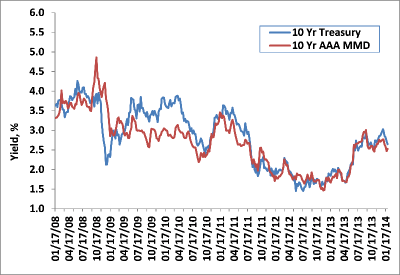

Taking direction from a sharp sell-off in risk assets across the globe—especially in emerging market economies, Treasury yields continued their month long decline last week. Falling nearly forty-basis points since December, 10 year Treasury rates (2.65%) have decreased the most in any month since August 2009 and are off to their best yearly start in six years. Though interest rates unfortunately appear to be a function of price action in other asset classes, there is potential for further volatility this week, as important economic data (ISM; payrolls report) are added to the mix.

The first week of February also officially marks the beginning of Janet Yellen’s tenure as head of the Federal Reserve. The new Chairwoman will have little time to acclimate herself to the new role, as she will deliver her mandatory Humphry Hawkins testimony to Congress next week (February 11th)—an event that will surely warrant market scrutiny. As expected, the Federal Open Market Committee reduced their monthly bond purchases by an additional $10 billion last week, to $65 billion ($35 billion Treasuries, $30 billion mortgage backed securities). Barring a dramatic negative shift in economic activity, Castleton expects the FOMC to taper by $10 billion per meeting, ending their monthly purchases entirely by December.

Weekly Change: 10Y Treasury Yields vs. 10Y AAA MMD

Source: Bloomberg, Thomson Reuters and Castleton Partners

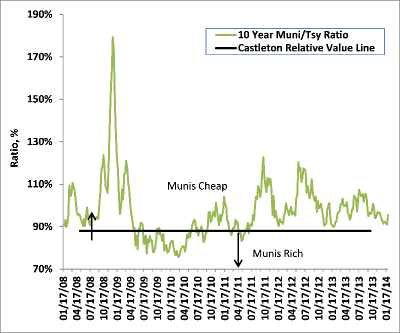

Ratio of 10Y Muni Yield to 10Y Treasury Yield

Source: Bloomberg, Thomson Reuters and Castleton Partners

Tax-Exempt

The tax exempt market took a breather last week, following a sustained rally over the first three weeks of 2014. Yields across the maturity spectrum were 5-8 basis points higher, as municipals markedly underperformed Treasuries. With 10 year municipal yields currently at 2.53%, the Muni/ Treasury ratio rose to 96% from the prior week’s 91% level.

Despite last week’s underperformance, tax exempts registered an impressive January, producing the best absolute and relative returns across fixed income for the month, in sharp contrast to 2013. Strong price gains were registered across the maturity spectrum in January, as 5y, 10y, and 30y yields fell by 14bp, 39bp, and 34bp, respectively. An improving technical backdrop—along with superior tax equivalent yields—is behind municipals’ impressive monthly performance. Mutual funds, which account for nearly 30% of asset class demand, remained positive for the third consecutive week, rising to $334 million—the highest tally in nearly a year. Tax exempt supply remained relatively light last month at just over $12 billion, an 18% drop versus January 2013.

Supply is expected to be below trend this week, with less than $4 billion coming to market. The State of Illinois (A3/A1/A-) accounts for 25% of the total, with a new money $1 billion general obligation loan earmarked for school and construction projects. Illinois has outperformed other tax exempt credits of late, owing to recently passed pension reform legislation. Though Illinois continues to struggle with economic growth, Castleton remains constructive on Illinois for long term investors due to the high degree of bondholder security that is perhaps the best among all fifty states. Under state law, the governor has NO discretion for NOT paying debt service. The state provides for debt service by segregating sufficient cash at the end of each month to cover 1/6th of all coming semi-annual interest payments and 1/12th of all principal payments. These monies are deposited in a trust, which CANNOT be tapped for any other purpose.

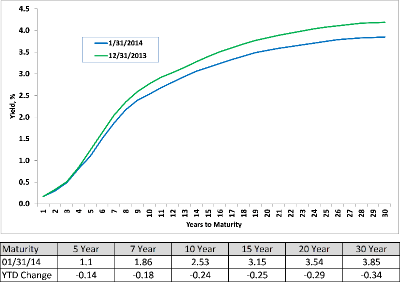

AAA Municipal Market Data (MMD) Yield Curve

Source: Thomson Reuters

Weekly Municipal Mutual Fund Flow Data

Source: Lipper AMG Data

Taxable

Though prices rallied with the sharp fall in Treasury rates last week, investment grade corporates were not immune to the risk off-trade, as spreads widened, on average, 8bp across all sectors. With the sharp rise in volatility last week, coupled with stocks registering their worst monthly decline since May 2012, only $13b of corporate debt was priced—the lowest week of 2014. Despite anemic yields, preference among taxable investors remains relatively short, as nearly 70% of last week’s volume was in 3 and 5 year maturities. Credit default swaps—as measured by the Markit CDX North American Investment Grade 5y Index—surged 10 points in January to nearly +73, highlighting the recent underperformance relative to Treasuries. The Markit CDX Investment Grade Index is comprised of 125 equally-weighted credit default swaps on investment grade companies and is intensely watched and/or traded by institutional taxable investors to hedge or speculate on the creditworthiness of corporate bonds.

Markit CDX Investment Grade Index

Source: Bloomberg

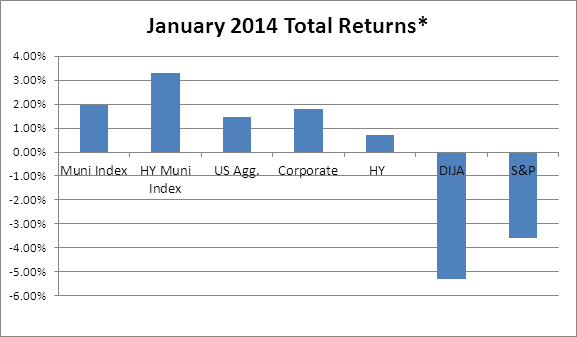

* Based on the Barclays family of indices

Muni Index: +1.95%

HY muni index: +3.29%

US Agg: +1.48%

Corp: +1.81%

HY: +0.70%

DJIA: -5.30%

S&P: -3.57%

© Castleton Partners