"Purer" Gold Exposure for the Long Term Investor

This week we dive into a discussion on the impact of diversifying the financing currencies used to purchase gold. At a high level the primary objective of wanting to diversify financing currencies is to gain a “purer” form of exposure to gold by using a number of different currencies (rather than a single currency) to make gold purchases. For example an investor could decide to use a combination of euro, yen, pounds and dollars to make a purchase. But this raises two questions - firstly what do we mean by a “purer” form of gold exposure and secondly why we would expect increasing the number of financing currencies to have this effect?

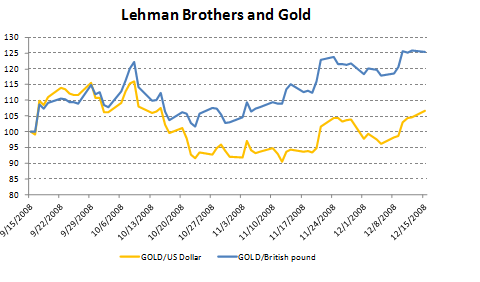

In previous commentaries we have spent considerable time developing the notion that when an investor buys gold they are also explicitly expressing a currency view. When an investor buys gold in US dollars (USD) they are expressing the view that they expect gold to increase in value relative to the USD. Similarly when an investor buys gold in British pounds (GBP) they are expressing the view that they expect gold to increase in value relative to GBP. Or put another way, the investor is exposed to risk factors that drive the price of gold as well as the value of the financing currency and as such the choice of financing currency is an important consideration in the investment process. This can be shown most vividly by comparing the performance of gold/USD and gold/GBP in the three month period after the announcement of the Lehman bankruptcy.

The extreme financial stress experienced post the bankruptcy announcement resulted in a surge in demand for USD assets driven both by the seizing up of the USD funding markets as well demand from investors to hold USD as a safe haven store of value. An investor who funded gold in USD experienced dramatically different performance versus an investor who funded in GBP. Whilst gold buying remained strong from investors looking to hold gold as a safe haven, the surge in demand for USD countered by concerns about the UK’s exposure to the financial sector caused a large shift in the value of GBP versus USD. This was reflected in the gold price where by the middle of December 2008 there was a 19% divergence in the relative performance of gold funded in USD versus gold funded in GBP. Whilst this is certainly an extreme example it does serve to demonstrate how the risk factors that drive the relative value of the funding currency (in this instance both USD and GBP) can dominate the risk factors that drive the relative value of gold. It also hints to the answer for the first question we posed on what we mean by a “purer” form of gold exposure.

When an investor purchases gold they are always, intentionally or not, exposed to the specific, idiosyncratic risks associated with the chosen funding currency. For investors that have a strong view on the currency this might be a desirable feature but for a medium to long term gold investor who may not wish to express a strong directional view on the currency it might be beneficial to look at ways on how to reduce this concentrated currency risk. And this is what we mean by a “purer” form of exposure - exposure to gold where the idiosyncratic risks that drive the funding currency have been diversified by using two or more currencies to finance the gold purchase. Borrowing terminology from portfolio theory the objective of using multiple financing currencies is to diversify unsystematic currency risk leaving only systematic currency risk.

An example that is instructive to look at is a gold purchase that is financed with equal amounts of euro, yen, pounds and USD. Following the logic from our first discussion piece (How to think about the gold price in currency terms) we show that the price change for gold financed in the four currencies can be calculated as follows

Gold/(USD,EUR,YEN,GBP) % Chg = GOLD/USD % Chg – 25%×EUR/USD % Chg - 25%×YEN/USD % Chg - 25%×GBP/USD % Chg

GOLD/USD = USD per Oz; EURUSD = USD per EUR; YEN/USD = USD per YEN; GBP/USD = USD per GBP

By increasing the number of financing currencies, the change in the gold price becomes a function of factors that drive the relative value of each of these currencies as well as factors that impact the relative value of gold. And to the extent that these various risk factors impact the currencies in different ways (i.e. they are not perfectly correlated), the combination of the four currencies achieves a diversification benefit that dampens down the impact of any individual financing currency on the overall gold price.

In summary we believe there are benefits for the medium to long-term gold investor to increase the number of financing currencies used for gold purchases. When an investor buys gold they are explicitly expressing a currency view and to the extent they do not have a strong directional view on the currency it would make sense for them to seek ways to reduce concentrated currency risk and gain “purer” exposure to gold. This can be readily achieved by increasing the number of financing currencies which provides a diversification benefit against the specific risks that drive each individual financing currency. In our next commentary we will look at the impact on the long term performance of gold when purchased using a basket of currencies.