In the spirit of year-end prognostication, here’s my annual review of secular trends and historic behaviors that are likely to influence key markets in 2014.

US Equities

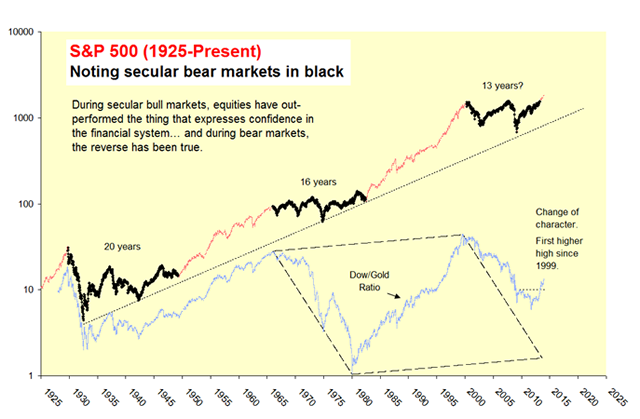

From a behavioral perspective, US equities entered a secular bull market in 2013, “breaking out” above their 13-year range, and doing so in grand style. The equity breakout was corroborated by a reversal in the Dow/Gold ratio which, in April 2013, posted its first higher high since 1999.

Chart 1 – S&P 500 and Dow/Gold Ratio

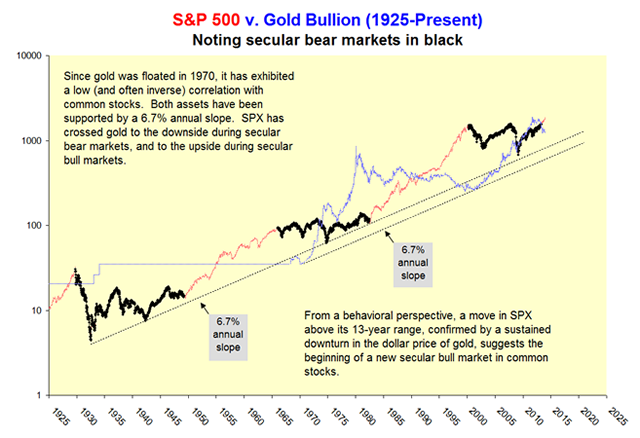

Chart 2 – SPX v. Gold (Alternative View)

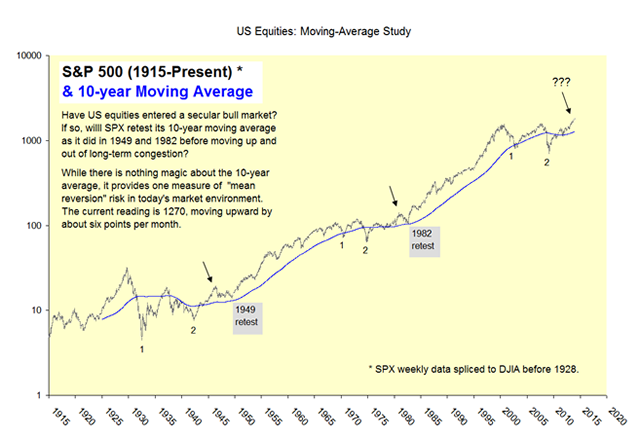

Does this make me wildly bullish on stocks? No. Equities are over-extended from a cyclical perspective, making them vulnerable to cyclical correction in months ahead. While the secular trend has turned bullish, the cyclical advance since October 2011 seems to be running on borrowed time. Risk #1 : A four-year-cycle low is due in 2014 or 2015, depending on whether one uses the old calendar interval (1998, 2002, 2006, 2010, etc.) or a four-year count from the 2011 bottom. Risk #2 : The stock-to-bond ratio is near the high end of its historic range, providing a likely catalyst for the next cyclical correction. The moving-average study below, while not meant to be predictive, provides one measure of risk in today’s market environment.

Chart 3 – How low might a “normal correction go?

Summary: US equities have apparently entered a secular bull market that should be measured in years, if not decades. A cyclical downturn to test the breakout level near SPX 1550, or the 10-year moving average near 1350, would be entirely normal from a behavioral perspective. Both the four-year cycle and the stock-to-bond ratio suggest an upcoming correction of cyclical proportion.

