Despite last week’s vernal equinox, signaling the first day of spring on Thursday, another arctic blast is hitting the Midwest yet again this week, and cabin fever has become an epidemic. So many of my friends and family are singing the same refrain; “When will this winter be over?”

Even in a day and age when people acknowledge the need to get out and run or walk, most are now staying in their houses, secure from the cold but at liberty only to be bored. They want out, but with temperatures dropping into the teens or worse nightly, they fear that every little puddle formed when the sun comes out later in the day is going to be frozen for their morning or evening constitutional. They fear becoming caught in a snare of black ice that will send them tumbling into a broken “something.”

And the fear is real. All of us here in the “winter states” know someone who has slipped and fallen this winter and has suffered a broken wrist, leg, elbow or hip. It just comes with the territory.

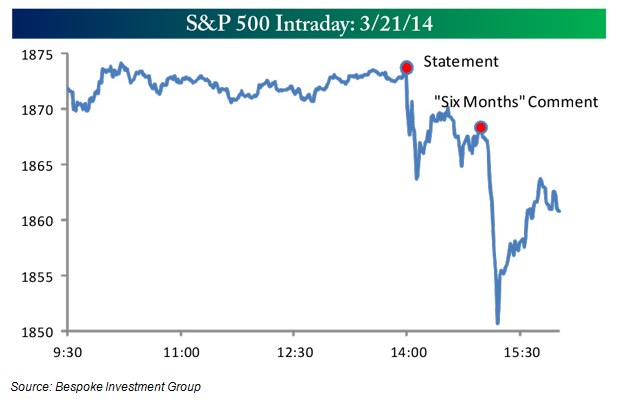

The same is true of the financial markets. Witness what happened last week as new Federal Reserve Chairperson, Janet Yellen, presented her first Federal Reserve Open Market Committee statement and held her first press conference as Chairperson. When she “slipped” and said that the Fed would start to raise interest rates “six months” after it stopped buying Federal paper (instead of the year that the market had been assuming), the stock market began to “fall.”

Of course, stock market investors hate the thought of higher interest rates; they generally drive stock prices lower. But as I said last week, a move higher will still leave interest rates below average for quite a long time to come. Plus, using the Fed’s own statements and a bit of arithmetic, it seems likely that the first Fed-required increase in rates will not occur until mid- to late-2015!

So most of last week’s market action was the usual knee jerk, anticipatory volatility that we warned would be more prevalent this year. Of course, the Ukrainian crisis is also to blame.

With few shots being fired, Russia has effectively annexed the Crimean Peninsula, taking back land given to the Ukraine by Russia in a treaty just two decades ago that was supposedly backed by the USA. With the benefit of the history prior to the last two World Wars, it can be surmised that this weekend’s troop movements along and, some say through, the southern and eastern borders of the Ukraine, were caused at least in part by Russian President Vladimir Putin being emboldened by the relatively weak response of the western powers.

Just as we saw before these conflagrations, where the aggressor has claimed that it was taking back land that was historically theirs to protect those of their culture, Russia is now claiming the same regarding the Crimea, and now for all of the Ukraine. Yet as my own family history testifies to, the Ukraine is an area of many cultures. In the 1800’s it was a vast unpopulated frontier much like our West. My family, along with many Germans, was attracted to colonize the whole territory from Kiev back to the border. Many other nationalities were recruited to pioneer the Ukraine in much the same fashion.

It is certainly the case that the Ukraine makes a negligible contribution to world GDP and even less to the US economy. And as Warren Buffet stated last week, fears of the Ukrainian situation affecting our stock market “are not warranted.” Still, putting the Russian actions in a historical perspective, it’s easy to see why our market is uneasy and reacts negatively, like it is today, to the latest Ukrainian news.

