It was the best of times, it was the worst of times, it was the age of wisdom, it was the age of foolishness …

Charles Dickens in a Tale of Two Cities

This commentary is divided into three sections. I begin with a review of current U.S. and foreign stock markets, examining the year 2013 and the past six years, including the crash of 2008. This perspective serves as a launch point into the future, specifically 2014 and the remainder of this decade. I conclude with a review of the past 88 years of U.S. stock and bond markets. As usual, I welcome your feedback, and hope you find my comments helpful and insightful.

Part 1: The Present

What a Difference a Year Makes

After feasting on the U.S. stock market’s 54% run-up from 2009 to 2010, we starved for performance in 2011, suffering a 1% loss. Some said the markets were due for a respite, so this lull was healthy, and they were right. Stock markets both here and abroad subsequently had a good year in 2012 followed by a spectacular 2013, generating a 54% two-year U.S. market return. The 2011 loss is sandwiched between two 54% return 2-year periods.

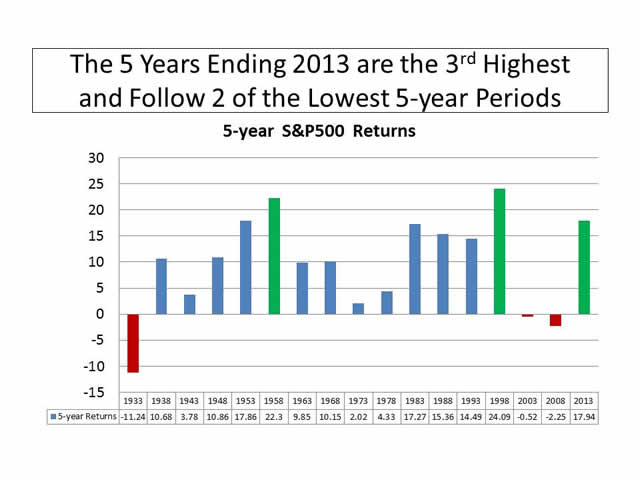

The past five years have been among the best on record, almost erasing the memory of the previous five years ending 2012, as shown in the graph on the right. These past five years produced the third highest return, as shown in the following graph, albeit it follows two of the lowest performing 5-year periods.

Source: PPCA Inc

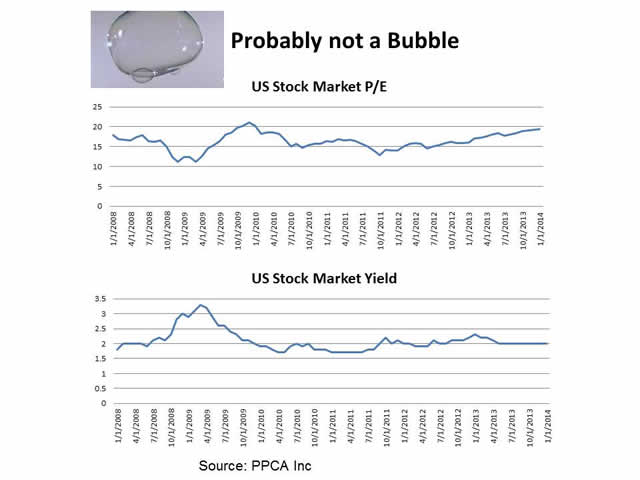

This good performance has generated concerns about another market bubble, but the graph on the right suggests otherwise. Even though stock prices have surged, both dividends and earnings have kept pace, so prices appear to be reasonable.

