Since the global financial crisis, economic recovery worldwide has been slow. Over the last three years, annual gross domestic product (GDP) growth in the U.S. was limited to 2.1%, significantly below its long-term average of 3.3%. In this low growth environment, for a majority of companies, churning out high earnings-per-share (EPS) growth rates, either through top-line growth or margin expansion, has become increasingly more difficult. At the same time, the markets are at all-time highs, with multiple-expansion driving most of the rally. Expectations are high and everyday investors and Wall Street analysts alike have adopted a “show me” attitude. The consequence for a disappointing report could be severe. To appease Wall Street, corporate managements are pressured to do everything in their power to deliver strong earnings numbers. There are a wide range of possible accounting gimmicks that could be deployed. Some examples are premature recognition of revenue, aggressive capitalization of expenses, exaggerating current expenses/losses to create cookie jar reserves, classifying one-time gains as earnings from continuing operations and hiding debt in unconsolidated subsidiaries.

A more commonly used “garden-variety” type of technique is accruals management, where accountants increase or decrease the level of financial statement accruals (such as accounts receivables, inventory, accounts payable, deferred revenue, accrued liabilities and prepaid expenses) in order to reach a desired level of profit. Earnings achieved through these types of accounting manipulations are low quality. Looking at the level of accruals, which represent the difference between net income and cash flow from operations, is a standard way to detect earnings management. If cash flow is less than net income, then the difference can be found in an accrual account, such as inventory. One fundamental property of accruals is that they will reverse over time. Specifically, future earnings for companies with built-up accruals will be suppressed when those accrual items invariably start to unwind. Eventually, companies are forced to make up earnings shortfalls with real cash earnings, or suffer write-downs or even management shakeup.

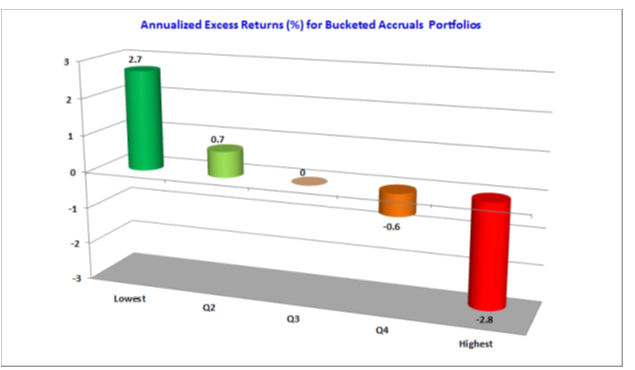

High quality earnings are both sustainable and repeatable. They should be based on consistent reporting choices and backed by actual cash flows. Academic literature (Sloan 1996; Richardson et al. 2005) shows stocks with disproportionately wide gaps between cash flows and reported earnings have lower future returns. Our own research confirms these findings. Stocks with the lowest accounting accruals outperformed their benchmark by 2.7% per year between 1993 and 2013. On the other hand, stocks with the largest level of accruals underperformed the universe by 2.8% (Exhibit 1).

Exhibit 1

Source: Columbia Management Investor Advisers; Notes: stock returns were weighted by the square root of market-capitalization. And financial stocks were excluded from this study. The investment horizon is six month. Past performance does not guarantee future results.

In the post crisis bull market, and especially in the last three years, the quality of earnings has not been much of a focus for investors. However, without many options on the table to meet Wall Street’s high earnings expectations and at higher valuations, some companies are more likely to turn to more aggressive accounting maneuvers. We all remember what happened to companies like Sunbeam, WorldCom and Enron during the go-go days around the turn of the millennium. In today’s environment, even if the gimmickry we see is not of the scale of those examples, active investors who closely monitor the quality of earnings issues should still be rewarded for their efforts.

References:

Richardson, S., R. Sloan, M. Soliman, and I. Tuna, 2005, Accrual reliability, earnings persistence and stock prices, Journal of Accounting and Economics, 39, 437–485.

Sloan, R., 1996, Do stock prices fully reflect information in accruals and cash flows about future earnings? The Accounting Review, 71, 289 – 316.

Disclosure

The views expressed are as of 3/10/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

876392