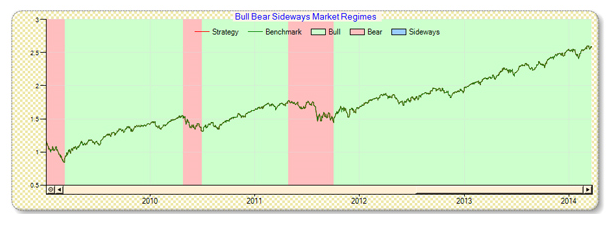

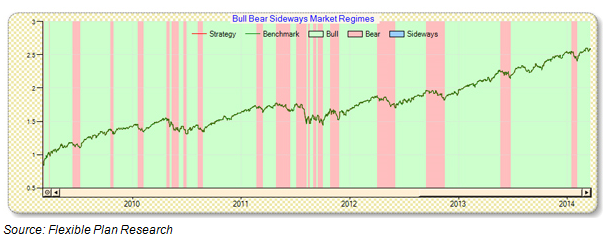

Speaking of perspective, as the first chart shows we have not seen a 10% or greater decline in the S&P 500 since 2011 and only two times since the current bull market began in March of 2009. The second chart demonstrates that, on the other hand, 5% declines have been much more prevalent. We’ve had eight since that 10%-plus decline in 2011. (The charts are from a tool we created to test strategies in Bull, Bear and Sideways markets, in these two examples no strategies, and only bull and bear markets are shown.)

These 5% declines, and a whole lot more that did not reach that percentage, are like when people slip and catch themselves, or as happened to me last week, I slipped and fell but did not hurt a thing. Yet as I have been saying since December, I believe that sometime this year we will “slip and fall” more than 10%.

That’s the general definition of a correction. As occurred in 2011, we tend to recover quickly from a correction. In contrast, I do not think we are headed for a bear market – a fall of the 20%, 30%, 40% or 50% magnitude.

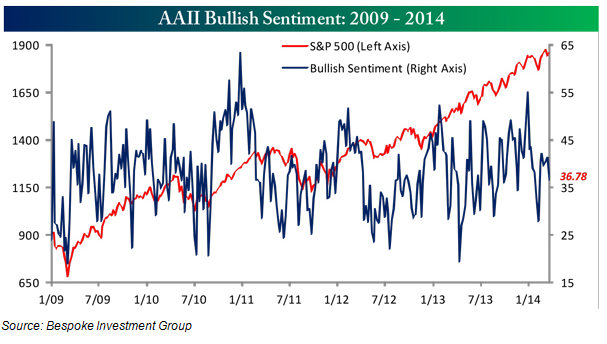

Nor do most investors think so. Sentiment surveys continue to show investors in a middle ground, not at either a bullish or a bearish extreme.

Surprisingly though, it continues to be apparent that many investors are still under invested in stocks. Like the health conscious Midwesterners who stay inside afraid of a slick spot, avoiding a slip and fall when they know that for their long-term good health they should be outside exercising, investors are staying inside their bond and money market funds where they will receive little protection from the ravages of rising interest rates and inflation that are more likely than the 2008-type implosion of the financial markets.

Still, the fears are rational. Most investors have experience in the 2007-2008 decline and maybe the 2000 to 2002 collapse as well. They know the pain.

That’s why dynamic risk-managed investing was created. I find myself fighting the same urges to take my money and run as you do. But more than 30 years ago I began using tactical investing strategies to manage my risk rather than depending solely on diversification to do that job. Since that time, each decline has been mitigated – not the little 5 to 10% dips, but the big falls that seem to occur every three to seven years.

I know it is hard when the market is volatile, but if the strategies are bullish on stocks (as they are now) and we start to slip or even take a minor fall, that’s the time for investors to move to dynamic, risk-managed investment strategies, which are designed to capture some of each bull market while avoiding much of the bear. And when first quarter earnings reports begin to arrive in a couple of weeks, they could prove to be the impetus for another push higher in the stock market.

Just as many Americans seek refuge in the local gym for a protected spot to get their exercise in the cold of winter, dynamic risk-managed investment strategies were designed to be a safer place to avoid the black ice found in today’s financial markets. As I found out last week, when you slip and fall you don’t have to break anything, and it’s a lot better getting out of the house than just sitting around inside. Who knows when spring will really come?

All the best,

Jerry