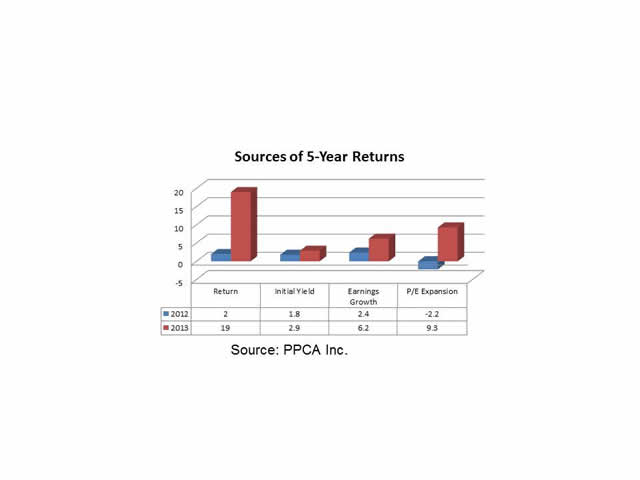

It’s useful and insightful to examine the sources of these returns. The following formula works quite well:

Return = Dividend Yield + (1 + Earnings Growth) X (1 + P/E expansion/contraction) – 1

This formula is simple yet elegant, stating that total return equals dividend yield plus sources of price change, namely the compounding of earnings growth with investor-driven changes in the price/earnings ratio. I’ll use this formula again when we discuss the future.

The components of returns for the past two five-year periods are shown in the graph on the right. As you can see, P/E expansion/contraction has been the driving force. This component is primarily driven by investor behavior, and may well be the cause of future economic results rather than being a leading indicator of the economy. In his 1998 book the Beast on Wall Street Dr. Robert Haugen contends that the market crash of 1929 caused the Great Depression, as opposed to predicting it. In other words, the market drives the economy rather than anticipating it. If so, recent P/E expansion bodes well for the economy, if this expansion continues. The big question remains: what will be the ultimate effects of quantitative easing? There’s no doubt the bond market is being manipulated and that this has a material effect on stock markets. Specifically stock buy-backs are proliferating because money is cheap. Corporations can borrow at very low interest rates to buy their own stock, which in turn drives up share prices. Can we expect buy-backs to continue when the brakes come off of interest rates? What forces will drive future P/E expansion/contraction?

America the Beautiful

The U.S. stock market has performed best, particularly in 2013, as shown in the graph on the right. Consequently there is a wide dispersion of performance among multi-asset managers, especially target date funds. The primary benefits of target date funds are diversification and risk control, both of which suffered on a relative basis in 2013. The most diversified funds underperformed their U.S.-centric competitors, as did funds with rigorous risk controls. This leads to the potential for error on the part of plan sponsors, hiring and firing investment managers for the wrong reasons.

Using the return components formula above, the U.S. stock market’s 2013 return breaks down as follows:

33% Return = 2% Dividend + (6.5% Earnings Growth compounded with 23% P/E Expansion)

As usual, some styles and sectors have thrived while others have struggled. Similarly, outside the U.S. there was a wide range of country performance. The following section examines these results.

Winners and Losers in 2013 and the 5 Years Ending 2013

U.S. stocks

Growth stocks led the way in 2013, with small-cap growth stocks performing best, earning 44%. By contrast, large-cap-core companies earned “only” 23%, and large-value earned only 28%. Other than these extremes, style returns clustered around 30%, a pretty good place to be. This has been one of those unusual periods where the “stuff in the middle” (core) has not performed in line with the “stuff on the ends.” I use Surz Style Pure® classifications throughout this commentary. It wouldn’t be surprising to see core outperform value and growth going forward, in a regression toward the mean.

On the sector front, consumer discretionary and health care fared best, earning more than 43%. By contrast, materials eked out a measly 7% return, and telephones-&-utilities also lagged with a 16% return. It was a year led by consumers, in contrast to previous periods that were led by infrastructure spending and the Chindia effect.

Looking back over the past 5 years we see that smaller companies of all styles have led the way, as have consumer-oriented stocks. The sector returns in this chart are shown in the same sequence as the year, so you can see that the big change in 2013 was in the leadership of technology stocks, which had performed relatively well prior to 2013. It’s also interesting to note that the previous 5 years (2004-2008) were led by value stocks in the energy and materials sectors. The leadership of the U.S stock market has shifted dramatically.

But the interesting details lie in the cross-sections of styles with sectors, especially if we are interested in exploiting momentum effects, as discussed in “ Part 2: The Future ” below.

