Stocks soared last week as economic reports showed the global economy was weaker than originally estimated in the last quarter of 2013 and has lost further momentum in 2014. This has acted to support bond prices and lower interest rates.

Thus, stocks as an asset class continue to do well.

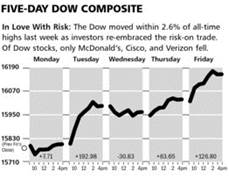

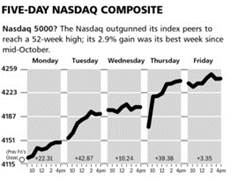

As the charts above illustrate, the Dow Jones Industrial Average gained 2.3, while the NASDAQ Composite moved higher by nearly 3%. The market is telling you that the weaker economic outlook is more important than the potential impact of theFed’s tapering policy, which at this point remains in effect.

The Markets & Economy

Last week’s maiden testimony by Janet Yellen, the new Chairman of the Federal Reserve Board produced no surprises. As expected, she is still working off the assumption that the economy is moving into a higher rate of growth and hence policy movements will dovetail with that (erroneous) assessment.

Clearly, the rally in gold combined with the rally in financial instruments tells you that the financial markets have concluded that growth this year will be disappointing. Of course, the weather will be cited as a problem given that this is now shaping up to be the 3rd coldest winter in the past 100 years. Against this backdrop it is not encouraging to markets to see our leaders from President Obama to Secretary of State Kerry running around the world proposing anti-growth measures to combat global warming.

The markets are speaking loud and clear. The year 2014 will be another “stink bomb” and policy moves from Washington DC in the form of Obamacare and the other misguided recommendations, will just make matters worse. Perversely, this is good for stocks as interest rates remain near zero, and corporations continue to grow profits and return cash to shareholders via dividend hikes and stock buybacks. This remains good for investors, but bad for society, which is why the recent polling show Americans expect the future will be worse. The level of pessimism has moved higher than has been seen in the past several years.Some recovery!

What to Expect This Week

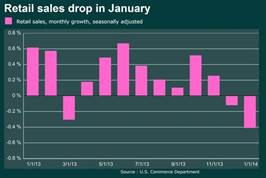

Being a shortened week with Congress out of session, the news flow will be lower than usual. The economic reports from last week’s retail sales number (see chart below) to industrial production to this morning’s NAHB report on housing all paint a rather dismal picture for the near-term. Accordingly, the rally in bonds and even gold might have some life remaining in it. The bigger trend of financial reengineering continues to run in high gear with deals being announced virtually every day.

The weekly update from ECRI shows a dip in their weekly index. The outlook has not gone negative, but it does buttress the notion implied by the other economic reports that the global economy just has no momentum at this point.

![]()

SYMBOL: BRCD

Brocade’s shares are trading at new 52-week highs after reporting solid fiscal first-quarter earnings results last week. Revenues came in at $565 million, which was $15 million higher than consensus estimates, even though they were down 4 percent from last year. Also, earnings per share topped the most bullish estimates at $0.24, which was 14 percent higher than last year. Management was conservative with their guidance for the next quarter, but we look for them to continue to exceed expectations.

Since CEO Lloyd Carney took over at Brocade, the Company has been successful in lowering its cost structure and focusing on its higher margin products. This quarter was no different as the Company’s Generation 5 Fibre Channel products saw a sharp increase in sales, and we expect the sales momentum will continue through 2014. The Company’s software solutions are also gaining traction in the industry, and these products generate significantly higher margins than its legacy businesses.

Management also remains aggressive with its share repurchase plan. The Company bought back 16.7 million shares in the fiscal first quarter, and has repurchased an additional 3.3 million shares since the end of the quarter. This has reduced the number of shares outstanding by over 3 percent from last year. We believe this is an excellent use of the company’s capital.

Shares of Brocade have rallied since the release of this earnings report, and we believe the shares are stillundervalued. Takeover speculation has died down and the shares now trade on the current fundamentals. As Brocade’s management team continues to exceed expectations, more investors will believe the turnaround story at the Company. We are raising our 12-month price target to $14 per share.

![]()

SYMBOL: PES

Pioneer Energy Services reported slightly better than expected fourth-quarter earnings results last week, and indicated that business conditions are improving. Revenues were 5 percent higher than last year at $238.2 million. The Company did lose $0.04 per share, but that was an improvement over last quarter. The management team was also able to pay down $35 million in debt during the quarter, bringing its total to $60 million since May of 2013. We believe that paying down this debt, given the advantageous prices in the market, is the best use of the Company’s capital, and shareholders will berewarded in the coming quarters.

Management experienced some stabilization in its drilling business, and the services division saw margins expand during the quarter. The Company was able to renew its drilling operations inColumbia, under slightly better terms, which should help the bottom line the rest of 2014. Also, the Drilling Services Segment margins expanded by 6 percent from last quarter and appear to be sustainable at these levels. While the Company will upgrade some of its fleet, the bulk of its cash flow will continue to go toward paying down debt.

This was the best quarter the Company has reported in a while, and the management team was more optimistic about business conditions on its conference call with investors. Pioneer has an extremely conservative valuation, and as management improves its balance sheet it will be able to generate significantly higher profits for its shareholders. We are encouraged by these improved operations and still believe the shares will reach $13 by the end of 2014.

© McIntyre, Freedman & Flynn