How Can You Find an Expert Whose Decisions You Can Trust?

Recently a family member visited the doctor to determine if she needed her gall bladder removed. Since she’d been having some pain, we assumed the answer would be “yes.” But, of course, we wanted an expert opinion, so we went to a surgeon that has done more than 6,000 removals.

Why is an expert good for this situation but, as I have written before, may not be best for long-range stock market forecasts?

Turns out this issue has been the subject of much research and, not surprisingly, of much debate.

On the one side are the Behaviorists, who believe that human nature causes all kinds of biases that result in our intuition about future actions being faulty. On the other side of the seeming divide are those who respect experts and believe in Naturalist Decision Making (NDM).

The NDM believers base their beliefs on studies of experts, such as surgeons, nurses, and firefighters. Each of these professions is often called upon to make split-second decisions that save lives when correct.

In contrast, Behaviorists have focused their research on people who make a living forecasting and predicting, such as economists, market gurus, stock pickers and political consultants. You know… the same people who populate the “expert” panels so commonly assembled and quoted by the media.

I’ve cited many of the Behaviorist studies in the past. A couple of new ones that have come to my attention:

1) Nobel laureate, Daniel Kahneman, in his 2011 book, Thinking Fast and Slow, reports on a study made with fellow Behaviorist, Richard Thaler, of 25 wealth managers that were employed by a financial firm that provided financial advice and other services to very wealthy clients. The study found that based on eight years of results in choosing investments there was no relationship between an advisor’s performance one year versus the next – none.

2) Phillip Tetlock, in his 2005 book, Expert Political Judgments, reports on his University of Pennsylvania study of over 80,000 predictions made by 284 people who made their living “commenting or offering advice on political and economic trends.” Kahneman summarized the results of the Tetlock study in his own book: “The results were devastating. The experts performed worse than they would have if they had simply assigned equal probabilities to each of the three potential outcomes. In other words, people who spend their whole time, and earn their living, studying a particular topic produce poorer predictions than dart-throwing monkeys…”

How does one reconcile these results from the near opposite outcomes found in the NDM studies? And what can we learn from that reconciliation in managing investment portfolios?

Turns out the two leaders of the opposing factions, Kahneman for the Behaviorists and Gary Klein for the students of NDM, co-authored an article titled “Conditions for Intuitive Expertise: A failure to Disagree,” published in the September 2009 issue of American Psychologist. They agreed that experts can be trusted when they act within an orderly environment. Firefighters, surgeons, nurse practitioners, and even poker players all act within an orderly environment, that is, one with definable rules that can be learned from sufficient practice consistent with a statistically sufficient number of occasions. In other words, they have to be in an environment where there are limited options with feedback of definable outcomes and there has to be the opportunity to learn from a very large number of situations.

Long-term predictions of a company’s fortunes or the stock market are not done within such an environment. Because of the necessity for feedback on the outcome from a large number of events, long-term forecasts usually fail because there are not enough examples to statistically base a prediction.

A psychologist can get plenty of practice interpreting clues to immediate patient behavior from his or her many client sessions, but has little ability to forecast the future life experience of those same limited number of patients. Similarly, though, a market forecaster may have little experience to draw on to predict another depression, while having considerable experience knowing what to expect over the near term in the face of often repeated patterns of investor behavior.

What is your financial advisor trying to do – create a portfolio for a distant future or respond to the present market environment? These studies from both camps – Behaviorists and NDM adherents – suggest that focusing on the latter may be the activity for which the advisor can be most trusted.

A second finding of the collaborative effort between the Behaviorists and the NDM school was that when faced with an irregular environment, like the financial markets, relying on quantitative algorithms will usually outperform human judgment. They both acknowledged, however, that the effort to get people to use mechanical methodologies instead of human judgment was likely to evoke substantial resistance. How true!

What does this mean you should do when looking for a financial expert to trust for your investments? Here’s my list culled from these studies of what’s necessary (in addition to the usual suspects always talked about – fiduciary integrity, sound financials, a clean regulatory history, efficient operations, and clear reporting):

1. Have a great deal of experience – a chess master, and most other sophisticated endeavors, requires 10,000 hours of practice. That’s about 5 years at 40 hours a week with no time off for vacations.

2. Because the financial markets are not “regular,” the expert should be focusing on methodologies that happen often enough that a statistically significant result can be obtained. Rolling 20-year studies are often used by buy-and-hold advisors to justify their approach. Even if you go back to the turn of the last century, these 20-year studies can only roll forward 103 times. And in your investment lifetime, how many have occurred? In contrast, dynamic risk management relies upon testing of short-term phenomena that occur with a regularity and frequency that allows for statistically significant results. It does not guarantee positive results, but it puts the probabilities on your side.

3. Rather than relying on investment committees to make day-to-day buy and sell decisions, as do most mutual funds, or a hot stock picker in the latest bull market, investors would be better off, in the very irregular financial markets, to rely on asset managers that trust statistically sound, quantitative (mathematical, computerized) models.

“Experts are a dime a dozen,” some people say. And it is certainly true that every day we are buried under an avalanche of opinions from people assembled by a voracious media. Often, these are opinions generated by people with impressive credentials that are polar opposites.

What’s an investor to do? Hopefully, the simple test outlined above – find one experienced with handling a large number of replicable events or, if in an irregular environment, reliant on short-term, statistically significant algorithms – will prove helpful in finding an expert upon whose decisions you can trust.

Flexible Plan has been in business for 33 years. Throughout that long history it has managed exclusively based upon rigorously tested, quantitative, dynamic risk management strategies. We believe we are the asset management “expert” for our clients and their advisors, putting the probabilities of investing on your side.

Hopefully, we’ll do as well with the doctor and the gall bladder…

All the best,

Jerry

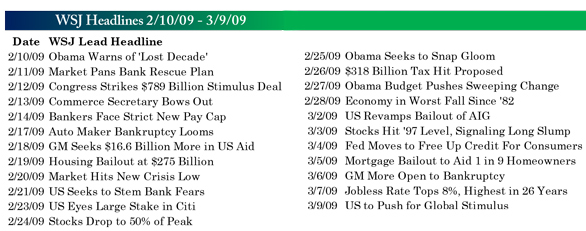

P.S. The stock market rally marked its fifth anniversary (sixth longest and fourth largest of all time) with a very different economic and technical environment than existed at its start back in 2009. As the headlines listed below make amply clear, it was a very dire time for our nation’s economy and markets. Studies show that the average investor had lost about 34%, and General Motors was still $16 billion short of the money needed to meet its obligations. On the charts, we were way below the 50-day and 200-day moving averages and it would be difficult for either technicians or fundamentalists to get a buy signal until some signs of life appeared.

Source: Bespoke Investment Group

As is usually the case, the trend-following signals were alerted to the buying opportunity before most investors, although even the venerable 200-day moving average did not see a positive cross over until the summer time that year. Of course, stock investors did not cross over to equities over bonds until just a few months ago – what a difference!

While interest rates were in a down trend like they are now, economic reports were uniformly negative. Now they are generally positive (two-thirds of last week’s 21 reports were better than expected). Investor sentiment was negative, today it is moderately positive. Earnings were down considerably and still falling. Now they are rising. One consistency – gold is up this year, just like it was in 2009 at this point in time.

Most of our portfolios, reflecting their underlying strategies, remain substantially committed to equities, largely ignoring, like the market, the Ukrainian crisis, and while I expect volatility to remain at higher levels than last year, we let our quantitative strategies be our guide not our “expert” opinion.