Foreign stocks

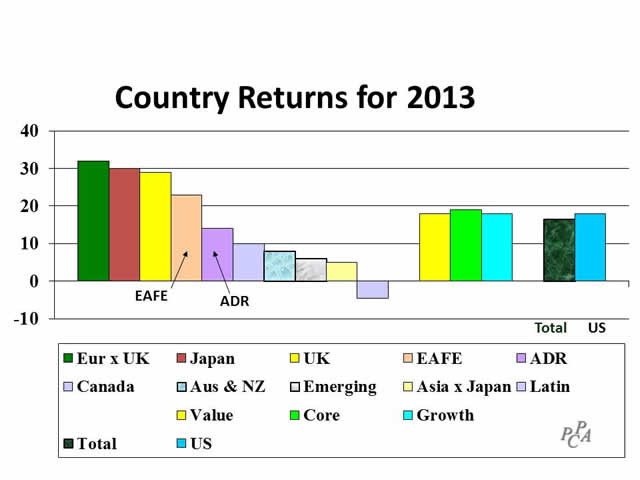

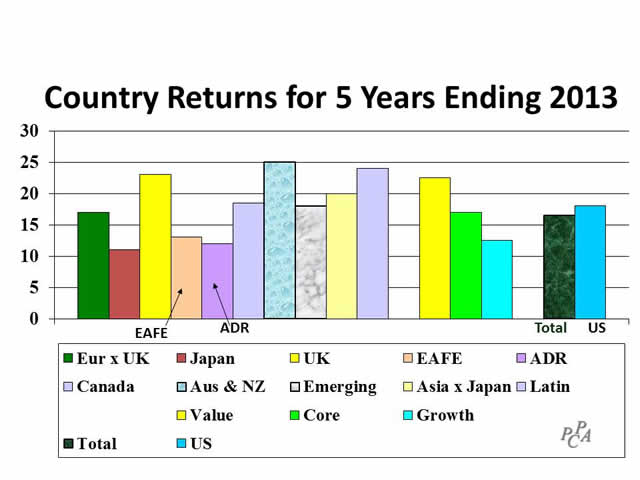

Looking outside the U.S., foreign markets earned 16.5%, lagging the U.S. stock market’s 33% return and EAFE’s 23% return. Japan and Europe are the big story, earning 30% on a dollar basis. The Japan return in Japanese yen was an even more impressive 44%. The Japanese stock market has soared this year as the yen was purposely weakened against the dollar. By contrast, all countries outside Europe and Japan earned less than 11%, and Latin America lost 4%, all in $US.

On the style front, core surprised, as it did in the U.S., but core led rather than lagged, although not by much.

Looking back over the past 5 years we see that leadership in 2013 shifted away from Latin America and Australia-&-New Zealand to Japan and Europe, and style leadership shifted from value to core. Country returns are shown in the same sequence as the current year above. Note also that EAFE and ADRs have both underperformed. This is because smaller companies have performed best, earning 20% per year while large companies have lagged with annualized returns of 16% per year (size results are not shown in exhibit).

In my 2012 Commentary, I observed that Japan had become a bargain, a deep value play, coming into 2013 -- a pretty good call. As concerns about a weakening U.S. dollar have been allayed, at least for now, interest has diminished in emerging markets, Latin America, and Australia-&-New-Zealand.

We can’t change the past or the present, but we can plan for the future, as addressed in the next section.

Part 2: The Future

In this section I provide a forecast of broad stock market returns as well as pinpoint market segments that will win and lose in the short term.

Stock Market Returns in 2014 and Beyond

You can use the components formula above to forecast future returns. Simply plug in your estimates of earnings growth and ending P/E. For example, the following table uses the formula to peer into 2014. The cell highlighted in yellow – earnings growth of 6% and an ending P/E of 15 – is the average long-term situation. In other words, if 2014 is “average” we’ll see a 16% loss next year. But what if it’s not average? The purple cells highlight a band around the average and indicate a performance range between a 13% gain and an 18% loss. By contrast, losses are not in most forecasts for 2014; see for example Economists say Happy New Year. A 16% loss is a contrarian view.

