With temperatures hovering around zero and wind chills in the negative teens, I can’t think of any better label for Friday’s stock market sell off than a “polar bear”. Here in Michigan at the Detroit Zoo, one of the nation’s finest, we have a rather unique polar bear exhibit. Visitors to the zoo can actually walk through tunnels interspersed throughout the polar bear environment created in the exhibit. At one point you are underneath the big furry creatures as they swim about. It is a beautiful sight.

Friday’s stock market, on the other hand, was anything but beautiful. Supposedly in response to weak manufacturing numbers from China, stocks sold off throughout the day. The opening price was the high for the day and the closing price was the low. You don’t get any more “down” than that. (And this hasn’t happened since November, 2011, and only 17 times in the last ten years, so it is relatively rare, but as Bespoke Investment Group points out, it has led to positive results one day and a week out more than half the time.)

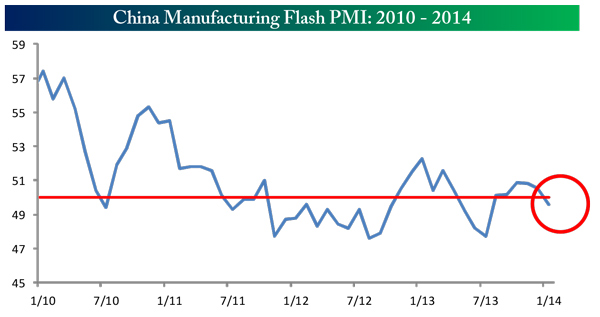

While the blame was on a below 50 Chinese PMI report, a quick look at the chart of the Chinese numbers in the past show that this has happened many times before and a 300-plus decline in the Dow was not always the result, as it was on Friday.

Source: Bespoke Investment Group

Instead, I believe, as I have stated since the end of last year, 2014 is going to be a more volatile year. In 2013, we did not have any decline worse than 5%. But as I said two weeks ago, I believe that we will see 10%+ corrections this year. After all, we have now gone over two years since the last 10% correction (mid-2011 had a 19.6% decline), so we are due. This is the fifth longest period in the last 86 years without such a correction.

The average 10%+ correction ends up being just over 14% in depth, and 16% when it follows a wide gap between such corrections. With last week’s 2.6%-plus decline, the fall from the S&P 500’s recent top was just 3.1%, down from its all-time high set on 1/15/2014, only six trading days ago.

There’s no way to know if this decline is going to be a 10%-plus correction. While I believe we will see at least one this year, if this is the beginning I don’t think we are going to see a down escalator to lower levels. Instead, I wouldn’t be surprised to see some strengthening in the near term.

The reasons why I gave for some beginning of the year downside action were: seasonality, earnings season, an overbought market, and the tapering of Federal Reserve bond purchases. A quick look at our Political/Seasonality Index will show a bottom occurring Friday. Earnings are coming in stronger so far than they did during the last eleven earnings reporting seasons. And, Friday’s tumble was fast and severe enough to move most of the stock market indexes out of overbought territory and into short-term oversold readings.

Finally, while the Fed is still set to taper, the reduction (from $85 billion to $75 billion) is relatively mild. More importantly, the markets have responded well to the move. Interest rates, rather than soaring as some commentators suggested they would, have fallen quite nicely. And the dollar has rallied, indicating that the world of global commerce likes the Fed’s move.

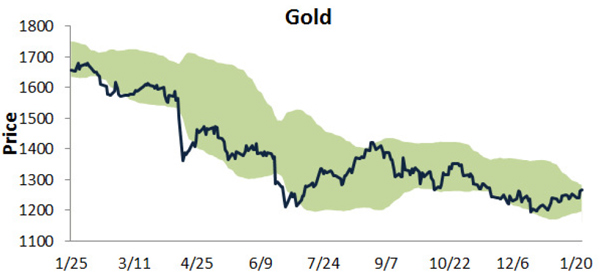

It certainly looks like the stock market could bounce higher from here before resuming its quest for a 10%-plus correction. In the meantime, the positive action has been in bonds, the dollar and… gold. Since we mentioned the possibility that gold might be hitting a bottom in December, the yellow metal has gained 6.5% since its December 19th low. It even gained ground last week, cushioning the decline in stocks.

Source: Bespoke Investment Group

If you clicked on the video above, you know watching the polar bear can be fun. But why is the bear having even more fun than we are? Funny, that’s how I felt Friday, too.

All the best,

Jerry

© Flexible Plan Investments