Focus on Income: The Illiquidity Premium: Opportunities for Investing in Credit Today

At a time when many investors are seeking income for their portfolios, traditional sources of fixed income - principally government bonds and high-grade corporate bonds - look less than compelling. Yields are low and there is an increasing risk that interest rates will rise, which would cause the value of existing bonds to fall.

Illiquid credit offers potentially attractive returns to those investors willing to forgo immediate access to their money

The search for yield has led individual investors to consider non-traditional sources of income. Illiquid credit, once the province of pension funds, endowments, foundations and other institutions with the luxury of long term horizons, is one such alternative. F or those investors willing to forgo immediate access to their money, illiquid credit offers the potential for attractive expected returns without an apparent commensurate increase in risk.

Winston Churchill observed that where the pessimist sees difficulty in opportunity, the optimist sees opportunity in difficulty. To the optimist, the aftershocks of 2008 credit crisis that hobbled banks opened up new opportunities for individual investors to participate in illiquid credit investing. The classic categories of these complex and often esoteric loans include corporate debt, real estate, structured finance, direct lending and the purchase of portfolios and orphaned assets.

Banks have vacated the illiquid credit market, creating an unusual window of opportunity.

Historically, this subset of lending has been the province of banks. But banks’ participation in this important market has declined as a result of several factors. Regulatory pressures to recapitalize under Dodd-Frank in the US and Basel III globally, mark-to-market accounting, a reduction in buyers for portfolios and difficulty acquiring and retaining the credit and negotiating talent have all contributed to banks vacating the illiquid credit market.

Moreover, this retreat is occurring during what appears to be the middle stages of a good credit cycle, a time when default risk on loans related to business activity may stay low, relative to historical levels. We believe that once banks rebuild their capital base through earnings and equity raises, the profitability of illiquid credit will lure them back to their historic role. In the interim, however, we believe the banks’ retreat has created an unusual window of opportunity, not only for pension funds and endowments, but also for asset management firms which, in turn, can open the opportunity to individuals.

It’s unlikely this window of opportunity will stay open long

We expect pension funds to fill part of the gap created by the banks. Having benefited from the rising US equity market, pension funds will likely be re-allocating assets to fixed income. While this may sound counter-intuitive, given our view that interest rates are on a slow rise, these institutions are seemingly taking a very long term view of their liabilities and re-adjusting their asset mix to take advantage of, among other options, the illiquidity premium. Ultimately, as participation by pension funds and other institutional investors picks up, the pace of the yield curve steepening will likely slow down. In other words, their demand for illiquid credit will bid prices up and bring yields down. This, plus the eventual return by banks to illiquid credit lending, could result in this window not staying open for very long.

Investors have the chance to exploit an apparent anomaly

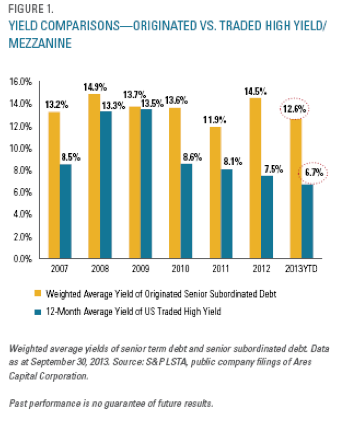

Interesting work done by Henry McVey, who heads global macro asset allocation at KKR, highlights some of the apparent anomalies that currently exist in the less liquid market. As Figure 1 below shows, yields on originated loans--that is, private loans not traded in the public market—are, as expected, higher than on publicly-traded high yield debt. This reflects investors’ demand for higher returns in exchange for less liquidity. What is important about Figure 1 is the increasingly large divergence between the two yields, a current trend that began in 2010 and continued through 2013.

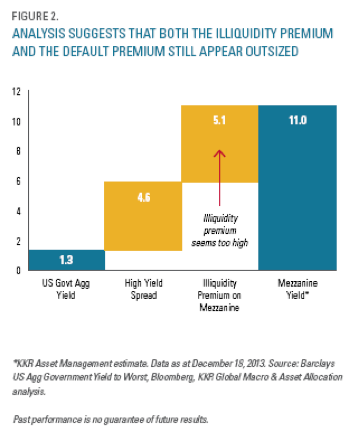

Figure 2 makes a similar point. Yields on highly liquid US Treasuries were 1.3% in December 2013 while yields on illiquid mezzanine loans, a key source of capital to small and medium-size businesses, reached 11%. Of that yield, 5.1% represents the illiquidity and default risk premium required by investors, a premium that KKR thinks may be too high. As we know, anomalies have usually been followed by reversion to the mean.

