Given stocks’ stellar rise over the last year, investorsworried about a correctionare asking me where they can park their money.

While I still believe that stocks aren’t yet in bubble territory andcan still push ahead this year, there’salways the risk that an unknown exogenous shockcould send markets tumbling.

So to help investors who are concerned about such a scenario and want to allocate tosafe havensto prepare, here’s a look at how various traditional safe-haven investments stack up in terms of post-market shock performance.

Contrary to popular belief, gold may not be the best performing safe - haven option, at least based on an analysis by David Wang, a researcher on my Investment Strategy Group team.

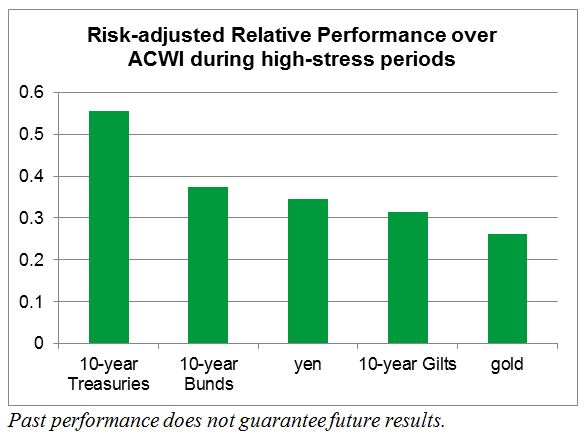

David looked at how a number of safe havens performed in comparison to the broad equity market during periods of high financial - markets stress over the last two decades.

He identified the periods of uncertainty, including the 2008 financial crisis and the collapse of Long - Term Capital Management in 1998, using theCleveland Financial Stress Index. He also compared the assets’ monthly averagerisk - adjusted returnsin order to gauge which safe havens delivered more stable outperformance.

Based on David’s analysis, though all of the safe havens examined outperformed the broad equity market during the high stress periods, they didn’t outperform equally. The 10 - year U.S. Treasury was the best performing safe haven on a risk - adjusted basis, followed by 10 - year German Bunds, 10 - year U.K. Gilts, yen and gold, as the chart below shows.

In regards to gold in particular, although the precious metal ranked highest in terms of average outperformance when risk didn’t come into the equation, it actually was the least attractive safe haven on a risk - adjusted basis. This is thanks to its status as the most risky safe haven examined (as measured by returnvolatility).

In addition, David found that U.S. Treasuries tended to outperform even when the source of uncertainty happened to be the U.S. government. In other words, investors who areworried about U.S. fiscal policy or a government shutdownmight still want to opt for U.S. Treasuries as a safe haven. This may have to do with investors’ perception that the U.S. Treasury is the closest thing we’ve got toa risk-free asset, and their faith that the U.S. government will always solve its problems, even if the solutions come at the last minute.

To be sure, David’s analysis didn’t include an exhaustive list of safe - haven assets. Still, it’s a helpful start for setting a safe - haven allocation. In addition, safe haven assets aren’t risk-free investments. Still, it’s worth noting that even the least attractive safe haven (i.e. gold) in the analysis still outperformed the equity market during the stressful periods examined in the analysis.

Finally, these safe havens are probably not the best options for investors who, like me,don’t see a correction looming on the horizon. During periods of normal market performance when uncertainty isn’t high, safe havens tend to underperform the equity market.

Source: BlackRock Investment Strategy Group Research, Bloomberg

© iShares Blog