Return Forecast for 2014 (1 Year)

|

Earnings Growth |

||||||||

|

End P/E |

-4 |

-2 |

0 |

2 |

4 |

6 |

8 |

10 |

|

10 |

-49 |

-47 |

-46 |

-45 |

-44 |

-43 |

-42 |

-41 |

|

15 |

-24 |

-22 |

-21 |

-19 |

-18 |

-16 |

-14 |

-13 |

|

20 |

1 |

3 |

5 |

7 |

9 |

11 |

13 |

15 |

|

25 |

26 |

28 |

31 |

33 |

36 |

37 |

41 |

44 |

|

30 |

50 |

54 |

57 |

60 |

63 |

66 |

69 |

72 |

|

35 |

75 |

79 |

82 |

86 |

90 |

93 |

97 |

100 |

Source: PPCA Inc

We can also use the formula to look beyond 2014, to the end of the decade, as shown in the following table:

Return Forecast for 2014-2019 (6 Years)

|

Earnings Growth |

||||||||

|

End P/E |

-4 |

-2 |

0 |

2 |

4 |

6 |

8 |

10 |

|

10 |

-12 |

-10 |

-8 |

-7 |

-5 |

-3 |

-1 |

0 |

|

15 |

-6 |

-4 |

-2 |

0 |

2 |

4 |

5 |

7 |

|

20 |

-2 |

0 |

3 |

5 |

7 |

9 |

11 |

13 |

|

25 |

2 |

4 |

6 |

8 |

10 |

11 |

15 |

17 |

|

30 |

5 |

7 |

10 |

12 |

14 |

16 |

18 |

20 |

|

35 |

8 |

10 |

12 |

15 |

17 |

19 |

21 |

23 |

Source: PPCA Inc

This framework can also be used for foreign markets, which are currently near historical averages, so their expected returns are near norm, namely returns near 9%.

Despite recent market gains, or perhaps because of them, investors have been flocking into hedge funds as a defensive move. The demand for these products is sure to increase substantially in the years ahead as the crowd grapples with the harsh reality of the future. But separating the alpha wheat from beta’s chaff is crucial in the business of intelligently selecting hedge funds.

In the future, we won’t pay much for exotic hedge fund betas (risk profiles), but the market will continue to put a premium on superior human intellect. We’ll know the difference because we’ll abandon simple-minded performance benchmarks like peer groups and indexes, and replace them with the smart science envisioned in this short entertaining movie on the Future of Hedge Fund Evaluation and Fees.

Winners and Losers Forecast for 2014

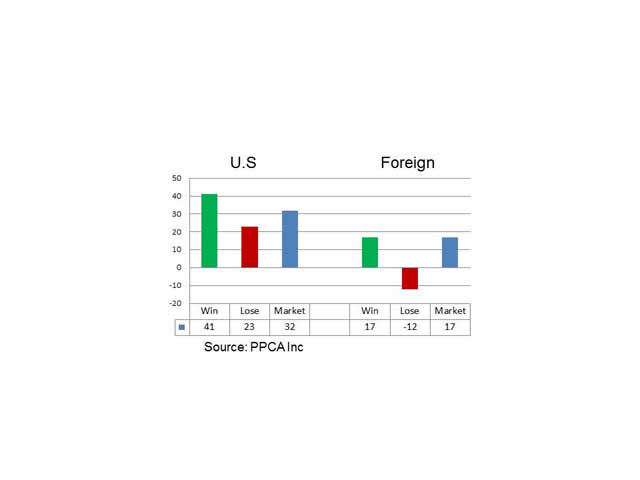

In Searching for Alpha in Heat Maps, published in early April, 2013 I showed how heat maps could be used to profit from momentum effects. I then published my forecasts each quarter, and promised to report on their success at year end, so here is that report.

Returns for forecasted winners and losers in 2013

As you can see, momentum investing worked in 2013 for investors who went long my forecasted winners and short my forecasted losers. If you simply went long my forecasted winners, you won in the U.S. but not in foreign stocks, relative to their respective markets. If you simply went short my forecasted losers, you won in foreign stocks. The momentum of lagging segments persisted to a greater extent than the momentum of winners.