A position in illiquid credit has a second, less obvious advantage.

In addition to the potential for higher returns, investing in illiquid credit can have a second, less obvious advantage of protecting investors in times of crisis. Perceived liquidity in the height of the financial crisis in 2008 and early 2009 was actually a detriment to performance. Investors sold, because they could. That selling, in turn, forced managers to liquidate portions of their portfolios to meet redemptions at fire sale prices just at a time when opportunities for those with the capacity and capability to make the most of the disruptions. In other words, liquidity is important, but false or imbalanced liquidity can reduce returns substantially.

Because this window of opportunity may not stay open forever, investors should take this opportunity to discuss the correct reallocation of assets with their advisors. For that portion of the portfolio that needs to remain liquid and immediately available, investors should consider some reallocation to mutual fund yield portfolios that have lower risk profiles and can take advantage of the anticipated increased volatility in the fixed income markets. This includes funds characterized as “non-conventional,” as well as long/short fixed income funds that are arbitraging credit risk as well as interest rate risk.

Investors comfortable with lower liquidity should consider funds whose managers have experience investing in illiquid credit

For that portion of the portfolio where yield is important but liquidity less so, we suggest that investors look for managers with experience managing long term capital who have demonstrated an ability over the past five years to provide a significant yield differential while controlling loan losses. Fortunately for the individual investor, not only has the number of managers with relevant experience increased, but so has the quality of the illiquid credit.

We encourage investors take a hard look at their fixed income portfolios to determine their exposure to an environment in which rates will likely rise and a good credit cycle will prevail, and adjust accordingly. In our view, this means moving some assets out of highly liquid, traditional fixed income investments into portfolios that are taking advantage of what the banks are not doing. In short, this could be the time to take advantage of elevated illiquidity premiums.

This material is being provided for informational purposes only. The author’s assessments do not constitute investment research and the views expressed are not intended to be and should not be relied upon as investment advice. This document and the statements contained herein do not constitute an invitation, recommendation solicitation or offer to subscribe for, sell or purchase any securities, investments, products or services. The opinions are based on market conditions as of the date of writing and are subject to change without notice. No obligation is undertaken to update any information, data or material contained herein. The reader should not assume that all securities or sectors identified and discussed were or will be profitable.

Past performance is not indicative of future results. There is no guarantee that any forecasts made will come to pass. Due to various risks and uncertainties, actual events, results or performance may differ materially from those reflected or contemplated in any forward-looking statements. There can be no assurance that any investment product or strategy will achieve its objectives, generate profits or avoid losses.

All investments carry a certain degree of risk including the possible loss of principal. Complex or alternative strategies may not be suitable for everyone and the value of any portfolio will fluctuate based on the value of the underlying securities. Investing in debt or fixed income securities involves market risk, credit risk, interest rate risk, derivatives risk, liquidity risk, and income risk. As interest rates rise, bond prices typically fall. Below investment grade, distressed, or high yield debt securities are considered speculative and are subject to heightened liquidity, default, and credit risks.

ABOUT ALTEGRIS

The Altegris group of affiliated companies is wholly-owned and controlled by (i) private equity funds managed by Aquiline Capital Partners LLC and its affiliates (“Aquiline”), and by Genstar Capital Management, LLC and its affiliates (“Genstar”), and (ii) certain senior management of Altegris and other affiliates. Established in 2005, Aquiline focuses its investments exclusively in the financial services industry. Established in 1988, Genstar focuses its investment efforts across a variety of industries and sectors, including financial services. The Altegris companiesinclude Altegris Investments, Altegris Advisors, Altegris Funds, and Altegris Clearing Solutions. As of December 31, 2013, Altegris had .49 billion in client assets, and provided clearing services to 3 million in institutional client assets.

© Altegris

© Altegris