US Bonds

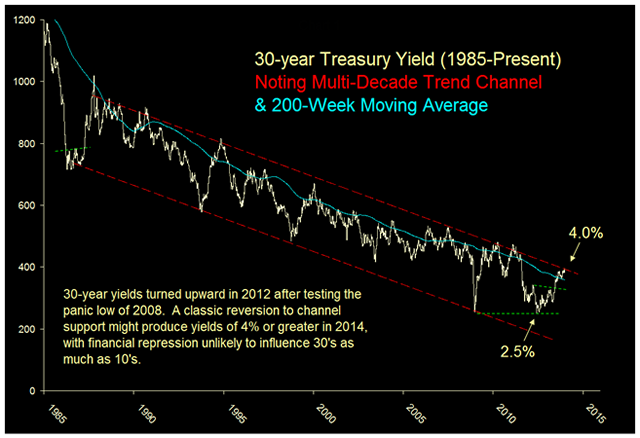

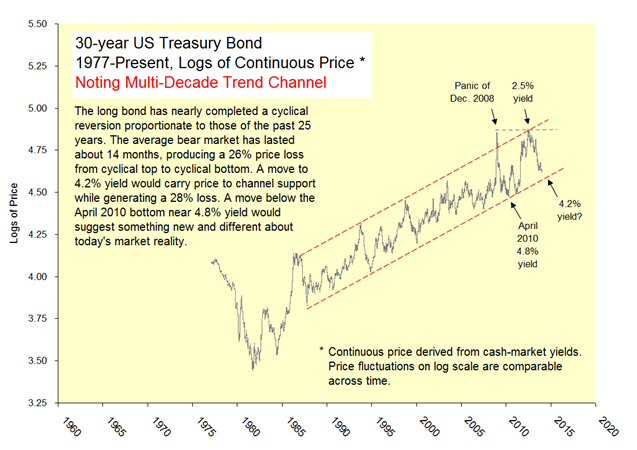

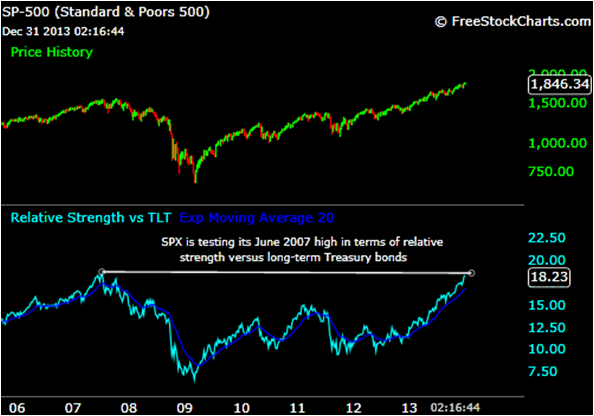

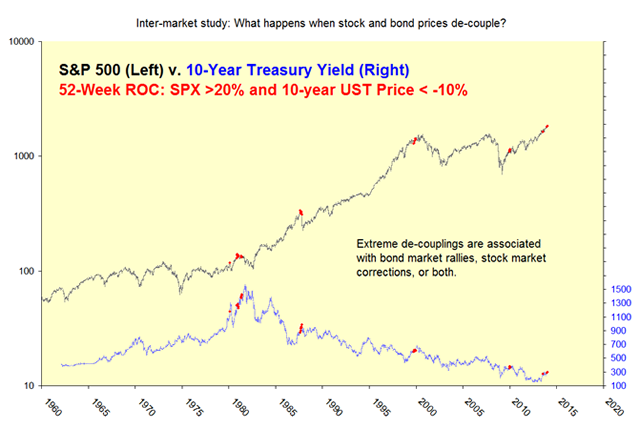

After 30+ years of downward trajectory, long-term US Treasury yields may have reached a secular trough in July 2012. A move above the 2011 peak of 4.8% yield on 30’s is needed to corroborate the secular-bear-market thesis. Meanwhile, bonds have completed, or nearly completed, a normal cyclical reversion, raising the odds of a bond market rally. The stock-to-bond ratio is at the high end of its historic range, suggesting a bond market rally, a stock market correction, or both.

Chart 4 – 30’s are near channel support.

Chart 5 – 10’s are near “repression channel” support.

Chart 6 – On a price basis, the sell-off looks nearly complete.

Chart 7 – The stock-to-bond ratio is testing its 2007 high.

Chart 8 – Extreme de-couplings have signaled market pivots.

Summary: US Bonds are near multi-decade channel support, suggesting the opportunity for a cyclical rally, perhaps in combination with a stock market correction. Rumors of a secular bear market in bonds are premature. A higher high in long-term yields (above 4.8% on 30’s) is needed to corroborate a secular reversal. If a secular bear market is in fact underway, the transition might require years of cyclical “sideways” action, as was the case from 1936-1956. Question: Can bonds complete a cyclical rout without a single Fed tightening? Answer: Yes, it’s already occurred once, from December 2008 to April 2010.