So now I’ll offer forecasts for the first quarter of 2014 using heat maps. A heat map shows shades of green for “good,” which in this case is good performance relative to the total market. By contrast, shades of red are bad, indicating underperformance. Yellow is neutral.

The table below is the U.S. heat map for the year ending December 31, 2013. We see that the best performing market segment comprises $45 Billion (not shown) of small-cap-growth companies in the industrial sector, earning 62.9%. And the worst performing segment was small-cap growth in the materials sector, losing 16.7%. Many quantitative managers employ momentum in their models, buying the “green” and selling the “red.” Fundamental managers use heat maps as clues to segments of the market that are worth exploring, for both momentum and reversal potential.

U.S. Heat Map for the Year Ending December 31, 2013

|

STAP |

DISC |

HLTH |

MATL |

TECH |

ENER |

INDU |

UTEL |

FINC |

TOTL |

|

|

LGVL |

20.1 |

40.2 |

31 |

7.6 |

37.6 |

21.8 |

41.2 |

7.4 |

37.5 |

28.6 |

|

LGCO |

29.6 |

31.5 |

28.8 |

9.7 |

1.8 |

23.4 |

38.7 |

23.7 |

28.7 |

23.2 |

|

LGGR |

25.9 |

49.3 |

62 |

9.8 |

43.8 |

21.6 |

48.8 |

29.1 |

30.5 |

38.9 |

|

MDVL |

33.5 |

43.5 |

57.7 |

6.5 |

54.8 |

25.2 |

39.2 |

17.5 |

32.8 |

34.2 |

|

MDCO |

49.6 |

37.2 |

38.6 |

15.5 |

32.3 |

26.1 |

36.5 |

16.5 |

22.5 |

31.5 |

|

MDGR |

31.6 |

57.5 |

44.7 |

-1.6 |

34.9 |

24.5 |

39.7 |

24.4 |

32.1 |

35 |

|

SCVL |

51.3 |

45.4 |

42.8 |

17.9 |

48.7 |

30 |

51.1 |

24.1 |

32.6 |

37.3 |

|

SCCO |

39.6 |

48.3 |

43.3 |

7.2 |

35.7 |

38.8 |

43.5 |

15.5 |

27.3 |

36.7 |

|

SCGR |

48 |

57.7 |

58.3 |

-16.7 |

52.8 |

16.3 |

62.9 |

37 |

43.3 |

44.3 |

|

TOTL |

27.3 |

45 |

42.6 |

7.4 |

33.2 |

23.1 |

42.1 |

16 |

32.9 |

32.6 |

Source: PPCA Inc

Using this heat map, I forecast the following winners and losers for the next quarter. I’ll continue to track the results on a cumulative and quarterly basis. Let the games continue.

