My caution last week unfolded into a market sell off related to both disappointing earnings and concern over emerging markets affecting the foreign exchange markets.

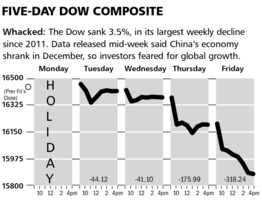

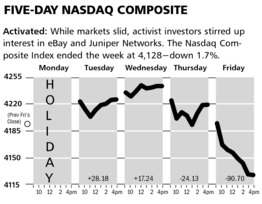

As the charts above illustrate, the Dow Jones Industrial Average tanked by 3.5% last week, while the NASDAQ Composite dropped by 1.7%.

So far in 2014 the averages are now negative; but not by all that much despite last week.

The Markets & Economy

While the beautiful people convened in Switzerland last week, the concerns mounted in the real world as to the strength of the global economy and whether or not the Fed’s recent policy move to begin tapering has indeed begun to impact capital flows in the emerging markets. Countries from Turkey, Argentina, South Africa and of course, the usual suspects of Venezuela and the Ukraine all had difficulties. This caused a surge in the major currencies such as the Dollar, Yen andEuro, and a rally in major bond markets.

When all was said and done, the hedge funds were poorly positioned for this sort of inter-market move, and they were forced to quickly adjust their positions. That is what led to the downdraft late in the week. The decline was then greatly influenced by hot money, but the fundamental questions behind the move have now moved to the front burner. No longer is there so much happy talk about the recovery here in the United States. This morning’s report on new home sales for December was a disappointment and does anyone think January will be better?

Clearly, the year 2013 didn’t end well for global growth. It may be weather related, but the weather remains an issue in January. This has helped us as our portfolios are richly endowed with natural gas and oil plays which are doing exceedingly well. The other theme which continues to persist, but gets little attention in the media, is this assumption that 2014 will be a better growth year than last. Beyond the fact that we have heard this from the same people (Central Banks for one) every year since 2010, what gives this any credence?

The revenue lines on many firms remain disappointing even as earnings are fine. This is being accomplished through expense control which you should read to mean lack of hiring. Given the tax hikes involved with Obamacare, this trend looks to continue throughout 2014. I think when all is said and done, the year will be lucky to record anything above a 2% growth rate. This will play out at a time when the Federal Reserve is most likely to continue its tapering policy. While the impact on the domestic economy is likely to be small, if it in anyway contributes to problems in global markets, then our exports will be impacted which would be a negative for growth.

What to Expect This Week

Sadly, the markets this week will be fixated on two things, which should be ignored.

- The first is the annual State of the Union Speech. President Obama is likely to focus on income inequality (read that to mean he wants more redistribution/tax policies,) and other such policies as global warming regulations despite January being the coldest month in over one CENTURY. While none of his agenda has any chance whatsoever in Congress, he continues to hold forth the notion that he will act unilaterally where possible. Not good.

- Secondly, this week there is a two day Federal Reserve Board meeting which will usher in the new Chairman, Janet Yellen. While she is about as much a dove as has ever had the position, she will most likely not want to rattle the cages too much with any break from previous Fed statements. This may or may not please markets, so unfortunately we will have to watch it.

- Finally, there will be much economic news released this week. This includes the GDP report for the final quarter of last year which is expected to show an annualized growth rate of 3%. Judging by the top line numbers being released by companies, that seems to be aggressive, but we shall see.

The weekly reading from the Economic Cycle Research Institute (next page) showed a pull back this week. Thus any thought this index was going to confirm a stronger economy can once again be put back in the closet. This will be a tougher year for all asset classes, but stocks remain the best alternative. Bonds, emerging markets, commodities all have much higher risk profiles in my opinion.

SYMBOL: MSFT

Microsoft reported better than expected fiscal second-quarter earnings last week, as the Company continues to have success in its Consumer Products Division. Revenues grew by 14 percent from last year to $24.5 billion, which was a billion dollars higher thanWall Street’s consensus estimates. Earnings per share came in at $0.78 per share, which also topped estimates by a dime per share. We are excited about the top line growth at Microsoft, and believe a new CEO could act as another positive catalyst for shareholders.

While other large technology companies are struggling to grow the top-line, Microsoft had several successful new product launches. The Surface 2 tablets are selling much better than expected, as revenues more than doubled from last year. Also the Company sold 7.4 million Xbox consoles during the quarter, and Xbox One was the top gaming console during the holiday season. Bing also continues to take market share in the search market, and ad revenues increased 34% during the quarter.

With operations improving, we believe that the new CEO will be taking over a much more exciting company than it was a year ago. There has been much speculation over who is going to be taking over the top job at Microsoft, and we expect an announcement from the Company is imminent. We believe this announcement should take the price higher, and look forward to hearing a new strategic direction for the Company.

Shares of Microsoft rallied following the release of this earnings report, even though the market sold off sharply at the end of last week. The stock has a conservative valuation, and we believe investors will begin to focus on the newer growth initiatives at the Company, not just its PC Division. We expect the shares of Microsoft to reach $45 by the end of 2014.

![]()

SYMBOL: FCX

Freeport-McMoRan Copperand Gold reported mixed fourth-quarter earnings results last week, but we believe the fundamentals are improving at the Company. The Company earned $0.84 per share, after one time charges, which was 4 cents higher than expectations. Revenues did come in light of consensus estimates at $5.89 billion, which was 30 percent higher than last year. The Company continues to have problems with its operations in Indonesia, which are weighing on the shares, but as these issues are resolved shareholders will benefit.

We believe that this earnings report indicates a much brighter future for shareholders of Freeport, and any weakness represents an excellent buying opportunity. The Company was able to increase copper production by 17% during the quarter. Also they significantly brought down the cost of copper production per pound. The average cost per pound came in at $1.16, which beat estimates of $1.46, and last year’s number of $1.54. This improvement will lead to higher margins in the future, and we believe earnings estimates are too low for the Company.

Freeport’s management team is focused on bringing down costs, and will be selling some assets this year to lower the debt load. This coupled with strong cash flow generation will give the Company a much stronger financial position by the end of this year. We do not believe this is priced into the current share price and expect investors will take notice.

Shares of Freeport sold off with the market last week, but we look for the shares to bounce back with better market conditions. We believe the deleveraging process at Freeport will be the prevailing story for shareholders this year. We expect the shares will reach $45 by the end of this year, and have been buying more shares on this downturn.

![]()

SYMBOL: CAT

Shares of Caterpillar are sharply higher this morning following better than expected fourth-quarter earnings results. Earnings per share came in at $1.54, which was $0.26 better than Wall Street’s consensus estimates. Revenues did fall by 10 percent from last year to $14.4 billion, but this was better than Wall Street’s dire estimates. The management team also announced a new $10 billion share repurchase plan, and will look to buy $1.7 billion in the first quarter of this year.

The management team at Caterpillar has done a nice job of cutting costs, while the domestic construction industry has been stronger than many were expecting. US construction spending in November was the highest since March 2009, and this strength has come at the right time for Caterpillar shareholders. We look for these trends to continue in the short-term, and expect that China and mining businesses are likely nearing a bottom

.

We are encouraged by the better-than-expected results, and the new share repurchase plan should continue to move the share price higher. We held onto Caterpillar when many on Wall Street were dumping, and now our patience is starting to pay off. We are closely monitoring the end markets that Caterpillar operates in, and look for further signs of recovery. We believe that the shares price is headed higher in the near-term, but it will take a stronger recovery for us to remain long-term shareholders.

© McIntyre, Freedman & Flynn