Monetary policy is primarily about “gaps” not growth: the Fed is trying to reduce spare capacity in the economy, not bring about a rapid expansion per se.

- Despite concerns over cyclical weakness in labor force participation, the unemployment rate is sending similar signals as most other output gap proxies.

- The output gap improved despite a relatively slow expansion, suggesting weak potential growth.

While it’s far too soon to revise any medium-term views, the activity data in hand suggest a modest downshift in U.S. growth since the end of last year. Our proprietary measure of monthly growth rates, for instance, was up just 2.0% (annualized) in January after an average gain of 2.9% over the previous three months. It’s possible that the slowing reflects cold weather and/or noise in the data, and we will not know for sure for a few more months. Our working assumption is that the firmer growth trend that we saw in the second half of 2013 remains intact.

However, even with modestly slower growth, we think that Fed officials would continue the process of gradually normalizing the stance of policy. The reason is that monetary policy is primarily about “gaps” not growth: the Fed is trying to reduce spare capacity in the economy, not bring about a rapid expansion per se. This is why the Fed’s guidance about the funds rate and the statement on longer-run goals and objectives are both expressed in terms of the unemployment rate, not the pace of job creation. In our view, the steadily shrinking output gap is what put the exit wheels in motion, and there’s little sign that this persistent trend has changed.

Economists think about the relationship between spare capacity and economic growth using a relationship called Okun’s Law. In the form that will be most intuitive here, this equation says that the output gap—which is just a technical name for spare capacity or economic slack—improves when growth is above potential, and worsens when growth is below potential:

Output Gap = β * (GDP growth – Potential GDP growth)

where beta is the Okun’s Law coefficient. The relationship is also commonly written in terms of the unemployment gap—the difference between the unemployment rate and its structural rate.

Okun’s Law is at the center of today’s biggest policy debate. Since the recovery began in the second half of 2009, GDP growth has increased at an average annualized rate of just 2.4%. Before and during the recession, most economists thought that potential GDP growth was greater than 2.5% (based on various forecaster surveys). Thus, the Okun’s Law equation above would have implied a worsening output gap, because GDP growth was actually below potential. Instead, available evidence strongly suggests a large and persistent improvement in the output gap over the last four years.

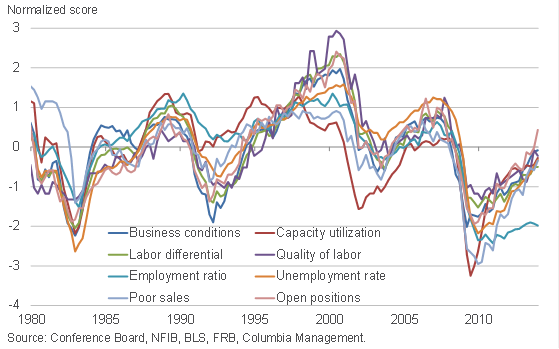

The output gap is only a theoretical variable. But as we have written about before, we can keep track of its likely changes by monitoring a variety of observable proxies. Specifically, we measure the output gap by focusing on eight monthly economic indicators: (1) the unemployment rate, (2) the industrial capacity utilization rate, (3) the labor differential from the consumer confidence survey, (4) the business conditions index from the consumer confidence survey, (5) the quality of labor index from the NFIB small business survey, (6) the poor sales index from the NFIB small business survey, (7) the open positions index from the NFIB small business survey, and (8) a measure of the employment-to-population ratio for the 24yr-54yr age groups (we do not use popular measures of underemployment from the household survey because of short histories and/or methodological breaks in the mid-1990s).

The first chart below shows normalized versions of these variables from 1980 through the present. A few points stand out. First, the variables are highly correlated, suggesting they are measuring the same underlying economic concept. Second, all but the employment-to-population ratio have improved substantially since late 2009. This suggests to us that the employment-to-population ratio may no longer be a good proxy for spare capacity. Third, the unemployment rate is right in the middle of the other indicators. Despite concerns over cyclical weakness in labor force participation, the unemployment rate is sending similar signals as most other output gap proxies.

