Pick up nearly any financial publication these days and it is bound to have one, if not several, stories about the headwinds facing the banking industry. Low interest rates are pressuring net interest margins; the financial crisis created a tidal wave of new regulations and operational costs; listless economic progress and political discord have left businesses lacking the confidence to invest, leading to tepid loan demand; and technological advancement is threatening to erode the value of branch networks built over the last 50 years. Despite these industry pressures, we believe banks with differentiated business models and niche customer bases can continue to thrive.

San Francisco-based First Republic Bank (FRC) continues to grow its business and intrinsic value even while dealing with a challenging industry environment. Growth in tangible book value per share is a common metric to evidence the growth in franchise value, and First Republic has grown its tangible book value at approximately a 15% compound annual growth rate (CAGR) since management bought the bank back from Bank of America in 2010.

A Differentiated Bank Model

Within select geographies, First Republic targets a niche demographic with its high-touch service model. The bank’s client base can simply be described as urban, coastal, and wealthy. These “economic outperformers” in markets such as San Francisco, New York, and Boston, tend to compound their net worth at rates faster than the economy as a whole. Couple the economic performance of their client base with “white glove” service, and it leads to lower client turnover and a high referral rate, creating an inherent growth rate in the business that is faster than peers.

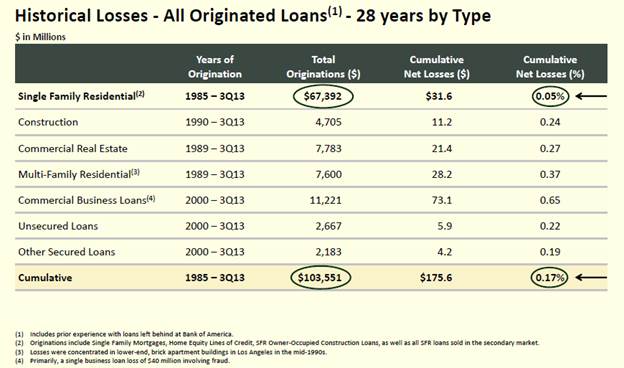

As a banker, it is nice to lend to people who do not need the money and whose capacity to pay you back is a multiple of what you are owed. The company regularly publishes a profile of its home loan clients, and the median borrower has a net worth of $2.6 million, a 775 FICO score, and liquidity of $571,000 to support the median loan size of $670,000. The bank also conservatively underwrites these loans with full documentation and a median loan-to-value (LTV) of 60%. The table below details First Republic’s impeccable underwriting history since 1985; lending conservatively to the right borrowers leads to great results. It is worth noting that this record was established during a time period that included two real estate collapses in their core market of California.

Source: First Republic Form 8-K (December 5, 2013)

After developing deep relationships with their retail clients, First Republic followed them to their places of business and philanthropic pursuits and created a strong business banking platform with a focus on schools, non-profits, and investment funds. This enhanced the value of First Republic’s franchise because the business deposits are a low-cost source of funding for the bank, now comprising nearly 50% of their deposit base. The business bank provides $4.60 in deposits for every $1.00 of loans with the excess deposits used to fund the retail side of the business.

First Republic has also leveraged their client base to develop a strong wealth management platform whose growth has accelerated since 2010. This not only diversifies its sources of revenue but also provides a valuable source of fee-based revenue and further entrenches the bank with their clients. As clients age, retire, sell businesses, pursue philanthropy, etc.; the wealth management platform is there to assist clients, and this business provides higher returns and is less capital intensive than core banking.

Growth vs. Value

With above-peer growth rates, First Republic is often labeled a “growth bank” and is on the higher end of the valuation spectrum in terms of price/earnings or price/tangible book value multiples. However, with our intrinsic value investing philosophy rooted in the evaluation of company fundamentals, we ignore such labels and agree with Warren Buffett, who in his 2000 annual letter described growth as “simply a component in the value equation.”

Sources of Investment Return

Despite the valuation multiples mentioned above, First Republic’s shares trade at a discount to our estimate of intrinsic value. Many investors only consider the convergence of the stock price and one’s estimate of value as the source of investment return. While we require a margin of safety to our estimate of intrinsic value in every investment, often times a more meaningful driver of investment return is the growth in intrinsic value over time. As investors, we are constantly searching for companies whose differentiated business can compound intrinsic value over time at attractive rates.

The banking industry as a whole certainly is facing multiple headwinds not limited to historic regulatory change and a sluggish economy. We believe First Republic’s differentiated client positioning allows them to grow the business despite these challenges and to compound its intrinsic value for the benefit of shareholders.

The views expressed are those of the analyst as of January 2014, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice.

© Diamond Hill Investments

© Diamond Hill Capital Management