U.S. politics, policy still overhang markets

Although the December 2013 U.S. budget pact between House and Senate negotiators was a welcome development, partisan battles over government spending still are possible in 2014. The agreement ends a three-year budget fight and sets government spending through fall 2015, but it does not eliminate the need to raise the nation’s borrowing limit – the “debt ceiling.”

A leadership change at the nation’s central bank in 2014 represents another significant development in Washington as Janet Yellen begins her tenure as Federal Reserve (Fed) chair. Yellen takes the helm at what many consider one of the more difficult junctures in Fed history.

The Fed closed 2013 by taking the first step toward reversing some of the unprecedented monetary support it has provided since the financial crisis. The decision to reduce its quantitative easing (QE) bond-buying program by $10 billion, to $75 billion per month, came five years after the Fed dropped the benchmark fed funds rate to a range of 0 to 0.25% – a move that was followed by a series of other initiatives that the Fed launched to boost the economy. In his final press conference as Fed Chairman, Ben Bernanke indicated that the Fed would likely further reduce the bond-buying program if the economy continues to unfold as Fed officials expect. However, he also extended the Fed’s commitment to low interest rates, saying the fed funds rate could remain at its current level “well past the time” the unemployment rate falls below the Fed’s previous target of 6.5%.

According to Fed economic forecasts released after the December meeting, officials do not expect the fed funds rate to increase until 2015 and then only slightly. The Fed forecasts 2014 gross domestic product (GDP) growth in a range of 2.8 to 3.2% with unemployment at 6.3 to 6.6% by year-end. The Fed expects 2014 core personal consumption expenditures inflation at 1.4 to 1.6%.

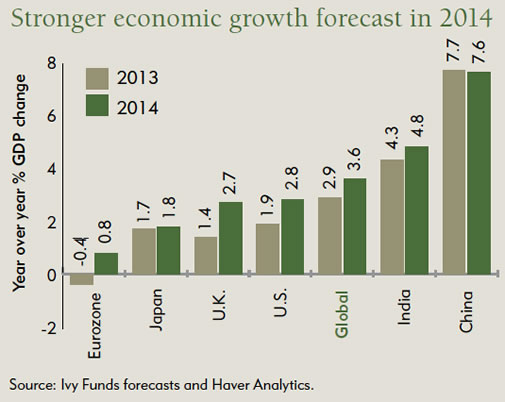

Global economy in 2014: Ivy Funds view on key markets

A synchronized global economic upturn is likely in 2014, according to Ivy Funds Global Economist Derek Hamilton, although the overall growth rate will remain sluggish. GDP growth is likely to show the largest improvement in developed markets and be mixed in emerging markets, Hamilton says. Acceleration in developed markets typically results in stronger growth in emerging markets, which he expects again in 2014. But Hamilton also thinks there are emerging-market countries that will continue to lag because of a need to slow domestic demand and credit growth.

View full global economic viewpoint here.

Stocks may benefit from U.S. economic gains

We believe the economic environment in the U.S. will continue on its recent trajectory of low but sustainable growth, with real GDP growth in a range of 2 to 2.8%. We also think inflation will remain low and the job market will continue its slow improvement.

“Given the slow but steady expansion of the U.S. economy, we think equities can still be a good place for investors in 2014. While market performance in the coming year may not be as robust as in 2013, we anticipate it will still offer growth opportunities and the potential for solid returns,” says Phil Sanders, Ivy Funds Chief Investment Officer and Co-Portfolio Manager of Ivy Large Cap Growth Fund. “We think 2014 market gains will be supported by improving investor sentiment, steady economic growth and healthy corporate financials.”

Although there was an uptick in sales of big-ticket, durable items – such as autos and homes – in the past year, we think the trend could moderate in 2014. On a positive note, opportunities in the non-residential market are starting to percolate as companies are beginning to invest in plant and office building construction.

Consumer spending trends remain inconsistent as many high-end retailers are experiencing stronger sales compared with their low-end counterparts. This is driven by the fact that middle- and upper-income consumers appear to have more money to spend because of rising home values and exposure to recent stock market returns.

“We think the positive developments in the U.S. around housing and autos, growth in oil and gas exploration and production, and a trend toward increased domestic manufacturing that is closer to sources of demand and inexpensive energy supplies were all supportive of growth in the domestic economy in 2013,” says Kimberly Scott, Portfolio Manager of Ivy Mid Cap Growth Fund. “We expect these trends to continue in the coming year.” .

We expect corporate profits to post modest growth in 2014, supporting higher levels of employment and capital spending.

While we think the economic environment generally favors equities, the risk of political gridlock in Washington, negative economic developments in Europe or China, or a sudden shift in U.S. monetary or tax policy could jolt the markets at any time. It does appear, however, that the political rhetoric out of Washington has softened a bit and investors have taken comfort in the fact that the global financial system is on much more solid footing.

Rate levels again are key for fixed-income market

We think the most significant issue heading into 2014 for fixed-income investors is the same as it was a year ago: When and how steeply will interest rates climb?

Mark Beischel, Ivy Funds Global Director of Fixed Income and Portfolio Manager of Ivy Global Bond Fund, says it is likely the market will see an eventual and gradual steepening of the yield curve in 2014.

“As long as the data supports the sustainability of economic expansion, the expectation is going to be that the Fed will further slow purchases of long-term assets,” Beischel says. “With that, the Fed is also going to begin to transition to providing more emphasis on its forward guidance of maintaining the fed funds rate low for a long period of time.”

The forward guidance may be especially critical. The Fed has struggled to communicate clearly to the market in the past and has emphasized that tapering is not an immediate precursor to an interest rate hike. While an eventual rate hike could come in 2015, Beischel says it could be pushed into 2016 if the Fed believes inflationary pressure remains well contained.

