With the Ukrainian situation very much in focus, Treasury rates moved mostly lower last week. The yield curve exhibited a flattening bias, as longer dated maturities registered the biggest declines. For the week, 10 year treasury yields closed at 2.65%, a drop of eight basis points from the prior week, while two year yields were unchanged at 0.32%. As Gross Domestic Product (GDP) was revised lower to +2.5% from +3.2%, we also learned last week that the economy expanded at a slower pace in the fourth quarter of 2013 than previously estimated, giving the expansion less momentum heading into 2014.

Volatility and uncertainty are expected to remain elevated yet again this week, with a host of economic data, geopolitical tensions, and Federal Reserve speakers confronting financial markets. The most important economic release will occur on Friday with the monthly payrolls report. After a string of disappointing reports, economists have lowered their expectations for the February jobs release to just +150,000, as weather continues to negatively impact economic data. Additionally, President Obama will present to Congress his 2015 fiscal budget.

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD; Source: Bloomberg, Thomson Reuters and Castleton Partners

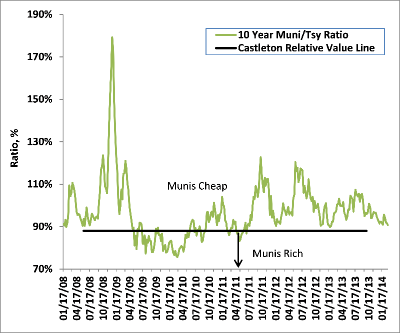

Ratio of 10Y Muni Yield to 10Y Treasury Yield; Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

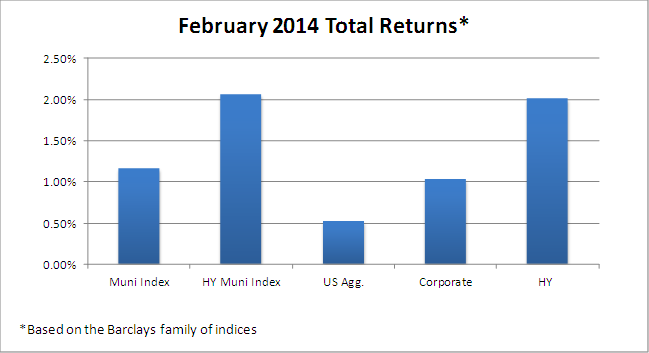

Fueled by a rallying US Treasury market and minimal supply, tax exempts once again registered strong price gains across the maturity spectrum. Continuing a 2014 theme, municipals outperformed treasuries, investment grade corporates, and mortgage back securities on the week—remaining the top-performing sector in fixed income year to date. In fact, over the last 6 months, the 10 year maturity sector of the muni market has returned +5.53%, according to Barclays Capital. Over the same time period, the Muni/ Treasury ratio has declined to 90.6% from 105%. For the week, ten year muni yields closed at 2.40%—a yield drop of ten basis points from the prior week’s close.

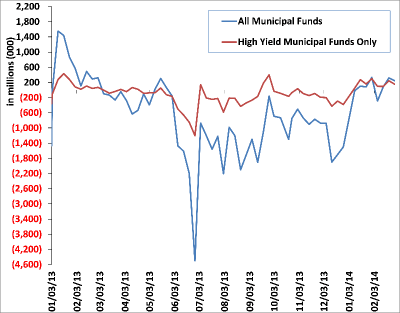

Perhaps the most important contributor to tax exempt outperformance in 2014 has been the resurgence in demand. Mutual fund flows, after closing out 2013 with 33 consecutive weeks of withdrawals, were positive yet again, as $247 million of new money hit the market. Fund flows have now been positive for six of the nine weeks to start the year. Perhaps the biggest reason for the change in demand: taxes. This year, high earners are facing tax bills that, for the first time, include the significant increases in marginal tax rates passed last year, as well as the 3.8% tax on investment income (except on tax exempt debt) to help pay for the new health care law. Castleton detailed those changes for clients in March 2013. Factoring in state and local taxes, many filers are crossing the 50% tax bracket.