Exhibit 1: Eight proxies for the output gap

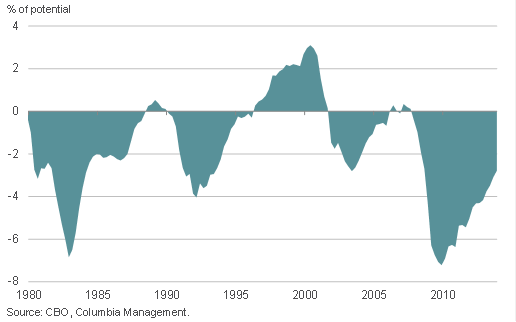

We can use these indicators to create an independent measure of the output gap. The details are somewhat technical, but essentially we capture the common movement of these series with standard statistical techniques. We then translate our data into output gap units by relating them to the average level of the official output gap from the Congressional Budget Office (CBO) over this time period. The next chart below shows our results. We estimate that at the end of 2013 the output gap stood at around -3%. This means that the level of US GDP was about 3% below its potential.

Exhibit 2: Output gap estimate

We can draw a few simple conclusions from our -3% output gap estimate. First, using standard rules of thumb, this figure implies an unemployment gap of 1.5 percentage points (i.e. the unemployment rate is about 1.5pp above its natural rate). Today the reported unemployment rate is 6.6%, and the U6-implied unemployment rate is 7.4%.* Typical estimates of the structural unemployment rate are 6% (Survey of Professional Forecasters) and 5.5% (midpoint of Fed’s central tendency projection). Thus, our 1.5pp unemployment gap estimate looks broadly consistent with other approaches, which put the “true” unemployment rate (adjusted for additional slack in work hours and discouraged workers) in the low-7% area, and a structural unemployment rate in the high-5% area.

Second, potential growth likely slowed in recent years. This is the implication of the Okun’s Law equation above: the output gap improved despite a relatively slow expansion, suggesting weak potential growth. We can use our multi-indicator approach to invert the Okun’s Law equation and infer an estimate of potential. Based on currently-reported GDP figures, this exercise suggests that potential growth may have fallen as low as 1%. We are not sure about the reasons for slow potential growth, but it now seems evident in the data.

Exhibit 3: Potential GDP growth

Third, the output gap has improved enough to begin debates about the appropriate level of the federal funds rate. In the “modified Taylor rule” used by Fed Chair Yellen, an output gap of -3% reduces the warranted funds rate by 3pp. If inflation were at the Fed’s 2% target, this would mean a warranted funds rate +1%. Today’s 1% inflation rate pushes the warranted funds rate down another 1.5pp to -0.5%. Fed officials point to other reasons why the funds rate should remain at zero—especially headwinds depressing the neutral funds rate and the lengthy period stuck at the zero lower bound. These arguments look likely to win the day for the immediate future. But we would expect dissenting voices to get louder as the output gap shrinks further and if inflation picks up at all.

* U6 is a broader measure of labor underutilization which includes unemployed workers as well as discouraged workers and those on part-time schedules for economic reasons. To calculate the U6-implied unemployment, we regress the actual unemployment rate on the U6 rate from 1994-2007, and then apply the estimated coefficients to the currently reported U6 rate.

Disclosure

The views expressed in this material are the views of the author through the date of publication and are subject to change without notice at any time based upon market and other factors. All information has been obtained from sources believed to be reliable, but its accuracy is not guaranteed. There is no representation or warranty as to the current accuracy, reliability or completeness of, nor liability for, decisions based on such information and it should not be relied on as such. This information may contain certain statements that may be deemed forward-looking statements. Please note that any such statements are not guarantees of any future performance and actual results or developments may differ materially from those discussed. There is no guarantee that investment objectives will be achieved or that any particular investment will be profitable. Past performance does not guarantee future results. This information is not intended to provide investment advice and does not account for individual investor circumstances. Investment decisions should always be made based on an investor's specific financial needs, objectives, goals, time horizon and risk tolerance.

Investment products are not federally or FDIC-insured, are not deposits or obligations of, or guaranteed by any financial institution, and involve investment risks including possible loss of principal and fluctuation in value.

Securities products offered through Columbia Management Investment Distributors, Inc., member FINRA. Advisory services provided by Columbia Management Investment Advisers, LLC.

© 2014 Columbia Management Investment Advisers, LLC. All rights reserved.