Economic Growth is Likely to Improve in 2014

We believe a global economic upturn is likely in 2014, although the overall growth rate will remain sluggish. We think developed countries will show the largest improvement, which in turn will help support growth rates in emerging markets.

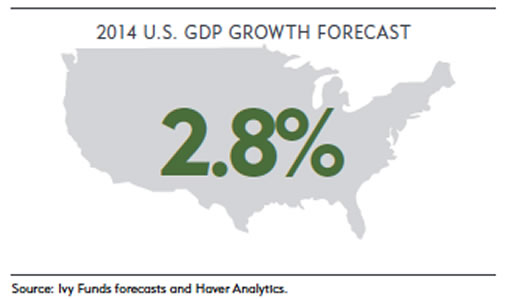

U.S. shows potential for faster growth

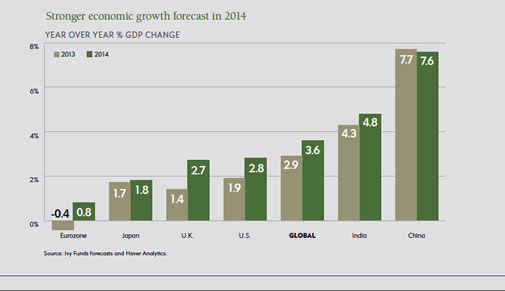

An increase in fiscal drag, higher levels of corporate uncertainty and continued weakness in the rest of the global economy contributed to a slowdown in the U.S. gross domestic product (GDP) growth rate in 2013 to roughly 1.9%. That compared with growth in 2012 of 2.8%.

View Larger Image

We believe U.S. GDP is set to grow in 2014 by 2.8% for several reasons:

- Fiscal drag is likely to diminish because the increase in payroll tax rates in 2013 will not be repeated in 2014 and there will be slightly less austerity in government spending. The fiscal drag in 2013 was 1.5 to 2.0% of GDP, but we think it will be minimal in 2014. In addition, we think the recent federal budget deal between Rep. Paul Ryan and Sen. Patty Murray, who chair the budget committees in the U.S. House of Representatives and U.S. Senate, will reduce uncertainty coming from the fiscal policy side.

- The reduction in fiscal drag coupled with modest improvements in employment and wages are likely to allow for an increase in consumer spending. In addition, we believe the recovery in household wealth on the back of recent stock market gains and higher home prices will provide additional support. Finally, the U.S. energy boom recently has helped hold gasoline prices at stable to lower levels.

- We believe that capital spending will accelerate. Capital spending has been disappointing over the past year, underperforming what other indicators would suggest. We believe stronger capital spending will be driven by pent-up demand as a result of more clarity in public policy, better external growth and improved credit availability.

The Federal Reserve (Fed) announced late in 2013 that it will begin tapering its purchases of securities in January 2014. However, we believe the Fed will maintain its view that tapering is not tightening in an attempt to dissuade markets from expecting an interest rate hike in the short term. If the economy progresses as we anticipate, then we think the Fed will wind down its asset purchases before year-end.

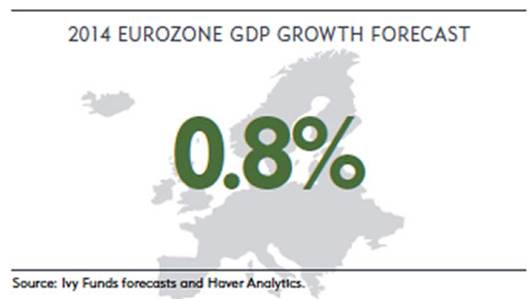

Europe leaves recession behind

Recession in the eurozone – which reported declining GDP for six consecutive quarters – came to an end in the second quarter of 2013. We believe growth will continue to be positive, although sluggish, in 2014. GDP growth in Germany is likely to continue to outperform the rest of Europe as better global trade and tighter labor markets lend support to corporate and consumer spending. The countries often referred to as “peripheral Europe,” including Spain and Italy, are likely to show slightly positive GDP growth for the year, in contrast to the large declines in GDP over the past couple of years. We think GDP growth in France should look more like peripheral Europe than Germany because necessary adjustments in competitiveness continue to lag other areas. Overall, we think eurozone GDP growth will average 0.8% in 2014.

View Larger Image

In the U.K., GDP growth has been better than many expected. Easier credit conditions and strong foreign demand have lead to a pickup in the housing market. This improvement coupled with lower interest rates, lower inflation and stronger employment are likely to lead to an increase in consumer spending. In addition, we think better growth from the U.K.’s two largest trading partners – the eurozone and the U.S. – should help exports.