With tax exempt yields having declined nearly 60 basis points since December, high yield tax exempts have seen renewed interest as well. Fund flow data in this area of the muni market has also reversed to the positive, as the sector exhibits strong relative value comparisons to taxable high yield debt. Per Barclays Capital, the high yield market has produced absolute returns of over 5% YTD, besting the +2.74% return in taxable high yield. Puerto Rico credits—despite the recent credit downgrades—continue to dominate trading in the high yield market, with yields declining an additional 10-15 basis points from the prior week. With a new $3 billion loan expected next week, the Commonwealth continues to benefit from its investor webcast on February 18th highlighting recent economic and fiscal reforms. A new tax exempt loan for United Airlines (B2/B), priced last week, received over a billion dollars of orders for only $176 million in bonds, according to Citigroup, the lead underwriter of the deal!

Tax exempt supply finally picks up this week, with over $5 billion expected to price. Relatively large and liquid names such as a $900 million loan for Texas Transportation (Aaa/ AA+) and a $740 million deal for the State of Maryland (Aaa/AAA) lead the resurgence.

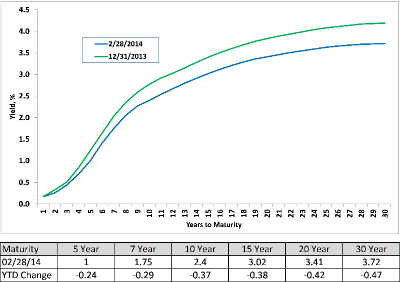

AAA Municipal Market Data (MMD) Yield Curve; Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data; Source: Lipper AMG Data

Taxable

Investment grade credit tightened further last week and hit post financial crisis tights, with spreads narrowing, on average, 2-4 basis points against a rallying treasury market. Supply was again the primary theme in taxable markets, as over $37 billion of new debt was priced—raising February’s total to $118 billion (Bloomberg). The largest offering was an $8 billion loan from Cisco (A1/ AA-), the largest corporate offering to hit the market since the $49 billion Verizon offering last September. With investment grade corporate bond mutual funds receiving $2.4 billion in new cash, other high profile issuers, such as Colgate Palmolive (Aa3/ AA-), PepsiCo (A1/ A), and Goldman Sachs (Baa1/A) issued debt as well.

With the corporate bond market returning, on average, +2.87% so far in 2014 (Barclays), we list recent ten year spreads on some of the top trading tech names following the recent Cisco loan:

| Issuer | Rating | 10Y TSY Spread |

| Apple | Aa1/AA+ | +70 |

| Cisco | A1/AA- | +86 |

| Aa2/AA | +64 | |

| IBM | Aa3/AA | +87 |

| Microsoft | Aaa/AAA | +65 |

| Oracle | A1/1+ | +75 |

|

THE FOLLOWING NOTES AND DISCLOSURES ARE AN INTEGRAL PART OF THIS REPORT: Past performance is not a guarantee of future results. Different investments involve varying degrees of risk, including the risk of illiquidity and the risk that you could lose part or all of your investment. There can be no assurance that the future performance of any specific investment, investment strategy, or product (including those discussed herein or recommended or undertaken by Castleton Partners, LLC) will be profitable, equal any corresponding indicated historical performance, be suitable for your portfolio or individual situation, or prove successful. Charts, graphs and indices are included herein only for reference and do not constitute forecasts of the past or predicted future performance of any investment. Indices are not investments. Due to changing market conditions and other factors the content herein may no longer reflect Castleton Partners, LLC’s current opinions or positions. Nothing discussed herein is or is intended as tax, legal, accounting or personalized investment advice from Castleton Partners, LLC. Should you have any questions regarding the applicability of any specific issue discussed herein we encourage you to consult competent advisers of your choosing. Nothing herein is or is intended as an offer to sell or a solicitation of offers to buy any security. Castleton Partners, LLC’s current written disclosure statement including discussion of our advisory services and fees is available upon request.