Gold

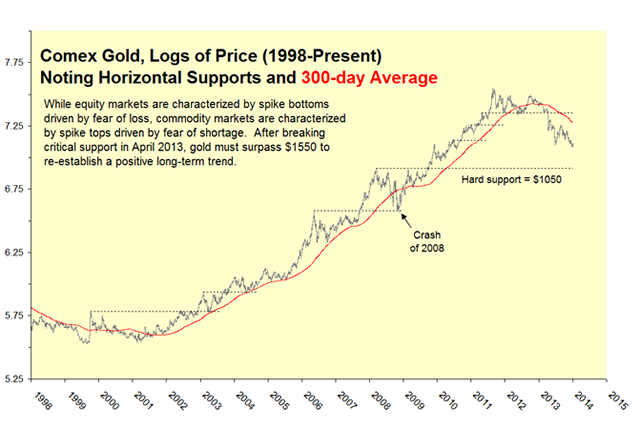

The long-term trend in $/Gold was severely damaged in April 2013 when price broke down from an otherwise normal 20-month consolidation. It should be noted that gold was similarly damaged near the middle of the 1970’s bull market, losing 40% from 1974-1976, before rising eight-fold into January 1980. A single historic example, however, is of little use. Gold must surpass the break-down area near $1550 to re-establish a positive long-term trend. Comment: In an age of global money printing, it’s hard to fathom why gold should perform so poorly. A market that tanks on bullish news, however, is particularly weak.

Chart 9 – Gold must surpass $1550 to repair its long-term trend.

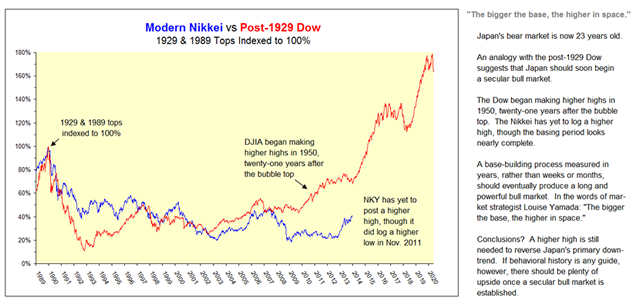

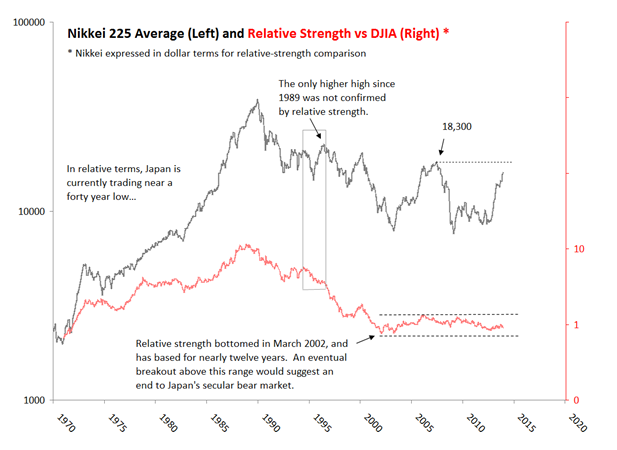

Focus: Japan

Japanese equities are entering the 24th year of a secular bear market, comparable to the post-1929 Dow Jones Industrial Average. In terms of relative strength versus DJIA, the Nikkei bottomed in 2002 and has based for nearly twelve years. An eventual breakout above this range would suggest an end to Japan’s secular bear market.

Chart 10 – Modern Nikkei v. Post-1929 Dow

Chart 11 – Relative Strength v. DJIA (1970 – Present)

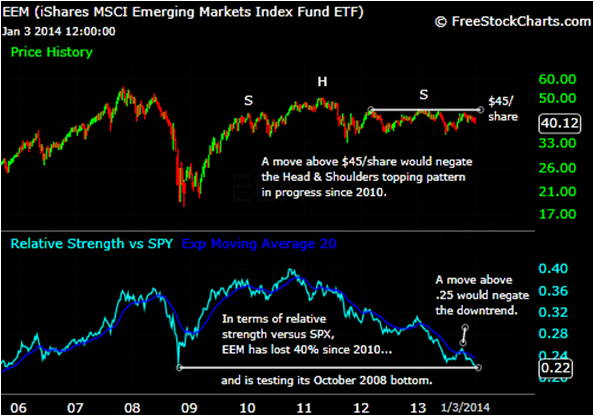

Focus: Emerging Markets

Emerging markets have performed dismally over the past three years, underperforming the S&P 500 by a whopping 40%. The bellwether MSCI index (EEM) has traded sideways since 2010, suggesting either a topping process or a base-building process. In terms of relative strength versus the S&P 500, EEM is currently testing its 2008 bottom – a pretty severe threshold for any macro market, even in relative terms. A convincing move above $45/share would establish a major uptrend, especially if corroborated by a higher high in relative strength.

Chart 12 – EEM is worth watching in 2014.

Wrap…

US equities appear to have entered a secular bull market. US bonds are due for a cyclical rally, perhaps in combination with an equity correction. Gold must surpass $1550/oz. to repair its long-term trend. Japanese and emerging-market equities both bear watching in 2014, as both have potential to establish powerful uptrends after long basing periods. An overstretched stock-to-bond ratio is the stand-out feature in today’s technical landscape.

© Charter Trust Company