Markets waited all week for the jobs report for February. After its release the data continued to be mixed at best.

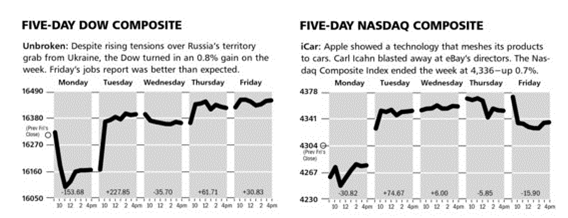

As the charts above illustrate, markets didn’t do much last week as the events in Ukraine and concern over the global economy weighed down sentiment. For the week, both the Dow Jones Industrial Average as well as the NASDAQ Composite racked upmodest gains of less than one percent.

The Markets & Economy

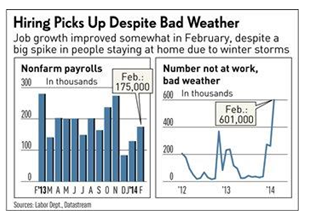

The good news from last week’s jobs report (see chart next page) was that weather oddly didn’t play a role in the data as 175,000 non-farm payroll jobs were created. This resulted in the unemployment rate RISING to 6.7%.

The bad news is just about everything else contained in the report. Average weekly earnings showed their slowest growth rate in 5 years. Over the past year, earnings are higher by just 1.3%. Given higher taxes and expenses for fuel etc., this will hardly cut it for the economy as we head into the spring. Hours worked are actually dropping due to the jump in part-time work due to Obamacare etc…

What this means quite simply is that the difficulty you are reading about in the consumer sector, whether it be retail sales or consumer sentiment in general, is based upon this background and it is not likely to change suddenly should this winter weather ever end.

Additionally, events around the world starting with the Ukraine and its impact on Europe, or China, which is so concerned about its growth rate (and perhaps terrorism at home) that it has been causing the value of its currency to fall over the past month, are adding to concerns. This is putting a damper on economies which export to China as well as increasing concern that China is once again manipulating (it never stopped) its currency. It appears that China has now joined Japan in devaluing their currency as a way of combating economic weakness at home.

All of this is more proof that 2014 will be another year of 2% growth, give or take. This will result in more calls for the government to do something, but people must come to realize that “something” is in many cases the reason the global economy cannot get going. Time to lessen the role of government spending, taxing and regulation and allow incentives to create the organic growth needed to truly change the direction of the economy. Under the current circumstances, accelerating the efforts to develop and export our natural gas to Europe would help so many problems but the Obama administration, at present, just doesn’t see it this way.

What to Expect This Week

Few earnings reports will rattle the markets, and the economic calendar calls for an update on retail sales towards the end of the week. Don’t expect much positive news there.

As a result, the day-to-day trading will hinge upon news coming out of Europe and perhaps the growing concern that terrorism was involved in the loss of the Malaysian airliner. Don’t expect anything positive to come out of either of these issues.

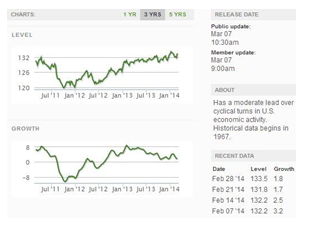

Finally, the “better” than expected payroll report has given renewed hope to the bulls on the economy, but as one can see from the weekly report from the Economic Cycle Research Institute, there is little to get optimistic about. The lackluster trend, implying a slow growth economy, remains intact. I suspect that what you see is what you will get for some time.

As you know, investors should cheer that this economy is neither collapsing nor approaching anything resembling a breakout year. Higher dividends & earnings per share (through buy backs) remain the foundation for this bull market.

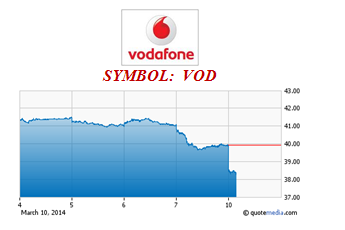

It has been reported that Vodafone has increased its takeover offer for the Spanish cable operator Ono, in an attempt to acquire the Company before its planned IPO. Ono is holding its annual meeting on March 13th, at which management plans to present its intention to sell shares in an IPO. Vodafone has been meeting with large shareholders and has offered to buy the company for $9.7 billion, although no final agreement has been reached.

This caused a sell-off in the shares of Vodafone on Friday and again this morning as some feel the Company will have to over pay for Ono. Some investors think it might make Vodafone less attractive to potential buyers itself, most notably AT&T. This story is going to stay in the forefront this week especially until Ono’s annual meeting on Thursday.

We believe this weakness offers an excellent buying opportunity and are adding to our position at these levels. Vodafone has been buying up European cable assets so that they are able to bundle phone, internet and television services to all of their customers and Ono is one of the few assets still available. The landscape in the European telecommunication/media arena is changing quickly, but we believe the value of Vodafone assets are worth significantly more than they are currently trading for.

We did receive the cash portion of the Verizon Wireless deal in our accounts last week, which completes the transaction. We believe that buying more shares of Vodafone is an excellent use of the cash given the weakness of the past couple of days. We expect the shares of Vodafone will be trading for more than $50 by the end of this year.