The Big Transition: A Letter to an Entrepreneur Friend

In the early 1990s one of my young colleagues convinced me to accompany him on a visit to Silicon Valley, the hub of high-tech America. Back then, Tocqueville’s traditional clientele consisted largely of “old money” inheritors, but we were quite aware that large fortunes were being made in new technologies. With a good performance record and a nice story to tell about our firm and (we thought) our value approach to investments, it seemed that we should be a natural choice as money manager for this sophisticated “new money” crowd.

Our early enthusiasm was somewhat tempered by the chief financial officer of then high-flying Intel. Our story was worthwhile, he said, but no one in Silicon Valley would be interested to invest in “value” companies selling at low prices but without growth stories. Essentially, “anything growing at less than 20-25 percent per year is below their interest radar,” he told us.

We were still not discouraged and decided that it was worth committing a (very) small advertising budget to get our story out. To the right is a sample of the cute ads we ran in the trendy tech magazine WIRED.

This short-lived campaign-on-a-shoestring must have set a record in the annals of advertising, with exactly ZERO response. Our Intel friend had been right.

Fast-forward 20-odd years to the present.

Over that time span, I developed friendly relationships with a number of young entrepreneurs – mostly because I was interested to learn about their sector of activity, but also because I was curious about how they coped with the early stages of a growing business, a voyage I had personally taken earlier in my career. Many of these people were in their late 20s when I first met them; over time, I became an informal adviser to a number of them – not so much about investments, since most of their money was tied up in their businesses, but about personal, career, and patrimonial matters. Eventually, however, as capital began to be freed from their enterprises, a few not surprisingly became investment clients.

Then, more recently, a sporting friend asked to see me. A senior executive of one of the most successful public companies in the Internet sphere for 10 years, he had had an epiphany: “I suddenly realized that almost 90 percent of my personal fortune is in the shares of my company. Is this safe?” This is the gist of my answer, starting with the obvious:

This is not primarily an investment question. In fact, we have three analysts who follow your company, and they all like the stock: The growth potential remains substantial (but you are better able to judge this than are we), and even for value investors like us, the shares are not that expensive, especially when compared to recent IPOs in your sector. So, if this were solely an investment question, I would advise you to hold your stock. But this is first and foremost a patrimonial question, which must be considered in a much longer time frame.

I am a firm believer that more money is lost or wasted through wrong life choices than through wrong stock market decisions. And at this stage, to diversify or not to diversify is, for you, a true life choice.

Even if at some point in the future you decided to go into another venture, you would be at an age when one does not invest all of one’s capital in a single project. You will need a more diversified nest egg as a backstop – for your security and your family’s.

So, you have to start diversifying at some point; and, because it will probably be psychologically more difficult than you realize or than estate-planning manuals make it sound, it should be progressive.

For one thing, for the past 10 years, you and your family have lived under a security umbrella, both psychologically and in practice: predictable income, insurance, health and other benefits, etc. It may generate some angst, especially for your spouse, who is no longer working, even to contemplate a move from under that umbrella – even though this is unavoidable when, at some point, you become rentiers and live off the fruits of your prior labors. This is exactly why it is essential to start diversifying in small increments, early and progressively.

For another thing, it is entirely possible that your diversified portfolio will underperform the shares of your high-flying company in the stock market for a period of time. And diversification may also bring with it some capital-gains taxes that might only have affected you later in your one-stock patrimony. You should be aware of those possibilities and become reconciled with them. They are for your greater, ultimate benefit.

I am sure you see your company’s stock price every day in the media. But you probably are not watching it the way you would watch the less-familiar stocks in a portfolio. The reason is that you are in your company and you are comfortable with how things are going, even when the share price weakens temporarily. Once you own shares of companies where you are just an outside observer with no control over the fate of those shares, you will tend to fall prey to the insecurities that affect most investors. One of those is to assume unconsciously, when a stock goes down, that someone knows more than you do and that, perhaps, you should sell. When you know a company well, the lower the stock price the more attractive the investment. When you don’t know a company as well, the crowd seems smarter.

