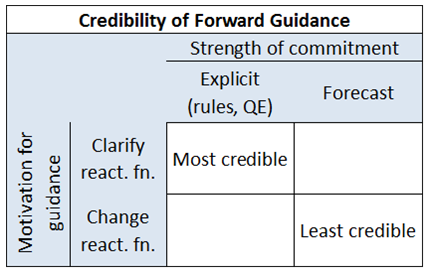

Forward guidance can take the form of an explicit commitment or a forecast. Central banks never make unconditional promises (at least about instruments), so there is not a black and white difference between commitments and forecasts. But in general, commitments are more difficult to reverse, either because policymakers’ credibility is on the line or because of institutional details of the policy framework. Statements that contain explicit commitments are more credible and should be taken more seriously by investors. Forward guidance based on forecasts alone (“we think we will raise rates next year because we forecast that inflation will rise”) is easier to reverse, less credible and should be given less weight by investors (even if it conveys some relevant information).

The motivation for forward guidance also differs over time and across countries. The distinction comes down to whether guidance intends to clarify the existing policy approach or signals an intentional deviation from historical policy. In other words, whether it simply restates the reaction function or changes the reaction function. The European Central Bank, for instance, is adamant that its “extended period” guidance is meant to clarify its existing approach, and nothing more. In contrast, many academic economists argue that policymakers should use forward guidance to intentionally deviate from past behavior in order to provide additional monetary stimulus at the zero lower bound—i.e. to go “lower for longer.” In our view, forward guidance that clarifies an existing framework is more credible, because the central bank will be less likely to change its mind in the future. Forward guidance which intends to deviate from past behavior should be considered less credible, because we cannot be sure that the central bank in the future will actually follow through with the plans laid out in the past (especially when the composition of the policy committee changes over time).

The table on the next page summarizes these ideas. The most credible type of forward guidance is one that clarifies the existing policy approach and backs up statements with some type of commitment. The weakest type of forward guidance is a forecast that the central bank will behave in the future differently than it has behaved in the past—a forecasted change in the reaction function.

The Fed’s communication for 2014 looks like the strongest type of forward guidance. Standard Taylor Rules would still imply short-term interest rates around zero for most of this year, so there is no reason to think that the Fed will not follow through on its guidance if the economy performs as expected—they are only restating the existing reaction function. In addition, this year’s guidance is backed up by a very strong form of commitment: quantitative easing (QE). Investors know that the Fed will not raise rates while they are still expanding the balance sheet. Plus, public communication from Fed officials suggests low odds that the pace of tapering ($10 billion per meeting) will either speed up or slow down. We can therefore be reasonably confident that QE will continue—and the funds rate will remain at zero—for most of this year. This is the reason why the 6.5% unemployment threshold is now irrelevant: it’s been superseded by the long tapering timeline.

Current statements for 2015 and beyond are closer to the weakest type of forward guidance. First, there will be no commitment device in place when QE ends. This means that the committee could behave differently than planned, even if the economy performs in line with expectations. Without a transparent policy rule or ongoing QE, there is little to bind the future Fed to today’s promises.

Second, the policy outlook in the Summary of Economic Projections (SEP) differs from past behavior—at least to a degree. Fed communication actually sends mixed signals on this point, which we assume reflects differences of opinion between policymakers. The SEP forecasts show rate hikes beginning only in late 2015 and then proceeding very slowly. Some officials explain this by referencing “headwinds,” while others point to “lower for longer” considerations. For instance, the following segment appeared in the minutes of the October FOMC meeting:

“the policy statement could indicate that even after the first increase in the federal funds rate target, the Committee anticipated keeping the rate below its longer-run equilibrium value for some time, as economic headwinds were likely to diminish only slowly. Other factors besides those headwinds were also mentioned as possibly providing a rationale for maintaining a low trajectory for the federal funds rate, including following through on a commitment to support the economy by maintaining more-accommodative policy for longer.” (emphasis added)

One could argue that the “headwinds” idea is a way to clarify the reaction function in light of the particular challenges in the post-crisis economy, rather than intentionally follow a different reaction function than in the past.

That being said, we know that Janet Yellen sees the SEP forecasts as a change in the reaction function. She said this in a speech last year:

“I view the Committee’s current rate guidance as embodying exactly such a ‘lower for longer’ commitment. In normal times, the FOMC would be expected to tighten monetary policy before unemployment fell as low as 6-1/2 percent.”

Thus, the structure of the Fed’s forward guidance means that its statements for anything beyond 2014 should be considered less credible. Funds rate forecasts in the SEP for 2015 and 2016 intentionally deviate from historical behavior—at least in Yellen’s view—and are not backed up by explicit commitments. For this reason, economic fundamentals like the size of the output gap should be more important for forming views about policy rates in these years than the SEP “dots.” Look for the market’s heavy reliance on the SEP forecasts to fade over time.

Disclosure

The views expressed are as of 3/24/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

887931