The Federal Reserve implemented an unprecedented experiment through three rounds of large-scale asset purchase programs, commonly referred to as quantitative easing or QE, from November 2008 through the end of 2013. These programs in aggregate have allowed for the purchase of up to $3.49 trillion in agency mortgaged-back securities (MBS), agency debt and U.S. Treasuries.

This amount is equivalent to 211 times the median market cap of the S&P 500, 19.9% of the market cap of the entire S&P 500 Index, or nearly seven times the market cap of Apple Inc. During the same period (11/25/2008 – 12/31/2013), the S&P 500 Total Return Index (S&P 500) has produced a cumulative total return of 142.7%, reaching a number of record highs along the way and surpassing advances from the previous two bull markets of 116.2% and 120.6%, from the bull markets of 1997 – 2000 (1/1/1997 – 3/24/2000) and 2002 – 2007 (10/10/2002 – 10/9/2007), respectively.

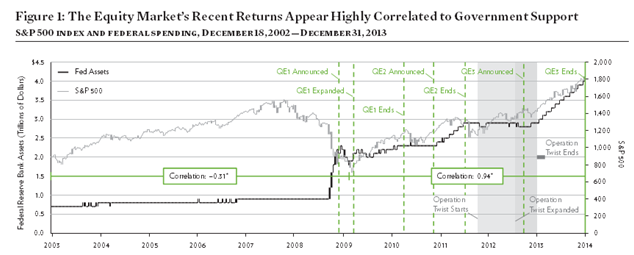

Figure 1 shows an interesting relationship between equity prices and the growth of the Fed’s balance sheet through the various QE pro- grams. Since November 2008, the correlation between the Fed’s balance sheet and the S&P 500 has been quite strong at 0.94, whereas prior to implementation of the QE programs, specifically, December 2002 through February 2009, the correlation was weak at –0.31. While the QE programs did not directly affect equity prices, some believe that the Fed’s presence as a large and indiscriminate buyer in the market has pushed other investors into incrementally higher risk asset classes, eventually impacting equity prices.

Prior to QE1, the Fed’s balance sheet was composed predominately of short-term U.S. Treasury securities. The Fed purchased these securities through its typical open market operations with the goal of maintaining market conditions consistent with the federal funds target rate, set by the Fed Open Market Committee (FOMC). In September 2008, at the height of the financial crisis, the Fed sharply increased the size of its balance sheet through a number of temporary liquidity programs (direct bank lending, central bank liquidity swaps, commercial paper/money market facilities, and funds related to the rescue of Bear Sterns and AIG). These programs more than doubled the size of the Fed’s balance sheet over a two-month period, though they were steadily reduced to pre-crisis levels by the end of 2009.

In November 2008, weeks prior to reducing the fed funds target range to 0 – 0.25%, thereby removing the ability to further stimulate the economy by reducing this rate, the Federal Reserve announced the first round of quantitative easing, later dubbed QE1. The overnight federal funds rate had been at 3.50% in January 2008 and was at 1.50% as recently as October 2008. QE1 allowed for the purchase of $1.75 trillion in bond purchases (MBS, agency bonds, and Treasuries). Over two-thirds of the program was directed to the purchase of MBS, with the objective of supporting mortgage lending and the housing markets.

Source: PerTrac. Federal Reserve Bank of St. Louis.

*Correlation between the Federal Reserve Spending and the S&P 500 Index: from December 18, 2002 – February 25, 2009, the correlation is –0.31; from March 4,2009 – December 31, 2013, the correlation is 0.92. Index returns are provided for illustrative purposes only to demonstrate a hypothetical investment vehicle using broad-based indices of securities. Returns do not represent any actual investment. Past performance is no guarantee of future results. The illustrations are not intended to predict the performance of any specific investment or security. The unmanaged indices do not reflect fees and expenses and are not available for direct investment.