The advantage of starting small with your diversification is that, if your diversified portfolio underperforms your company’s stock for a while, it will affect a relatively small portion of your wealth, and you will not be tempted by rash, ill-advised impulses. Thus, it will not jeopardize your diversification plan. Of course, over time, as your company matures, the comparisons will become easier; but the point is to get accustomed to the normal, cyclical, and sometimes volatile behavior of a stock portfolio, even a well-managed, conservative one.

Two more caveats, based upon this observation: By nature, entrepreneurs think that they can understand everything. But the skill set to be a good entrepreneur is not the same as the one to be a good investor.

First, the types of decisions are not the same. Stock market investors have no say in management decisions. If they disagree with management’s strategies or moves, all they can do is sell their investment. But, at least, they can sell – and presumably will, if they think the share price has gotten too expensive, for example. This is not an option (at least not an easy one) for entrepreneurs whose only recourse, if they find their shares overpriced, is to take over a cheaper company – often an elusive strategy.

And second, there is a tendency for entrepreneurs to prize the best companies in a sector. Successful investors, however, always pay attention to price as well. I need not remind you that, in the late 1990s, there was an overwhelming favorable consensus on Wall Street about Cisco System’s quality and growth potential. And indeed, their revenues, earnings, and cash flows either tripled or quadrupled since 1999. Nevertheless, anyone who bought the shares since then either lost or made very little money: After peaking at $80, the stock currently trades around $22, and now, of course, investors are worried about the future. For stock market investors, price counts – at least as much, and sometimes even more than, quality or expected growth.

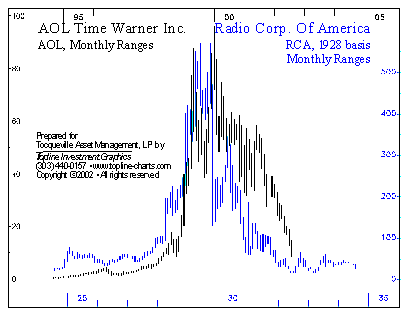

Just as another warning, beware of companies and industries that are going to change the world. They may well do so, but that is no guarantee that they will make money for investors. In December 1999 I wrote a paper making a fairly compelling parallel between radio in the 1920s and the Internet in the 1990s (“AOL, RCA, and the Shape of History”). Nearly three years later, I was able to publish the following chart, which superimposes the stock prices of RCA and AOL during their booms and busts. Net-net no money was made in the market, though radio and the Internet did indeed change the world.

I don’t want my friendly advice and assorted caveats to scare you away from a plan to diversify, but neither do I want it to sound like a sales pitch for our firm or for value investing in general. Still, as I said at the start, this is not an investment decision. You can try your slow experimentation with a couple of good mutual funds or directly with a managed portfolio. The experience will be very instructive, and you will be better prepared when the decision – someday – is imposed on you.

François Sicart (in Mexico)

1/1/2014

This article reflects the views of the author as of the date or dates cited and may change at any time. The information should not be construed as investment advice, nor is there any guarantee that any projection, forecast or opinion will be realized.

References to stocks, securities or investments in this writing should not be considered recommendations to buy or sell. Past performance is not a guide to future performance. Securities that are referenced may be held in portfolios managed by Tocqueville or by principals, employees and associates of Tocqueville, and such references should not be deemed as an understanding of any future position, buying or selling, that may be taken by Tocqueville. We will periodically reprint charts or quote extensively from articles published by other sources. When we do, we will provide appropriate source information, including hyperlinks to websites we borrowed from. The quotes and material that we reproduce are selected because, in our view, they provide an interesting, provocative or enlightening perspective on current events. Their reproduction in no way implies that we endorse any part of the material or investment recommendations published on those sites.

Source: Tocqueville

Author: François Sicart

© Tocqueville Asset Management