Stocks Break Even to End February

Equity markets rebounded from a sluggish start to 2014 to finish February at record high levels. February’s 4.6% gain also pushed stocks back into positive territory for the year; the S&P 500 now stands up 0.3% in 2014.

Economic data slanted somewhat negatively last week, but there were more encouraging indications under the surface. Investors have had difficulty deciphering 2014’s data due to adverse weather sweeping across the nation, a notion that Fed Chairwoman Janet Yellen acknowledged last week in public comments before the Senate Banking Committee. She noted that it would take a “significant change” in the economy for the Fed to change course on its current pace of reduction in asset purchases.

The Conference Board’s measure of Consumer Confidence fell marginally from 79.4 in January to 78.1 in February. This was slightly below expectations, but the report was skewed lower by a sharp drop in the expectations component of the index. Consumers’ view of current conditions jumped 4.4 points, an encouraging sign amid otherwise weak data to start 2014.

On Tuesday, both the FHFA House Price Index and the S&P Case-Shiller Home Price Index indicated that home prices improved in December with each measure rising 0.8% in December. The FHFA index rebounded sharply from a soft November while the Case-Shiller report has weakened somewhat over the past few months. A similar trend is evident in the year-over-year measures.

This familiar refrain of a gradual tapering in housing markets was broken Wednesday, when new home sales surged to an annualized rate of 468,000. This was well in excess of an expected 400,000 figure, and sharply at odds with last week’s sub-par existing home report. Strength in January’s new home sales occurred despite poor weather conditions across much of the country. The largest source of improvement was in the South, which posted a double-digit gain.

The week ended on somewhat of a disappointing note, as fourth quarter GDP was revised lower from 3.2% to 2.4%. This was largely at the hands of personal consumption expenditures, which was moved down from 3.3% to an estimate of 2.6%. Growth also stands sharply lower than the third quarter’s 4.1% gain. The final estimate of fourth quarter GDP will be released March 27.

A Consumer Releveraging Renaissance?

After a long period of deleveraging, there are appearances that consumers are entering a stage of releveraging. The devil is always in the details, though, and this releveraging cycle is likely to play out vastly different than those of previous expansions.

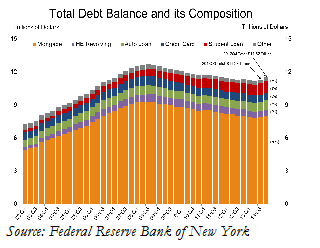

Last week the Federal Reserve Bank of New York released its “Quarterly Report on Household Debt and Credit.” According to the report household debt outstanding increased $241 billion in the fourth quarter, representing the “largest quarter over quarter increase since the third quarter of 2007.”

By category, the largest increase occurred in mortgage debt and student loan debt, which experienced increases of $152 billion and $53 billion, respectively. Those two categories accounted for 85% of the credit growth last quarter.

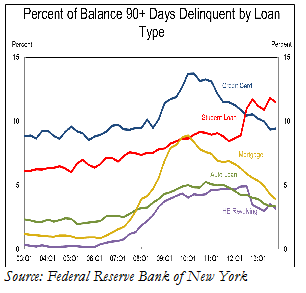

Coincident with the retrenchment of outstanding debt during the past several years was an overall decline in delinquency rates, with one exception – student loans. Delinquencies in excess of 90 days are now above 10%, more than double the rate prior to 2008. This is only expected to continue as a greater number of people pursue higher education.

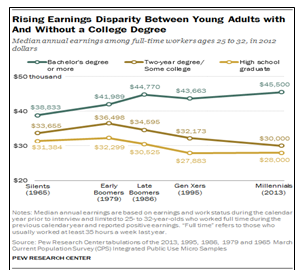

Ultimately, the story of this releveraging cycle is likely to be about student loans more than any other form of debt. Primary behind this trend is the growing wage disparity between individuals with a bachelor’s degree and those with a two-year degree, or high school education. In earlier generations, the gap was modest, but during the course of the past three generations, the earnings gap has become reasonably pronounced.

The Pew Research Center recently released data on median earnings of full-time workers between the ages of 25 and 32. In 1979, people with a bachelor’s degree made an estimated $41,989, compared to $32,299 for high school graduates. By 2013, median earnings for college graduates were $45,500, and, for high school graduates, earnings had actually declined to $28,000.

Source: Pew Research Center

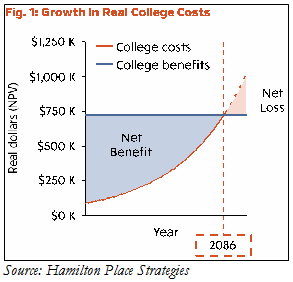

As the cost of a college education has risen rapidly in recent decades, so too has the burden of affording college. It might be easy to assume that we are rapidly nearing an inflection point where the cost to pay is no longer worth the additional lifetime earnings. But, not so fast. Hamilton Place Strategies, a private consulting firm, estimates that the benefits of college outweigh the costs for many decades to come.

The inflection occurs in 2086 by their calculations. At that time, college will cost $181,000 a year in current dollars, or a cumulative $725,000. Projecting that many decades in the future is highly fraught with shortcomings, but it offers a general understanding as to why college costs and ultimately, student loan debt will continue rising.

\

\

Recent leveraging cycles were notably driven by mortgage and credit card debt. This time around, the necessity of a college education is likely to drive more consumers to borrow in order to finance their education, and rightfully so, for the time being. That borrowing will impact consumers’ ability to releverage other areas of their balance sheet, particularly if we continue to see an overall rise in student loan delinquency rates. Investors would be wise to watch the student loan markets closely in the approaching years for any signs that it is placing too great a burden on consumers.

The Week Ahead

A busy week of economic data lies ahead, with personal spending, ISM manufacturing, and the government jobs report highlighting the schedule.

Geopolitics will also remain in focus with Russia’s potential military involvement in Ukraine. Risk assets have retreated throughout the weekend over the threat of conflict in the region.

It is also a busy week on the central bank front, with the ECB and Bank of England meeting. The ECB is expected to cut rates from 25 bps to 10 bps to combat recent disinflationary troubles. Other central banks meeting include Malaysia, Australia, Poland, and Canada.

About Fortigent

Fortigent, LLC delivers a fully integrated and customizable business-to-business outsourced wealth management solution to banks, trust companies, and independent advisory firms. Services include a comprehensive investment platform with particular expertise in alternative investments, a flexible unified managed account program, and consolidated wealth reporting. Fortigent's web-based portal interface allows access to proposal and rebalancing tools, client portfolio reporting and accounting, as well as industry articles, research papers, and other practice management and business development resources.

The information provided is general in nature and is not intended to be, and should not be construed as, investment, legal or tax advice. Fortigent makes no warranties with regard to the information or results obtained by its use and disclaims any liability arising out of your use of, or reliance on, the information. The information is subject to change and, although based upon information that Fortigent considers reliable, is not guaranteed as to accuracy or completeness.

Not FDIC Insured No Bank Guarantee May Lose Value

© Fortigent