This year in the stock market I feel that most investors (and commentators) are focusing on walking the daily, hourly and, perhaps, even second to second ups and downs of the major market indexes. They’re measuring their progress each day, like using the foot-long ruler to measure a coastline.

When the market is down more than 2% like last Monday, it is all gloom and doom. When the market soars better than 1% on two days, back to back, like last Thursday and Friday, it’s “Happy days are here again”!

As with most things in life, with the stock market it is often better to get a broader perspective – see the forest not just the trees. When you do that, it’s apparent that last week was a probable turning point, or at least a notable one.

Check out this longer-term chart of the S&P 500. When I link the lows together (the red line), three things are noteworthy:

1.It looks just like a coastline, and the advancing sloping line better captures the trend than does the daily ups and downs,

2.Even after last Monday’s plunge, the long-term upward trend of the great 2013 stock market rally is still intact; and

3.Last Monday’s touch of the trend line said that emotionally bearish investors were likely spent and a turnaround to the upside was possible as long as that low held.

While the weakness may not be over yet (the average downturn once the market has fallen 5% has been a little over 8% since the current bull market started in 2009), the turnaround last week may mark the bottom and, in any event, we are not expecting anything more than a correction, worst case.

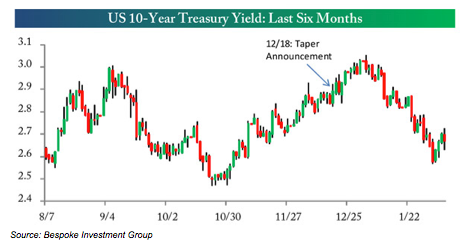

Earnings continue to be more positive than expected, and as the chart below shows, the Federal Reserve’s December tightening decision has surprisingly sent interest rate yields lower. This is positive for the intermediate term.

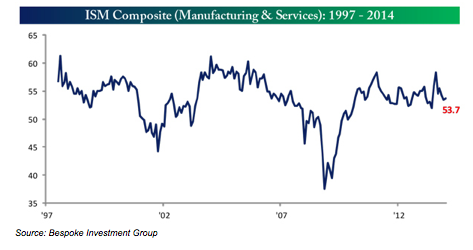

Most of the market moves last week were dictated by economic reports. The ISM Manufacturing Index was a major disappointment on Monday. Yet by Wednesday, when you combined it with a positive report for the companion Services Index, given the fact that the service sector of the economy is bigger than manufacturing, the result was actually an uptick in the total.

And while the employment numbers for a second month in a row were weaker than expected (the Fed seems to have chosen a high point in the economy to start tightening), this is precisely the type of news that suggests the Fed will go slowly in further tightening moves. While these reports were weak, overall, last week out of eighteen economic reports, underperforming reports were outnumbered by better-than-expected reports 10 to 6.

Furthermore, investors are no longer registering the overconfidence that a 30% 2013 rally instills. And while the market is short term overbought (which could cause some further weakness this week), the stock market’s intermediate term overbought readings have been negated.

All the best,

Jerry