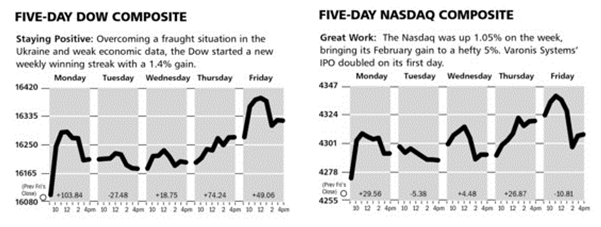

As the charts above illustrate, both the Dow Jones Industrial Average and the NASDAQ Composite moved higher by over 1% to close out the strong month of February which saw stocks regain their January losses.

The Market & Economy

As we highlighted last Monday, the things to keep your eyes on were Russia’s actions in the Ukraine and last Friday’s GDP report for the final quarter of 2013.

We now know that Russia under Putin is still on the prowl for chances to reassemble the old satellite countries of the USSR. The West’s response to their invasion in Georgia of 2008 and the Obama administration’s (led by Hillary Clinton as Secretary of State) attempt to reset relations (that’s code for we let you do whatever you want, just don’t embarrass us) with Russia has produced the weekend invasion in the Ukraine and turbulence in the financial markets.

Naturally this comes at a difficult point for the USA. Just last week the administration announced plans to cut the military to levels not seen since before World War I. Thus at this point our only threat of response is not to attend the G8 economic meeting in Sochi, Russia later this spring.

I am sure Putin is quaking in his boots over that one.

The USA does have things it could do:

Approve the Keystone Pipeline and announce an initiative to export amounts of liquefied natural gas sufficient to neuter the strong leverage which Russia has over Europe in terms of being their supplier.

The Russian stock market has collapsed some 20% the past ten days - keep the pressure on and show the world that America’s lead in energy and technology can slowly but surely put Russia out of business in terms of using its natural resources to gain international leverage.

I am sure there are other measures, but America must regain leadership in the world or the vacuum will be filled and risks will be taken by tyrants that would not have been tried years ago.

What a shame to find Russia back on the stage just years after its economy and even military standing had been degraded some ten years ago. The history books will not look kindly on the West’s leaders which allowed this to happen.

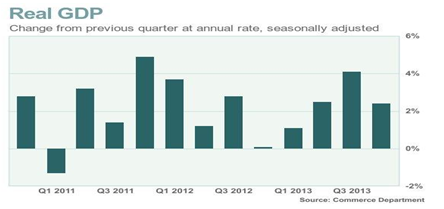

As far as the economy is concerned, last Friday’s report on GDP (see graph below) showed a large but expected downward revision. We ended the year with just a 2.4% annual growth rate which surely will be even lower in the 1st quarter of 2014.

This explains why jobless claims are rising, and the auto and home sectors are weakening. The overall outlook has now been downgraded from where all the happy talk had it at the beginning of the year. The consensus outlook for 2014 GDP growth is now falling fast to my long held belief of 2% plus or minus. In other words the lousy economy of the past four years is repeating itself and now we have Obamacare and higher commodity prices (oil & natural gas) to further dampen hiring and growth.

I must repeat, all of this is known but not reported by the MSM. It is, however, showing up in the drop in interest rates and the strong performance of US equities once again. Rising dividends, mergers and buybacks are all fueling stocks. Equities remain a solid asset class choice despite the perversity that the policies which have led to this are producing lackluster growth and income disparity which is not good for society.

What to Expect This Week

Well, the big enchilada is Friday’s employment report for February. While it is always difficult to predict the number given the ability for seasonal adjustments and other assumptions to mask the true number, this report should be a real stink bomb. Who in their right mind is doing any hiring given the backdrop that Washington DC is providing. Now we have the mess over in Europe and a slowdown in China. A weak report will be ignored due to weather but the markets don’t believe that and bonds are rallying. Soon the Federal Reserve will acknowledge this trend and this will give another shot in the arm to stocks.

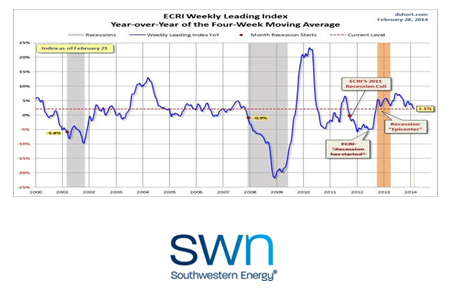

Finally, the weekly report from the Economic Cycle Research Institute (shown below), confirms the trends spoken of above. The economy is now weakening and there seems to be a loss in momentum which is much more serious than the weather or even the near-term disruptions caused by the confusion in the Ukraine. Perversely, this represents more good news for stocks.

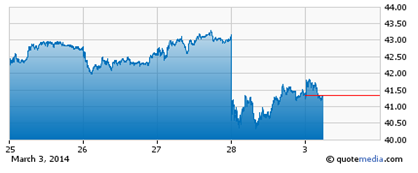

SYMBOL: SWN

Southwestern Energy reported solid fiscal fourth quarter earnings results driven by strong gas production at the Company’s Marcellus Shale properties. The Company earned $0.54 per share, 2 cents higher than consensus estimates and 20 percent higher than last year’s level. Revenues also grew nearly 13 percent to $876 million and easily beat Wall Street’s estimates. During the quarter the Company set records in production, reserves, net income, and cash flows. We believe the business is poised for a better 2014.

The Company experienced 18 percent oil and gas production growth during the quarter. This was led by a 181 percent increase in natural gas production at Marcellus Shale. These strong production numbers more than offset a slight weakness in pricing, although the price of natural gas did get significantly stronger throughout the quarter. Also the management team was able to increase its cash flows, and its superior financial strength gives the Company much more flexibility than its main competitors.

Despite the solid earnings results the shares did sell-off following the release of this earnings report. This is due primarily to exploration at its New Ventures division at the Company’s Brown Dense assets. This is a new project and drilling results have been mixed, although management stated this is common in early stages of drilling. We look forward to hearing more details about this project and expect investors’ concerns are overblown. We will know much more about the Brown Dense assets in coming quarters.

Following the initial sell-off shares have been recovering and we believe any weakness is a buying opportunity. Strong production growth should continue through 2014 and the pricing environment is getting much more favorable for the Company and shareholders. We believe the shares are undervalued at these levels and expect the price to rise to $50 by the end of this year.