The later expansion of QE1 was officially announced shortly after the March 9, 2009 equity market lows and nearly tripled the size of the original program. News of the announcement and speculation ahead of the announcement of the program’s expansion served as one of the catalysts for the initial rise in equities. QE2 was announced in November 2010 and was the smallest and shortest in duration of the three programs; it allowed for the purchase of $600 billion in long- term Treasury purchases with a broad goal of promoting a stronger pace of economic recovery.

Instead, this program extended the average maturity of the Fed’s holdings in U.S. Treasury securities by selling $667 billion in short- term securities (less than three years) and purchasing an equal amount of long term securities (6 – 30 years).

QE3 was originally a continuation of Operation Twist’s long-term Treasury purchases when it was announced in September 2012, but was expanded months later to include MBS purchases as well. QE3 has allowed for the purchase of up to $1.14 trillion in bonds through December 31, 2013, with the intention of putting downward pressure on long-term interest rates and supporting mortgage markets.

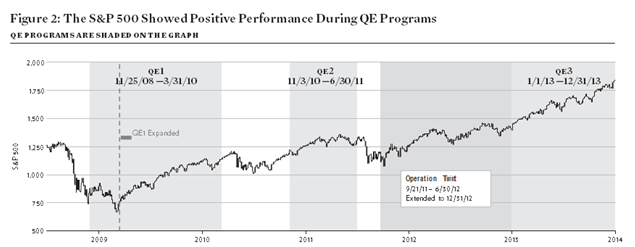

The time periods when the Fed has been a purchaser of assets outside of its typical open market operations have been matched by significant moves in the equity markets.

This can be seen in Figure 2. The S&P 500 produced cumulative total returns of 53.6%, 12.2% and 61.7% during the respective periods for QE1 from its expansion date (3/18/2009 – 3/31/2010), QE2 (11/3/2010 – 6/30/2011), and the combined period of Operation Twist and QE3 through the end of 2013 (9/21/2011 – 12/31/2013). Also, during these periods of asset purchases, the S&P 500 never saw even a technical correction of down 10%.

Conversely, there were notable declines in the S&P 500 during recent periods when the Fed stopped asset purchases, with drawdowns of –15.6% between QE1 and QE2 in 2010 (4/1/2010 – 11/2/2010), and –17.2% between QE2 and Operation Twist in 2011 (7/1/2011 – 9/20/2011). We should note that the reason for the equity decline was likely not the removal of the QE programs alone. In the 232 days after QE1 ended in March 2010, the market was affected by the BP rig explosion, a Greece bailout, the “Flash Crash,” and heightened European debt crisis fears. In the 83 days after QE2 ended in June 2011, the market was impacted by Washington’s handling of the budget and debt ceiling debate, the U.S. debt downgrade, fears of another U.S. recession and renewed concerns about Europe. Both of these periods can be characterized as flight-to-quality periods as money flowed to the safe haven of U.S. Treasuries, causing yields to decline sharply and bond prices to rise.

On December 18, 2013, the Federal Reserve announced it would “taper” or reduce QE3’s bond purchases by $10 billion per month starting in January, with $5 billion in reductions to both long-term Treasury and MBS purchases. While it is not yet clear when asset purchases will end, we believe it is likely that the impact from QE going forward will diminish and fundamentals may become more important. Even if the correlation of the Fed’s balance sheet and the S&P 500 were to continue into 2014, with tapering now in place, the trajectory of the growth of the Fed’s balance sheet will begin to level off, which would imply a slower pace of growth in equity prices.

Beyond the potential diminished effects of QE, there are other market risks; for example, market multiples no longer appear cheap. Both the S&P 500’s trailing and forward 12-month P/E ratios are currently above their five- and 10-year averages. Multiples have also expanded, with only a moderate level of earnings growth and meager level of revenue growth, as the S&P 500’s EPS grew 5.7% year-over- year in 2013 and revenue per share grew just 2.9%.