The European Central Bank recently cut interest rates because as inflation was lower than expected. We think easy monetary policy will continue and further easing is likely if GDP growth or inflation are weaker than expected. The Bank of England has stated that it wants to keep rates low until the unemployment rate reaches 7%, which it forecasts to occur in third-quarter 2015. We believe the unemployment rate will reach 7% in the middle of 2014, which could cause some market concern because of fears of an earlier tightening of policy.

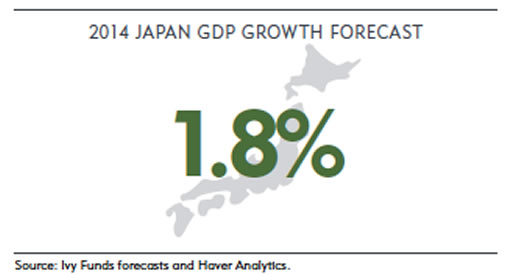

Japan grows at uneven pace

GDP growth in Japan was better than expected in 2013, rising roughly 1.7% with support from Prime Minister Shinzo Abe’s plan to end deflation and boost economic growth. We think growth will be inconsistent in 2014. We believe it will remain strong in the first quarter but drop temporarily in the second quarter because of a planned increase in the value-added tax (VAT) rate from 5% to 8%. We believe modest growth will return for the remainder of the year. Overall, we expect 2014 GDP growth in Japan to average 1.8%.

View Larger Image

We also think the slowdown in growth following the VAT increase coupled with a continued slow recovery in inflation will result in further easing by the Bank of Japan. The pace of Abe’s reform agenda has slowed recently and could generate market concerns if it this slow pace continues.

Emerging markets look to developed world

GDP growth slowed in emerging-market countries in 2013 as slower GDP growth in developed markets meant weaker export growth for the emerging markets. Weaker domestic demand in the emerging markets affected GDP growth as well. We believe emerging-market economic growth will be mixed in 2014. We think countries including South Korea, Taiwan and Singapore will benefit from better growth in developed markets. However, we believe emerging-market economies with large current account deficits are likely to underperform. These countries in recent years have been dependent on cheap funding and strong credit growth, which have boosted domestic demand. That situation has started to change now that U.S. interest rates have begun to rise. Overall, we think these countries are likely to have weaker credit growth and therefore less improvement in GDP growth relative to other emerging economies.

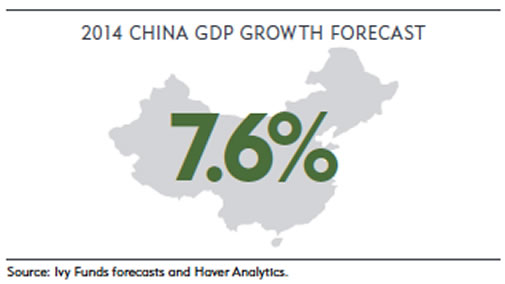

China faces challenge of past rapid growth

GDP growth in China looks to have averaged about 7.7% in 2013. We think growth in 2014 will be similar. We believe export growth will improve as developed market GDP growth picks up. At the same time, we think that growth in investment spending will continue to slow as China’s new leadership attempts to move toward a more consumption-oriented economy. President Xi Jinping has introduced a broad, long-term plan for economic and domestic reforms that we think will be positive for future growth in China. However, some of the reforms could be a headwind for short-term growth.

View Larger Image

Positive global outlook, but risks remain

While we have a positive view about the path for growth in 2014, risks remain. In the U.S., one of the biggest risks in our view is the Affordable Care Act (ACA) and its effect on businesses and consumers. Will businesses reduce the pace of hiring as a result of costs related to the ACA? Will higher healthcare premiums and deductibles cause consumers to cut back spending? We think the answer to both questions is likely to be “yes,” but the magnitude of the potential negative effect of the ACA still is unknown. We also think the market uncertainty caused by Congressional wrangling is likely to subside, although this is not assured since events in Washington still are difficult to predict.

The potential for some emerging-market economies to feel pressure from higher U.S. interest rates and less global liquidity remains a key concern. In addition, interbank rates in China have been trending higher, with periods of sharp spikes as the central bank tries to limit credit growth without creating a dislocation in the system. Finally, continued unrest in the Middle East could bring about a jump in oil prices. Overall, we are hopeful that policymakers will not endanger GDP growth in 2014.

View Larger Image

Past performance is not a guarantee of future results. The opinions expressed in this article are those of Mr. Hamilton and are not meant to predict or project the future performance of any investment product. The opinions are current through Jan. 6, 2014. Mr. Hamilton’s views are subject to change at any time based on market and other current conditions, and no forecasts can be guaranteed.

Investment return and principal value will fluctuate, and it’s possible to lose money by investing. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets.

Investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. For a prospectus, or if available a summary prospectus, containing this and other information for the Ivy Funds, call your financial advisor or visit us online at www.ivyfunds.com. Please read the prospectus or summary prospectus carefully before investing.

© Ivy Funds Investment Management