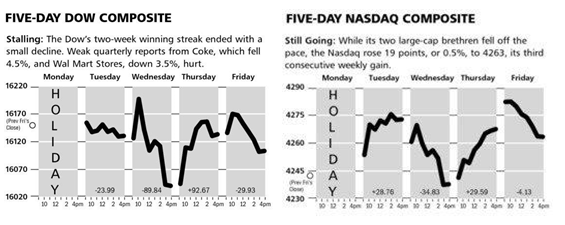

A quiet four days for stocks last week. Between the holiday, school vacations and winter weather; there just were not many catalysts for the stock marker.

As the charts above illustrate, the Dow Jones Industrial Average showed a .3% loss, while the NASDAQ Composite was fractionally higher on the week.

The Markets & Economy

Last week provided more evidence that the economy has lost momentum from the latter part of 2013. Housing starts and mortgage applications have been weak for some time now and it is showing up in inventory of unsold homes - fewer new home starts/sales and, of course, fewer jobs required in the related industries associated with housing which had been viewed as a primary source of growth for 2014.

It is still conventional wisdom that it is the weather which is skewing the economic data, but remember, the disappointing economic reports are seasonally adjusted for the winter months which come every year at this time. Even more telling is that the West, including California, is experiencing very disappointing results and they have a drought to deal with rather than cold weather everywhere else. Thus it seems that it is more than weather at work in the New Year.

In any case that is for the short run the debate which the markets are having. Is the weakness temporary? Will it be made up as the arrival of spring approaches, or have we in fact entered an ill-timed malaise to coincide with the Federal Reserve Board’s tapering policy?

To the extent the talking heads at the Fed have offered their view, it is that things are great and just you wait and see. Of course this is a version of what they always say. Thus in my opinion the stock market is not concerned about a slow growth economy but is actually concerned that the Fed thinks they have still have a solid year of recovery and hence will further adjust their policy (higher interest rates sooner than currently expected). This would be the wrong move at the wrong time. Thus putting at risk our current 2% lackluster economy for 2014 which remains my view for the year.

What to Expect This Week

It’s a full week, and the news from around the world is quite interesting, but so far it has had no impact on markets. Now that there has been a regime change in the Ukraine, it remains to be determined just what the response will be from Russia. Remember in 2008, Putin sent the troops into Georgia to preserve his interests and paid no price. I don’t expect him to simply acquiesce in losing a puppet stake to the West so close to his borders.

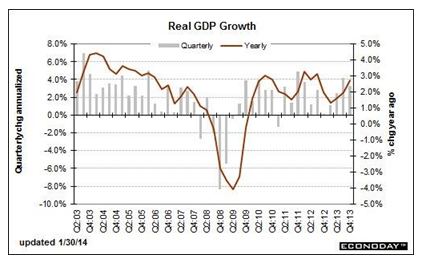

In terms of economics, while there will be several reports on the economy, the one with the most potential to change opinions is the GDP Report for the 4th quarter of 2013. This comes out on Friday this week.

As the graph below shows, this was originally estimated at a positive 3.1%. The current estimate is a downward revision to around 2.5%. Even worse is the opening quarter of 2014, so this report has the potential to force the powers-that-be to stop the “Happy Talk” on the economy and face the music. This year will be disappointing for growth, but another reasonable one for financial assets as the time is pushed out further as to when interest rates will rise.

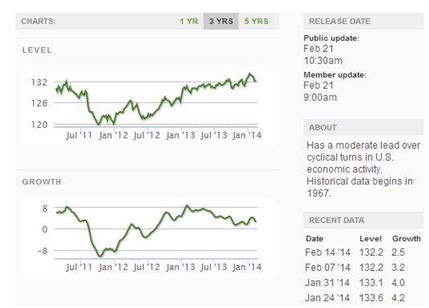

Finally, the weekly look at the chart of leading economic indicators from the Economic Cycle Research Institute, shows more sub-par growth. There is just nothing in their analysis to indicate a renewed bout of growth ahead. This analysis sounds like a broken record, but it beats the garbage out there masquerading as an insightful look into the economic future - much of which forms the foundation for our current monetary policy.

On Friday Verizon announced that it has completed its acquisition of Vodafone’s 45 percent stake in Verizon Wireless in a deal valued at about $130 billion. We have been discussing the merits of this for several quarters, and we are pleased the companies were able to complete the transaction on schedule. We believe the prospects for shareholders of both companies are attractive and look to be long-term shareholders of both Vodafone and Verizon.

As previously announced Vodafone’s shareholders would be receiving some shares of Verizon, retaining shares of Vodafone on a split-adjusted basis and also receiving cash considerations. After completing the transactions, Vodafone’s shareholders received 6 new shares for every existing 11 shares they hold. As a result of the transaction if you owned 1000 Vodafone ADRs, you now have 545 shares of Vodafone, 263 shares of Verizon, and will be receiving the cash considerations in your account by March 4th.

As we have previously stated, we believe this deal makes plenty of sense for both groups of shareholders. Verizon paid a fair price for the Vodafone’s stake in Verizon Wireless, which will allow them to increase profit margins and will be immediately accretive to earnings. Vodafone shareholders now own a much different company with a strong balance sheet and operations throughout Europe. It has been a rumored takeover candidate of AT&T, and we would not be surprised if that happens within the next 12 months.

Management teams of both Verizon and Vodafone are hitting the road to promote the merits of this deal and the new strategic focus of both companies. We believe both of these companies will be attractive investments for the next several years, and both have conservative valuations at these levels.