The post-2009 stock market upswing now qualifies as only the sixth cyclical bull market since 1900 to last five years or more. Life expectancies at such an advanced age are limited; only three of the previous five-year-old bulls lived to see a sixth birthday. Many media and market pundits seem to believe a rising age somehow leads to rising life expectancy. The consensus opinion that a new secular bull market has begun is much more confident today than at the bull’s first, second, third or fourth birthdays.

For those who doubt the impact of easy money on asset prices, consider that three of the six cyclical bulls that reached the five-year milestone occurred under the reigns of Alan Greenspan and Ben Bernanke (with Janet Yellen receiving partial credit for her unblemished performance out of the gates). Incidentally, Greenspan was also present the final few months of yet another five-year bull (August 1982 through August 1987).

While the Fed has only publicly endorsed the stock market wealth effect in the last few years, the past 30 years’ experience suggests there’s been a much longer reliance on this policy transmission mechanism. The danger today in relation to previous old-age bulls is that the public has come to fully understand—and rely upon—the Fed’s intentions. The element of surprise was once a valuable (not to mention free) policy tool, one that the hyper-transparent Yellen Fed seems set to squander.

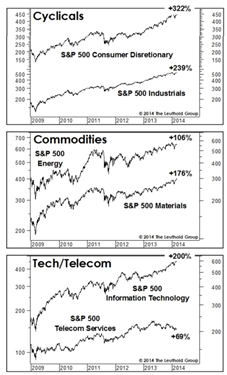

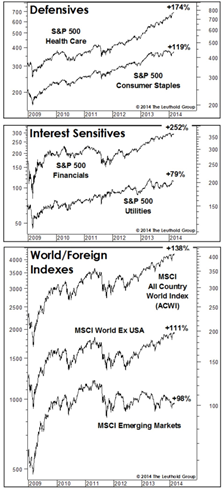

The post-2009 experience lends credence to the Wall Street wisdom that stock market leadership rarely repeats itself in back-to-back bull markets. The 2002-2007 cycle was all about the Emerging Markets boom and its impact on commodities. During the current bull, the lowly S&P 500 Consumer Staples sector has beaten both the MSCI Emerging Markets Index and S&P 500 Energy sector, although the S&P 500 Materials has essentially matched the S&P 500 off the 2009 lows (+176% versus +177%).

From both a geographic and sector perspective, the best bets have been U.S.-based “traditional” (rather than commodity-oriented) cyclicals, with the S&P 500 Consumer Discretionary and Industrials scoring price gains of +322% and +239%. Financials are well ahead of the S&P 500, although most of that gain was booked in the bull’s first year.

Technology and Health Care (the highest ranking sectors in our group work) have been essentially market performers in the bull’s first five years. Technology’s mere 200% price gain is a disappointment on a beta-adjusted basis.

On the heels of the Oscar season, our “Bull Market Achievement Award For The Sector Overcoming A Frugal Future Prophesied By The New Normal Hypothesis” goes to: Consumer Discretionary.

Bulling Through the History Books

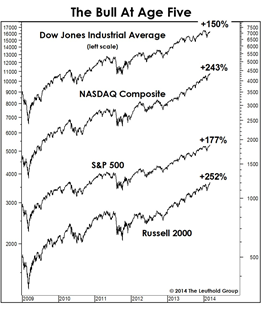

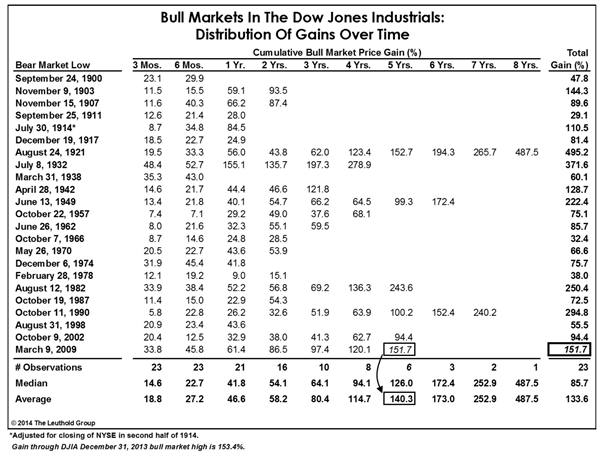

The table below is reserved for special birthdays, like the bull market’s fifth one on March 9th. This milestone—along with the Dow’s +150% cumulative gain—has been matched or exceeded only five times since 1900.

The current bull will move into even more rarified territory if it manages to last through the end of this month. Remember, the last cyclical bull market lasted five years to the day (October 9, 2002 through October 9, 2007), and the 1982-1987 bull topped out just two weeks after its fifth anniversary. This bull is poised to become the fourth longest on record.

The Dow Jones Industrials’ bull market gain of +150% is well ahead of the long-term median (+86%) and average (+134%), and places the 2009-to-date move as the sixth-best all time. Improving on that historical position will be a challenge; it will require a move above Dow 21,000 (to match the +222% gain of the 1949-1956 bull market).

The table below is not an actuarial guide to bull market life expectancy, and we wonder if the severe market decline in mid-2011 reset the bull’s internal clock. However, even if the 2011 decline—which was only –16.8% on the DJIA—is considered a full-blown cyclical bear, the ensuing bull market which commenced on October 4, 2011 is already almost two-and-one-half years old. Only ten of the 23 cyclical bulls shown below celebrated a third birthday. Either way, time is not on the bull’s side.

Doug Ramsey is Chief Investment officer of The Leuthold Group. Based in Minneapolis, The Leuthold Group is recognized as a pioneer in tactical asset allocation, with a flexible flagship strategy that has a 25-year track record. The firm’s investment philosophy stresses quantitative measures of value combined with recognition of fundamental and technical trends for an investment approach that is disciplined, unemotional, and at times contrarian. The Leuthold Group is majority employee-owned. Its investment arm is Leuthold Weeden Capital Management.

© 2014 The Leuthold Group