|

STAP |

DISC |

HLTH |

MATL |

TECH |

ENER |

INDU |

UTEL |

FINC |

TOTL |

|

|

LGVL |

15.2 |

32 |

36.2 |

-3.5 |

22.2 |

10.1 |

19.5 |

21.2 |

20.2 |

17.7 |

|

LGCO |

18.4 |

25.7 |

32.4 |

-7.5 |

32.6 |

6 |

28.3 |

13.8 |

15.1 |

18.6 |

|

LGGR |

13.2 |

30.8 |

29.5 |

-12.5 |

21.2 |

8.4 |

25.1 |

34 |

15.7 |

18.2 |

|

MDVL |

15.4 |

35.5 |

36.7 |

0.9 |

25 |

2 |

23.6 |

11.5 |

15.4 |

16.5 |

|

MDCO |

20 |

28.8 |

30.8 |

2.8 |

20.6 |

4.4 |

23.6 |

10 |

18.6 |

19.4 |

|

MDGR |

9.5 |

26.4 |

27.6 |

-8.6 |

40.2 |

6.2 |

17.5 |

5.7 |

16.8 |

16.1 |

|

SCVL |

23.1 |

24.5 |

43.6 |

11.2 |

34.2 |

6 |

27.8 |

15.8 |

22.7 |

23.2 |

|

SCCO |

14.5 |

20.2 |

31.7 |

3.9 |

28.7 |

12.6 |

23.9 |

9.6 |

16.8 |

18.7 |

|

SCGR |

13 |

20.1 |

29.7 |

-13.8 |

41 |

-5.7 |

20.7 |

16.9 |

19.3 |

16.7 |

|

UK |

20 |

45.5 |

38.3 |

-5.1 |

38.9 |

18.4 |

39.6 |

50.4 |

35.9 |

28.9 |

|

JAPN |

21.1 |

34.2 |

23 |

21.1 |

33.7 |

6.7 |

24 |

50.2 |

31.8 |

29.9 |

|

CANA |

15.9 |

37 |

61 |

-33 |

29.9 |

8.3 |

31.7 |

4.6 |

22.3 |

10.5 |

|

AUST |

5.5 |

24.1 |

15.3 |

-13.7 |

29.6 |

-5 |

3.1 |

13 |

17.7 |

7.7 |

|

APXJ |

0.6 |

16.2 |

26.2 |

-3.7 |

12.6 |

-8.9 |

9 |

4.5 |

3.5 |

5.5 |

|

EURO |

25.8 |

36.9 |

36.7 |

21 |

38.5 |

16.1 |

38.9 |

36 |

32.4 |

32.3 |

|

EMRG |

7.1 |

11.6 |

14 |

-8.4 |

42 |

6.4 |

1.4 |

4.7 |

6.5 |

5.6 |

|

LATN |

-2.4 |

-5.8 |

4.4 |

-18.6 |

15.9 |

-5.9 |

-1.9 |

-3.2 |

0.5 |

-4.6 |

|

TOTL |

14.7 |

29.2 |

31.8 |

-3.3 |

27.7 |

7.9 |

22.8 |

20.2 |

18.1 |

16.5 |

|

UK |

JAPN |

CANA |

AUST |

APXJ |

EURO |

EMRG |

LATN |

TOTL |

||

|

LGVL |

23.7 |

20.8 |

18.5 |

13.9 |

2.6 |

35.4 |

2.4 |

1.3 |

17.7 |

|

|

LGCO |

22.9 |

27.8 |

0 |

7.4 |

5.2 |

34.2 |

5.7 |

-5.3 |

18.6 |

|

|

LGGR |

31.2 |

38 |

3.1 |

-5.1 |

0.3 |

23.9 |

8.6 |

-5.1 |

18.2 |

|

|

MDVL |

31.4 |

32.8 |

5.7 |

4.2 |

4.8 |

38.6 |

9.1 |

-3.9 |

16.5 |

|

|

MDCO |

38.2 |

28.7 |

9.9 |

11.2 |

5 |

35.3 |

-0.5 |

1.5 |

19.4 |

|

|

MDGR |

42.9 |

33.4 |

0.8 |

4.4 |

7.5 |

40.7 |

1.4 |

-10.2 |

16.1 |

|

|

SCVL |

46.6 |

27.1 |

9.8 |

3.7 |

19.2 |

43.6 |

17.3 |

-3.9 |

23.2 |

|

|

SCCO |

50.3 |

23.4 |

-1.1 |

5.9 |

14.9 |

35.3 |

7.3 |

-11 |

18.7 |

|

|

SCGR |

30.3 |

36.6 |

-4.7 |

-24.3 |

17.2 |

34 |

1.7 |

-9.8 |

16.7 |

|

|

TOTL |

28.9 |

29.9 |

10.5 |

7.7 |

5.5 |

32.3 |

5.6 |

-4.6 |

16.5 |

|

Forecasts for U.S. Markets in Q1, 2014 |

|

|

High |

Low |

|

Small-cap Growth Industrials |

Small-cap Growth Materials |

|

Large-cap Growth Healthcare |

Mid-cap Growth Materials |

|

Small-cap Growth Discretionary |

Large-cap Core Technology |

Similarly, the following table is a heat map for foreign stocks in the year ending December, 2013. As you can see, healthcare stocks in Canada have thrived with a 61% return, while materials in Canada have suffered 33% losses.

