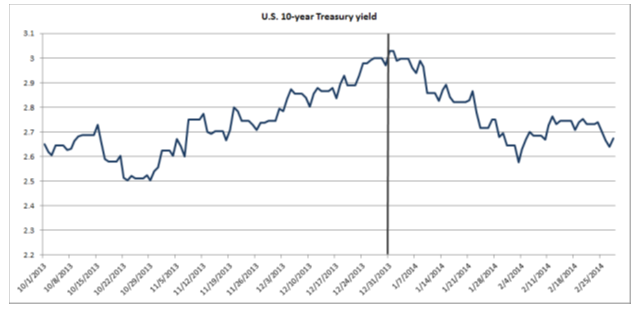

In 2013, both the S&P 500 Index and the yield on 10-year Treasury bonds finished the year at their highest levels of the calendar year. So ended a year when equity markets dominated the return landscape, while bonds and numerous other assets struggled. The environment apparently changed, though, with the turning of the calendar to 2014. In the New Year, bonds have performed quite well, with yields on 10-year Treasuries, as an example, falling from 3.03% to 2.67% so far this year. Stocks meanwhile, have been volatile, yet stand close to unchanged on a year to date basis.

Exhibit 1

Source: DataStream, February 2014.Past performance does not guarantee future results.

There are two good reasons for bond yields to have fallen this year. First, having closed 2013 above 3%, bond yields had reached a level where interest rate risk was no longer over-priced. With valuation back to fair value, at least in the short run, bonds had become a relevant choice for portfolio diversification once again. Second, the economic data have been markedly weaker so far in 2014 than most forecasters expected. Our research on asset class sensitivities to economic activity suggests that in an economy that is both growing and accelerating, like we saw last year, equities perform well while interest rate sensitive bonds, like Treasuries, struggle. When economic growth levels off, the headwinds for bonds subside, which fits the patterns of 2014 so far quite well.

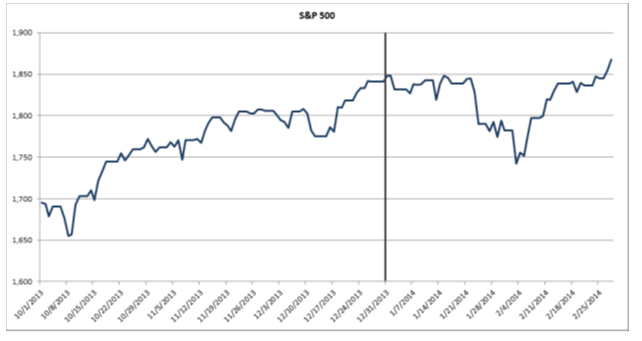

The last two months notwithstanding, we think that investors should hold off on declaring the environment of equity hegemony (see Q1 Investment Strategy Outlook for discussion on equity hegemony) to be finished. Stocks, as measured by the S&P 500, have recently eclipsed their 2013 highs and as of this writing stand in record territory. Bond yields, meanwhile, remain far below their 2013 closing levels. This inconsistency bears watching in the weeks ahead. With bond yields this low, the attractiveness of interest rate risk from a valuation standpoint is once again meager. Should the economic data reaccelerate, we think the recent equity breakout would be validated, and the friendlier environment for bond yields that has defined 2014 so far would be but a memory.

Exhibit 2

Source: DataStream, February 2014.Past performance does not guarantee future results.

This week, several key U.S. economic releases will shed some light on these issues. Personal income, purchasing managers surveys and the monthly payroll report, all bellwether releases, are being reported during the week. Should these data (or subsequent statistics, in fact) portray reacceleration, we would expect further equity market strength but also bond market weakness. Markets, we think, would revert to their 2013 patterns. This remains our central case for the months ahead. Stubbornly low Treasury yields going forward, therefore, would signal that we should rethink our central case. As always, we continue to closely monitor global markets and adjust our investment strategy accordingly.

Disclosure

The views expressed are as of 3/3/14, may change as market or other conditions change, and may differ from views expressed by other Columbia Management Investment Advisers, LLC (CMIA) associates or affiliates. Actual investments or investment decisions made by CMIA and its affiliates, whether for its own account or on behalf of clients, will not necessarily reflect the views expressed. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon, and risk tolerance. Asset classes described may not be suitable for all investors. Past performance does not guarantee future results and no forecast should be considered a guarantee either. Since economic and market conditions change frequently, there can be no assurance that the trends described here will continue or that the forecasts are accurate.

This material may contain certain statements that may be deemed forward-looking. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable.

Asset allocation does not assure a profit or protect against a loss.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Distributors, Inc. All rights reserved.

870002