Fears over emerging markets, a tightening Federal Reserve Board and a loss in momentum in the economy have combined to create a sloppy market for stocks, while the bond market continues to confound the pundits and enjoy a solid start to the New Year.

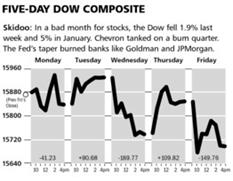

As the charts above illustrate, the Dow Jones Industrial Average fell over one percent last week while the NASDAQ Composite led by Apple and Amazon dropped by .6%

The Markets & Economy

The Happy Talk continues to emanate from the administration in Washington DC and its supporters in the media. To listen to last week’s State of the Union speech, one would think the US economy is doing very well. If so, then why the need for a sixth year extension of “emergency” unemployment benefits? Why then would Walmart warn on their holiday season and cite a lack of food stamp buyers as a reason? Something just doesn’t add up.

Friday’s report on GDP growth in the USA showed that in 2013 the economy grew by 1.9% which was down quite a bit from 2012. To be fair, the growth rate from the 4th quarter of the two years showed better results, but still nothing to indicate prosperity was around the corner.

To make matters worse, the misperception took hold that somehow 2014 was going to be significantly better - this despite turmoil around the globe and Obamacare at home causing employment to drop and consumer confidence to plummet.

The above explains why the bond market this morning is at its best levels since early November. This, of course, is exactly the opposite from what many had predicted would occur while the Fed engaged in its “tapering” policy adjustment. Thus the year has started off on a confusing note. Too much enthusiasm entered the stock market late last year, and the commentary about the economy is just laughable and now is changing.

This morning’s national ISM report on manufacturing may be the biggest skunk at the party so far. Plunging new orders took that index to an historic miss with implications for another weak employment report this Friday. It is becoming ever so clear to more and more people that the year 2014 will be just like the last several ones. This means growth will once again disappoint, but many of the “doctored” economic statistics will continue to show improvement which will allow the myth of improvement to continue to perpetuate itself despite the hard evidence to the contrary.

What to Expect This Week

Janet Yellen was sworn in this morning as the new Chairman of the Federal Reserve Board and she will soon learn that she is in a difficult position. The Fed wants to get out of the QE business because it doesn’t work and has long-term negative implications. On the other hand the financial markets are addicted to this money printing and the problems you are observing around the world are at least partially due to the fewer dollars being created along with the perception that fewer still will be created going forward.

Until someone blinks (it will be the Fed), the markets will be nervous and penalize weak earnings or even revenue growth a bit more aggressively. This morning’s weak January auto sales report is another worrying sign for 2014.

The next big data point for the New Year will be Friday’s unemployment report. This report could be a game changer, but then again due to all the assumptions and seasonal adjustments the government can virtually report any number it wants.

Finally, our look at the weekly leading economic indicators from the ECRI shows little change in outlook for the economy. I look for this index, which is influenced by stock prices, to further weaken in the weeks ahead. GDP growth for 2014 will be lucky to achieve 2%. This is good for stocks because it takes pressure off interest rates, but bad for any company which has weak fundamentals. Accordingly, we will continue to move our positions around to deal with this trend.

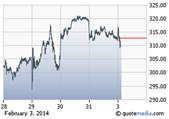

SYMBOL: BIIB

![]()

Biogen Idec reported better than expected fourth-quarter earnings results last week as sales of the multiple sclerosis drug Tecfidera continues to exceed all estimates. Profits rose by 57 percent to $2.34 per share, which was roughly a dime better than Wall Street’s consensus estimates. Also revenues grew by 39 percent to nearly $2 billion. Management is expecting 25 percent revenue growth in 2014, and was conservative with their earning guidance for this year.

Sales of Tecfidera continue to outpace all of its competitors and the Company received approval this morning to market the drug in Europe. The drug remains on pace to exceed $1 billion in revenue for its first year on the market, as sales grew to $398 million in the fourth quarter. Analysts believe the drug should reach annual sales of $6 billion by 2019, and we believe this is too conservative given the record launch of the drug.

Since building the industry leading treatment franchise for multiple sclerosis, management now is looking to grow its hemophilia division into an industry powerhouse. They have announced several development deals in the last several quarters and we expect to hear plenty more from the division during the second half of 2014. Also, look for a mid-year launch of Pledgridy, a treatment for recurring MS, as a positive catalyst for the share price this quarter.

Biogen has been one of the top performing stocks over the past two years, and we expect the news will only improve at the Company. We believe management is making all the right moves to build itself into a leading pharmaceutical company in the world. Shares of Biogen will likely remain volatile, but we view any significant pullback as a buying opportunity. We are raising our 12 months price target to

$400.

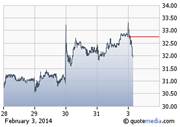

SYMBOL: BX

Blackstone Group reported record fourth-quarter earnings last week, as strong capital markets and the recovery of the real estate market fueled strong profit growth. Economic net income more than doubled to $1.35 per share, compared to consensus estimates of just $0.83 per share. CEO Steve Schwarzman has positioned the Company for aggressive growth and sees stronger economic activity in 2014.

The Company benefited from rising asset prices and stronger capital markets that have allowed the Company sell four of its holdings by initial public offerings this quarter. The Company took Hilton Worldwide, Extended Stay America, Brixmor Property Group and Merlin Entertainments public during the quarter. Due to the offerings, management was able to value those four assets 35 percent higher than in the third quarter of last year.

Blackstone saw its assets under management rise by 7.1 percent from the third quarter, and sees strength in the capital markets continuing through 2014 and beyond. Management was able to attract $17 billion in new money during the quarter as investors around the world are lining up to do business with Blackstone. The Board also declared a quarterly distribution of $0.58 per common unit this quarter and the units still offer an extremely attractive yield.

Blackstone has been one the best performing financial stocks of 2013 and we look for the positive momentum to continue. The management team at Blackstone took advantage of the financial crisis to build a much stronger Company and investors are benefitting from the improvement in capital markets. We continue to hold on to Blackstone and expect the units to reach $40 within the next 12 months.

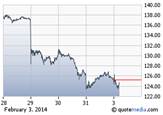

SYMBOL: BA

![]()

Boeing reported better than expected fourth-quarter earnings last week, although the shares sold off following conservative guidance from management. The Company earned $1.61 per share, as revenues rose by 7 percent to $23.79 billion. Both of these numbers easily exceeded consensus estimates, but management brought down this year’s earnings per share guidance to the low-end of estimates.

Boeing’s management has a history of doing this every year, and we expect 2014 will be another record year for Boeing.

In 2013 Boeing shattered records for revenues, profits and the number of commercial aircrafts delivered during one year, and we look for management to grow on this success. The Company ended this year with a record backlog of $374 billion, which will turn into profits over the next several years.

Production has been ramped up on the 737, 777 and 787 aircrafts in the second half of 2013, and we expect record shipments this year. Boeing is the bright spot in manufacturing in our domestic economy, and management is using this to grow its dominant position in the global marketplace.

Shares of Boeing traded lower following this report, but we believe any weakness is a buying opportunity. As management converts its record order backlog into free cash flow, we expect the shares will continue to head higher. The shares have a conservative valuation at these levels, and we expect further production increases will act as a positive catalyst to the shares over the next several months.

We maintain our 12 months price target of $165 per share.