Accordingly, my forecasts for foreign market returns in the upcoming quarter are as follows:

|

Forecasts for Foreign Markets in Q1, 2014 |

|

|

High |

Low |

|

Canadian Health |

Canadian Materials |

|

UK Utilities & Phones |

Small-cap Growth in Australia & NZ |

|

Small –cap core UK |

Materials in Latin America |

In the final section of this report, I provide a longer term 88-year history of stocks, bonds, T-bills and inflation. There are many lessons to be learned from this history.

Part 3: The Past

The 88-year history of the U.S. capital markets

The table on the following page shows the history of risk and return for stocks (S&P 500), bonds (Citigroup high grade), T-bills and inflation. There are many lessons in this table, so it’s worth your time and effort to review these results. For example, here are a few of the lessons:

- T-bills paid less than inflation in 2013, earning 0.09% in a 1.4% inflationary environment. We paid the government to use their mattress, as we have for the past ten years, with a 1.64% return in a 2.35% inflationary environment.

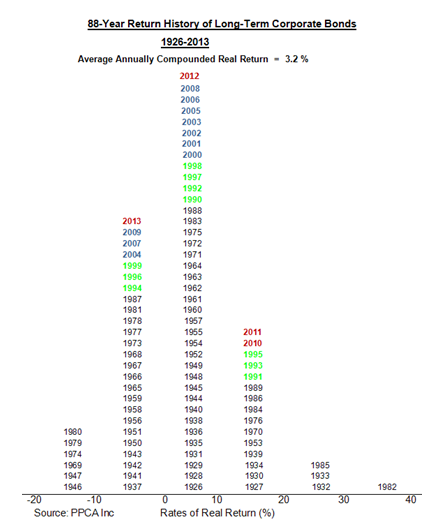

- Bonds were more “efficient,” delivering more returns per unit of risk than stocks in the first 44 years, but they have been about as efficient in the most recent 44years. The Sharpe ratio for bonds is .45 versus .35 for stocks in the first 44 years, but the Sharpe ratio for both is about the same in the more recent 44 years, at .31 for stocks and .32 for bonds.

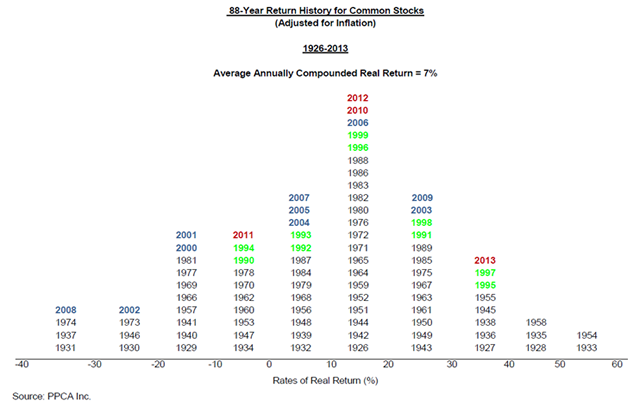

- The past decade has been the third worst for stocks across the past eight consecutive 10-year periods. The decades 1934-1943 and 1964-1973 were slightly worse.

- Average inflation in the past 44 years has been about 2.5 times that of the previous 44 years: 1.75% in 1926-1969 versus 4.26% in 1970-2013.

- Long-term high-grade corporate bonds have fared reasonably well in the last five years, earning more than 4% per year above inflation, which is surprising in light of low interest rates. America has benefitted from confidence in the U.S. dollar, resulting in decreases in interest rates.

- The 8.59% standard deviation of monthly stock returns in 2013 is less than half the historical average of 19%. It was a year that went up month after month, with only a couple exceptions in June and August. High return with low risk.