Source: Yahoo. Index returns are provided for illustrative purposes only to demonstrate a hypothetical investment vehicle using broad-based indices of securities. Returns do not represent any actual investment. Past performance is no guarantee of future results. The illustrations are not intended to predict the performance of any specific investment or security. The unmanaged indices do not reflect fees and expenses and are not available for direct investment.

On the positive side, the U.S. economic recovery appears intact, with Q3 GDP growth revised to 4.1%, the S&P/Case Shiller composite index of 20 metropolitan areas showing 13.3% year-over-year growth in home prices through October, and the U.S. ISM Manufacturing index at its highest level in over two years in November. December’s budget deal appears to be a notable change from the bipartisan gridlock in D.C. Furthermore, the Federal Reserve has stated that it remains committed to highly accommodative monetary policy for a “considerable amount of time” even after QE ends.

In 2013, the S&P 500 had its best year since 1997 with a 32.4% total return, and all ten sectors within the index returned over 10% for the first time since 1995. Given the size of the market move now behind us and the amount of ambiguity currently in the equity market, we believe the opportunity set for hedged and long/short strategies is attractive as the market environment evolves into one where the asset price movements of winners and losers could be more clearly differentiated.

Definitions

Correlation: This is a statistical measure of how two securities move in relation to each other.

S&P 500 TR Index: This is an index of 500 stocks chosen for market size, liquidity, and industry grouping, among other factors. The S&P 500 is designed to be a leading indicator of U.S. equities and is meant to reflect the risk/return characteristics of the large cap universe.

S&P/Case Shiller composite Index: This index is a composite of the home price index for 10 major Metropolitan Statistical Areas in the United States. Published monthly by Standard & Poor's, it uses the Karl Case and Robert Shiller method of a house price index using a modified version of the weighted-repeat sales methodology which is able to adjust for the quality of the homes sold, unlike simple indexes based on averages.

U.S. ISM Manufacturing Index: This index is based on surveys of more than 300 manufacturing firms by the Institute of Supply Management and monitors employment, production inventories, new orders and supplier deliveries. The Institute creates a composite diffusion index that monitors conditions in national manufacturing. Investors can use the index to obtain insight into national economic conditions: higher corporate profits are likely to lead to increases in equity markets.

Investors should consider a Fund’s investment objectives, risks, charges and expenses carefully before investing. The prospectus or, if applicable, summary prospectus contains this and other important information about the Hatteras Fund and may be obtained by calling 866.388.6292, or visiting hatterasfunds.com. Read it carefully before investing.

Safe Harbor and Forward-looking Statements Disclosure

The opinions expressed in this report are subject to change without notice. This material has been prepared or is distributed solely for informational purposes and is not a solicitation or an offer to buy any security or instrument or to participate in any trading strategy. The opinions discussed are solely those of Hatteras and may contain certain forward-looking statements about the factors that may affect the performance of the illustrative examples in the future. These statements are based on Hatteras’ predictions and expectations concerning certain future events and their expected impact, such as performance of the economy as a whole and of specific industry sectors, changes in the levels of interest rates, the impact of developing world events, and other factors that may influence the future performance of the illustrative examples. Hatteras believes these forward- looking statements to be reasonable, although they are inherently uncertain and difficult to predict. Actual events may cause adjustments in portfolio management strategies from those currently expected to be employed. It is intended solely for the use of the person to whom it is given and may not be reproduced or distributed to any other person. The information and statistics in this report are from sources believed to be reliable, but are not warranted by Hatteras to be accurate or complete. Past performance does not guarantee future results.

No investment is risk free, loss of principal is possible. Equity values fluctuate in price so the value of your investment can go down depending on market conditions. Alternative investments involve specific risks that may be greater than those associated with traditional investments. There can be no assurance that any investment will meet its performance objectives. These investments may not be suitable for all investors.

Hatteras Funds are distributed by Hatteras Capital Distributors, LLC, an affiliate of Hatteras Investment Partners, LLC Hatteras Capital Investment Management, LLC, and Hatteras Alternative Mutual Funds, LLC by virtue of common control or ownership.

HF 03-2014-05