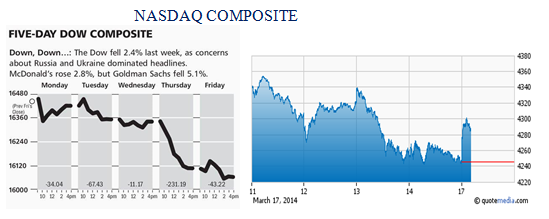

Stocks were buffeted last week on the outcome in Ukraine (well founded), growing concern that the world does not know what happened to that missing Malaysian airliner, and of course, the ever-present worries about the global economy –especially in light of renewed concern over China, both its economy and its banking system.

As the charts above illustrate all of this together created the background for stocks to pull back, which they did to the tune of greater than 2% for both the Dow Jones Industrial Average & the NASDAQ Composite.

The Markets & Economy

The news on the economy is up one day (today for instance), but down on other days such as the retail sales report from last Thursday. Today’s strong opening in the stock market (up over 200 points this morning) is a relief rally caused by no further Russian military action in eastern Ukraine (so far) as well as the better than expected report this morning on industrial production.

Of course, this morning’s report was influenced by renewed automobile production, which only served to bloat the dealer’s inventory lots further, but for this morning it is viewed as a positive.

In my view, substantively, nothing has changed. The global economy is threatened by a no-growth picture in Europe and a disappointing growth picture from China. The data in China is so soft that the authorities there have continued to allow the Yuan to weaken. Today it is back to levels which prevailed nearly one year ago. So here we have another country which tries to fix economic problems by weakening its currency.

This is bad news for Europe whose Euro is perversely stronger this year as the ECB along with the Bank of England is viewed to be the most hawkish in their monetary policy. I say this is perverse because Europe is a no-growth basket case which is flirting with deflation. Given its double digit unemployment, growing reliance upon the government sector which means high taxes to redistribute income and squelch growth, the prospects for Europe remain dark.

Here at home, interest rates have fallen and a general recognition of our virtual energy independence has given support to stock prices even as our economy is viewed to be slogging along at a growth rate of 2% plus or minus.

As I have said now for years this slow-growth economy, given the US has the reserve currency of the world’s economy along with our very financially strong corporate sector, is allowing stock prices to hold in there despite the uncertainties which have brought down markets in Asia including Japan, Europe and, of course, the emerging markets. In an uncertain world, America, despite weak leadership is still viewed as a safety zone for investors. For that reason, I had to laugh last week when it was reported that Russian oligarchs were moving their money out of the dollar.

All I can say to that is “good riddance”. Let them invest in their ruble and see what the world looks like as sanctions are applied to their very weak economy. An economy which is totally dependent upon Europe to sell its energy to. I sincerely doubt money is returning to Russia but rather is investing in US treasuries (overseas), gold and perhaps the Swiss Franc. All of which are traditional safe havens in times of uncertainty.

What to Expect this Week

All of the items mentioned above will still be in play. Thus there will be watching and waiting. In addition, the Federal Reserve Board is meeting this week, with an announcement on Wednesday as to their updated reading of the economy. No doubt they still see us on track, but those forecasts like previous ones should be ignored.

The Fed wants two things:

· It wants to continue to withdraw from the ill-advised quantitative easing policy and

· It also wants to support the financial markets in every way possible through assurances of extended promises of lower rates as the risks to the economy are, if anything, increasing and not diminishing.

Thus, how those two policies are paired together will likely determine the market’s reaction which in itself could be overtaken by many of the other events discussed above.

As far as our weekly look at the Economic Cycle Research Institute’s leading indicators, they showed an improvement last week, but still indicate that the economy is drifting along. I hesitate to think where we would be if not for the continued renaissance of America’s energy infrastructure. The irony, of course, is that this was accomplished in spite of government policies and not because of them. Taxpayers should remember this.

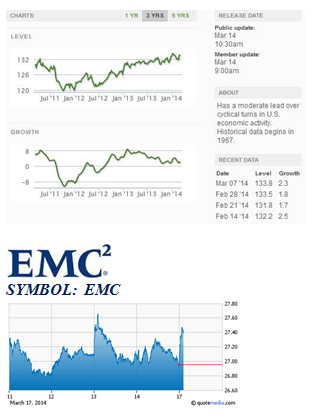

Shares of EMC are trading at new 52-week highs this morning after several Wall Street firms spoke positively last week about the Company’s growth prospects and valuation. We have believed for quite some time that shares of EMC are undervalued given the growth of its cloud computing operations and its 80 percent ownership of VWWare. Even though the stock is making new highs, we contend there is still plenty more upside for shareholders.

As cloud computing becomes more prevalent in the smartphone, tablet and laptop markets, EMC will be there to grow much faster than their large-cap technology competitors. The Company has been taking market share in the past two quarters and we look for this trend to accelerate in 2014. Also, we would not be surprised if management were to change its capital structure concerning its holding in VMWare, which would be a positive for EMC shareholders.

The shares of EMC still trade at a P/E ratio of just 12, which we do not believe is justified given its growth opportunities, strong cash-flow generation and experienced management team. After underperforming the market in the last 12 months, we believe that shares of EMC are primed for significant outperformance for the next 2 years. We expect the Company will exceed earnings estimates over the next several quarters which will lead to a $35 share price within the next 12 months.

SYMBOL: VOD

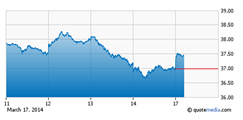

As we discussed last week Vodafone has agreed to purchase Spanish cable operator Ono for $10 billion, which will allow the Company to bundle its wireless offerings with broadband and television. We believe this deal makes sense as Vodafone focuses its operations in Europe. Ono is one of the last stand-alone cable operators in Europe and Vodafone’s financial strength allows them to acquire these assets before their competitors have the opportunity.

Shares are trading higher this morning following the announcement, and we did add to our position last week due to the weakness in the share price. We expect Vodafone will be able to generate more savings than its estimated 2 billion euros, as it now focuses on combining the two companies. Despite press reports to the contrary, we believe that AT&T is still looking at possibly acquiring Vodafone in the future. Shares of Vodafone are undervalued, and we expect the shares to trend higher now that the deal with Ono has been announced.