Weighing the Week Ahead: Will "Good News" be Good for Markets?

Suppose you knew -- right now, at the start of the week -- that the payroll employment report would show an extreme number. With 200K jobs expected, suppose it were to be 350K? Or 50K? If you had advance information fromMr. Beekswould you even know what to do?

This week the market will ask "Is good newsreally good news?"

Or the opposite.

Last Week Recap

Last weekI suggestedthat a holiday-interrupted week with little data would invite a focus on predictions for the new year. This was pretty accurate. Those working at trading desks experienced some of the lowest volatility in recent memory and also low volume. I also guessed that Fed talk from the American Economic Association meeting in Philadelphia might move markets a bit. That was accurate, but the move was a very small bit!

This Week's Theme

The focus on Friday's jobs report is obvious, but the market reaction is not. In recent years all economic news has been interpreted by asking how it might change Fed policy. There have been two schools of thought.

- Those who believe that asset prices are strictly the result of Fed policy. For these people, good news is bad.

- Those who see the Fed impact as marginal and diminishing. For these people the economy, earnings, and reduced fear are the driving market forces.

With the Fed's announcement of the beginning of the end for QE, market participants have more definition for future policy, including assurances of low short term rates for a long time. The reaction to last month's employment report suggested that good news would now be good. The markets have continued to rise over the last few weeks, but some do not think this is meaningful.

The unusual mid-week holidays have created an extended period of vacations for the "A-Teams" at many firms. As a result, some question the market message from the last few weeks. Now that these guys (pictured here) are back on the trading desks, we can expect to get a better read on market reactions.

I have my own guess, while I will offer in the conclusion. First, let us do our regular update of the last week's news and data. Readers, especially those new to this series, will benefit from reading thebackground information.

Last Week's Data

Each week I break down events into good and bad. Often there is "ugly" and on rare occasion something really good. My working definition of "good" has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially -- no politics.

- It is better than expectations.

The Good

Most of the important recent news was good.

- Chances for avoiding another debt ceiling fight are improving. GOP strategists see better chances from emphasizing ObamaCare and avoiding another government shutdown. This is consistent with what I have reported in the past. (SeeThe Hill).

- TARP has concluded and the taxpayers actuallyshowed a profit– at least from this part of the stimulus.

- ISM manufacturing beat expectations and the internal elements were also mostly positive.Steven Hansenhas a comprehensive analysis.

- Gasoline prices for 2013 were the lowest in four years, and are expected to decline furtheraccording to AAA.Doug Shorthas his typically fine chart showing the data since 2000.

- Merger activity picked up especially in the latter part of the year. David Gelles'swell-researched DealB%K articlecites both the restructuring encouraged by lower interest rates and a longer term, more strategic focus by companies.

- Consumer confidence from the Conference Board produced a slight beat of expectations. It is still below the long-term average trend. See theanalysis and chartsfrom Doug Short.

The Bad

There has not been much fresh bad news. This week's items are unusually minor with respect to trends and expectations. Feel free to suggest more items in the comments

- The Fed could increase rates faster if needed,according to Philly Fed PresidentPlosser. He is a voting member of the FOMC this year and regarded as one of the more hawkish members. The comment was actually pretty consistent with prior Fed statements about what could change policy, but it moved the market by 30 bps or so on a slow day.

- Income inequality is getting worse and causing assorted negative effects.Bloombergpulls together recent economic and survey data to provide a comprehensive report. (HTMark Thomawho notes that the median income is less than in 2007). Doug Shortcharts the progress:

- George Soros is worried about China (ViaJosh Brown). He ismore positive about the USand the rest of the world.

- China's PMI hit a three month low,although it was in line with expectations and the "flash" reading. (ViaBusiness Insider).

- Pending home sales increased only slightly, below expectations. (SeeCalculated Risk).

- Auto sales for December showed disappointing growth of 2.3%.Calculated Risk charts the trendon a multi-year basis.

The Ugly

Heightened conflict in Iraq.Al-Qaeda-linked force captures Fallujah amid rise in violence in Iraqis the Washington Post headline. U.S. forces withdrew over two years ago.

Noteworthy

There is plenty of good advice and more than a few chuckles in Josh Brown's annual "What I Learned" piece.