For investors in 2014, we think the result may be an environment similar to 2013: The short end of the yield curve remains well anchored while the curve from 10 years out exhibits more volatility, moving with market sentiment on monetary policy and fiscal concerns in Washington.

Municipal bonds, which are closely correlated with Treasuries, will remain especially sensitive to potential rate moves in 2014 and continue some of the pain felt in 2013, according to Bryan Bailey, Portfolio Manager of Ivy Municipal Bond Fund. However, Bailey believes the return profile may become more attractive later in the year, depending on the speed and magnitude of expected increases.

Beyond the rate environment in 2013, municipal-bond markets also suffered bouts of volatility related to the fiscal turmoil in Detroit, Puerto Rico and other municipalities. While these events have created negative headline pressure on the market, Bailey believes the overall sector remains healthy.

We think a third issue of concern for municipal-bond investors in 2013 – the potential reduction or elimination in the municipal-bond tax exemption – appears highly unlikely to gain traction in 2014. The market may set this aside until campaigning begins for the 2016 elections.

International equities likely to retain value

Central bankers and politicians, particularly in the U.S., continued to hold sway over international markets in 2013. International equities closed the year at levels that are in line to slightly above their historical averages over the last 25 years, while bonds were at a significant premium.

“This year, for the first time since the downturn of 2008, we are seeing money flow from bonds to equities rather than the reverse. As long as this continues, it will support equity market returns,” says John Maxwell, Portfolio Manager of the Ivy International Core Equity Fund. “We feel equities should trade at a discount to their long term averages as prospects for global growth are lower, but the relative value case remains attractive.”

We believe improvement in economic growth in 2014 eventually will lead to tighter monetary and fiscal policy in the developed economies. In Japan, we think an increase in the supply of the Japanese yen should help assets denominated in yen rise in value. However, at some point we think the country’s aggressive monetary stimulus efforts to weaken its currency and stoke inflation may become tenuous if not monitored effectively.

Longer term, we think emerging economies, including India and Brazil, will continue seeking to improve their overall standard of living. But their ability to accomplish this change is in question in the near term, especially as some show signs of stress from the potential for further tightening in monetary policy and general uncertainty over the economic direction. Within Asia, we believe that an ongoing urbanization trend, excellent demography and a high savings ratio will continue to strongly drive the Asian economy for the foreseeable future. As more individuals achieve middle-class status we believe consumption and infrastructure themes bode well for opportunistic investing.

China pursues economic reform

China in late 2013 announced an ambitious economic plan covering reforms in 16 major areas with a target of 2020 for “decisive” results. Among the plan’s key objectives:

- Reform the system of dominant state-owned enterprises and promote the private sector of the economy, including allowing private banks and more open markets.

- Reduce limits on foreign investment.

- Liberalize prices on major commodities.

- Open household registrations in small- and mid-size cities and get permits for work, education, health care, etc.

- Give farmers land title and allow title trading.

“We are encouraged by China’s plan, which is the most far-reaching in more than 20 years,” says Mike Avery, Executive Vice President of Ivy Investment Management Company and Co-Portfolio Manager of Ivy Asset Strategy Fund. “It could be the most dramatic since Deng Xiaoping announced the opening of China’s economy in 1978,” he says.

Avery says the plan reinforces Ivy Funds’ view that China’s leaders want to grow the economy by increasing domestic consumption and improving standards of living, not by continuing government spending and exports.

Past performance is no guarantee of future results. Past performance is no guarantee of future results. The opinions expressed in this article are current through January 2014. Opinions are subject to change at any time based on market and other current conditions, and no forecasts can be guaranteed.

Risk factors. Investment return and principal value will fluctuate, and it’s possible to lose money by investing. International investing involves additional risks, including currency fluctuations, political or economic conditions affecting the foreign country, and differences in accounting standards and foreign regulations. These risks are magnified in emerging markets. Investing in mid-cap stocks may carry more risk than investing in stocks of larger more well-established companies. Investing in companies involved primarily in a single asset class (large cap) may be more risky and volatile than an investment with greater diversification. Fixed-income securities are subject to interest-rate risk and, as such, the net asset value of the Fund may fall as interest rates rise. Municipal bond funds may include a significant portion of investments that will pay interest that is taxable under the Alternative Minimum Tax (AMT). These and other risks are more fully described in the Fund’s prospectus. Not all funds or fund classes may be offered at all broker/dealers.

The Standard & Poor’s 500 Index is an unmanaged index of common stocks that generally is considered to represent the U.S. stock market. It is not possible to invest directly in an index. The S&P 500 Index is a product of S&P Dow Jones Indices LLC (SPDJI) and has been licensed for use by Ivy Investment Management Company (IICO). Standard & Poor’s®, S&P® and S&P 500 Index are registered trademarks of Standard & Poor’s Financial Services LLC (“S&P”); Dow Jones® is a registered trademark of Dow Jones Trademark Holdings LLC (Dow Jones); and these trademarks have been licensed for use by SPDJI and sublicensed for certain purposes by IICO. IICO’s Ivy Funds are not sponsored, endorsed, sold or promoted by SPDJI, Dow Jones, S&P, their respective affiliates, and none of such parties make any representation regarding the advisability of investing in such product(s) nor do they have any liability for any errors, omissions, or interruptions of the S&P 500 Index.

Investors should consider the investment objectives, risks, charges and expenses of a fund carefully before investing. For a prospectus, or if available, a summary prospectus, containing this and other information for the Ivy Funds, call your financial advisor or visit www.ivyfunds.com. Please read the prospectus or summary prospectus carefully before investing.

© Ivy Funds Investment Management