MARKET HISTORY FOR YEARS ENDING DECEMBER, 2013

stocks bonds t-bills cpi

--------------------- --------------------- -------------- --------------

RETURN STNDEV SHARPE RETURN STNDEV SHARPE RETURN STNDEV RETURN STNDEV

------ ------ ------ ------ ------ ------ ------ ------ ------ ------

2013(1 Year) 32.39 8.59 3.86 -2.13 3.19 -.69 .09 .02 1.40 .99

______________________________________________________________________________________________

1926-2013(88 YRS) 10.08 19.00 .33 6.15 7.35 .34 3.54 .89 3.00 1.82

______________________________________________________________________________________________

1926-1969(44 YRS) 9.75 21.96 .35 3.87 4.32 .45 1.84 .49 1.75 2.20

1970-2013(44 YRS) 10.41 15.49 .31 8.48 9.41 .32 5.27 .93 4.26 1.25

______________________________________________________________________________________________

1934-1943(10 YRS) 7.17 23.50 .30 6.20 2.33 2.60 .14 .05 2.88 2.07

1944-1953(10 YRS) 14.31 12.85 1.03 3.13 4.34 .50 .96 .16 4.43 2.83

1954-1963(10 YRS) 15.91 13.02 1.02 2.65 4.15 .08 2.32 .25 1.40 .75

1964-1973(10 YRS) 6.01 12.40 .08 2.93 6.78 -.29 4.98 .37 4.12 .87

1974-1983(10 YRS) 10.61 16.36 .11 6.43 12.50 -.17 8.65 .89 8.16 1.27

1984-1993(10 YRS) 14.92 15.58 .51 13.82 7.86 .87 6.57 .61 3.69 .73

1994-2003(10 YRS) 11.10 15.92 .41 7.57 6.49 .49 4.29 .46 2.56 .61

2004-2013(10 YRS) 7.41 14.62 .39 5.96 10.21 .41 1.64 .55 2.35 1.51

______________________________________________________________________________________________

1929-1933( 5 YRS) -11.24 47.12 -.27 8.17 6.19 .97 1.89 .50 -5.14 2.78

1934-1938( 5 YRS) 10.68 25.98 .40 7.70 2.29 3.31 .15 .05 1.33 1.88

1939-1943( 5 YRS) 3.78 20.88 .17 4.73 2.33 1.97 .13 .05 4.45 2.16

1944-1948( 5 YRS) 10.86 14.66 .71 2.43 1.94 1.00 .46 .07 6.67 3.55

1949-1953( 5 YRS) 17.86 10.82 1.49 3.83 5.85 .40 1.45 .10 2.23 1.67

1954-1958( 5 YRS) 22.30 13.10 1.52 .96 4.93 -.19 1.91 .27 1.49 .88

1959-1963( 5 YRS) 9.85 12.87 .54 4.36 3.15 .51 2.72 .18 1.31 .60

1964-1968( 5 YRS) 10.15 10.37 .54 .37 5.18 -.74 4.32 .19 2.84 .62

1969-1973( 5 YRS) 2.02 14.16 -.24 5.55 8.05 -.01 5.64 .42 5.41 .93

1974-1978( 5 YRS) 4.33 17.59 -.10 6.03 7.80 -.03 6.24 .40 7.94 .94

1979-1983( 5 YRS) 17.27 14.98 .36 6.83 15.94 -.25 11.13 .75 8.39 1.53

1984-1988( 5 YRS) 15.36 17.95 .43 15.03 9.62 .77 7.21 .48 3.51 .71

1989-1993( 5 YRS) 14.49 12.92 .63 12.62 5.64 1.12 5.93 .68 3.88 .74

1994-1998( 5 YRS) 24.09 13.86 1.32 7.22 5.68 .37 5.05 .20 2.56 .42

1999-2003( 5 YRS) -.52 17.29 -.23 7.91 7.25 .58 3.53 .55 2.55 .76

2004-2008( 5 YRS) -2.25 12.84 -.41 5.81 11.61 .22 3.19 .46 2.76 1.86

2009-2013( 5 YRS) 17.94 15.83 1.13 6.12 8.69 .69 .11 .02 1.94 1.05

Source: PPCA Inc.

Additional perspective is provided by the following histograms of stock and bond returns.

© PPCA Inc