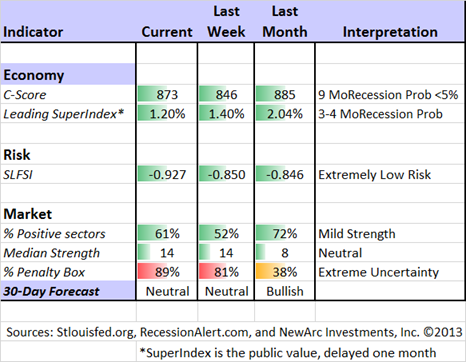

Quant Corner

Whether a trader or an investor, you need to understand risk. I monitor many quantitative reports and highlight the best methods in this weekly update. For more information on each source,check here.

Recent Expert Commentary on the Economy

Doug Short: Continuing discussion of the ECRI commentary and some alternatives.

Georg Vrba: Takes a look atpotential stock returns through 2020, using the 5-year Shiller CAPE. He also discusses some other popular analyses, and the potential for a rocky path. Georg's conclusion is as follows:

| Thus the historic trend forecasts a probable gain of about 40% for S&P-real over the next six years. The worst scenario would be a possible loss of about 25%, and the best outcome would be an approximately three-fold increase of the current price. |

The Week Ahead

This is a big week for data.

The "A List" includes the following:

- Monthly employment report (F). Most widely followed and most visible to the public.

- Initial jobless claims (Th). Best fresh data on employment.

- FOMC minutes (W). More color on the tapering decision.

The "B List" includes:

- ADP employment change (W). A good alternative to the "official" number.

- ISM services (M). Good complement to the manufacturing series, but a shorter history.

- Factory orders (M). November data.

- Trade balance (T). November data, but a bearing on Q4 GDP.

We will also get some retail sales comparisons from private releases.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a "one size fits all" approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has remained in neutral, although we are fully invested in the top three sectors. Felix's ratings have been in a fairly narrow range for several months. The rapid news-driven shifts are not the ideal conditions for Felix's three-week horizon. The ratings are slightly positive, and many sectors in the penalty box.

Insight for Investors

The start of a new year brings an avalanche of new ideas. One of the most eagerly awaited lists comes from Eddy Elfenbein, who "locks" his picks for the full twelve months, rotating five of the selections each year. Take a look at hischoices for this year. (My own valuation methods often lead to some of the same conclusions). Eddy also has a great wit, which you can enjoy both on his blog and byfollowing him on twitter.

Take a few minutes to read thestory behind the Wolf of Wall Street scam– how people were really fooled. Could it happen again? An expert seems to think it is possible.

Josh Brown highlightssome great investment advice from Joe Mansueto, chief executive of Morningstar. (Theentire WSJ team articleis worth your time to read). Here is part of Josh's piece:

| So investors are in many ways misled by stock-market volatility. The values of the underlying businesses just don't change as quickly as stock prices do. You really don't have to watch those changes hawklike day after day.

It is in a lot of people's interests to get you to do something. |

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Each week I try to highlight something special for the long-term investor. My own current investor recommendations aresummarized here. I will also have my regular annual preview in the next week or so.

And finally, we have collected some of our recent recommendations in anew investor resource page-- a starting point for the long-term investor. (Comments and suggestions welcome. I am trying to be helpful and I love feedback).

Final Thought

A better economy will benefit both businesses and consumers. Corporate earnings will grow and companies will be more valuable. Eventually, good news will be good news.

Those who have been wrong about the economy and the markets have taken the popular course:Blame the Fed!

When tapering on a data dependent basis was suggested by Bernanke, the market had a "delayed reaction" including rising rates and falling stocks. This was widely embraced – despite the delay and the nuanced guidance – as "tapering is tightening." Assorted pundits explained that the very beginning of the end of QE would lead markets to price in the entire Fed policy shift, even if it was expected to take several years.

Many of the same sources are now suggesting that the latest Fed announcement has NOT been priced in. Why not? It was only an announcement of something that will begin in January. December saw the full complement of dollars "pumped into the economy."

Neither of these arguments makes any sense. They serve only to allow those who have been mistaken to cling to their viewpoints for a little bit longer.

This week's news – including both the FOMC minutes and the employment report – will inform us all if we have finally gotten past the fixation on the Fed.

Originally posted at Jeff's blog:A Dash of Insight

© New Arc Investments