Weighing the Week Ahead: How Should Investors Judge the Prospects for 2014?

Advisor Perspectives welcomes guest contributions. The views presented here do not necessarily represent those of Advisor Perspectives.

Sometimes the calendar of news and events makes it easy to predict what will grab our attention in the week ahead. In the last few weeks leading up to the Fed tapering announcement, I highlighted the following:

|

I certainly don't always get it right, but it has been a pretty good run.

The accident of the calendar, mid-week holidays for two consecutive weeks, has created an extended vacation for many market participants. There is little earnings data or important reports, but plenty of football.

The field is open for pundit prognostication!

The predictions cover a wide range, including one featured columnist who sees a 90% chance of a market crash. There is another series on how to prepare for a total collapse, including a link to a survivalist "grab-and-go" bag. I am not including it here, since I clicked on it myself and it now pops up on every page I visit! (Amazon is sold out, at the moment…. Hmm).

How should you navigate the varying forecasts?

- Consider the track record. Anyone can improve, but sometimes it requires accepting new data. You can start with my featured"hot and not" listfor last year. There are some sources that just do not understand earnings, the economy, and the Fed. It is past time to tune them out.

- Try to find balance.Seeking Alphais once again drawing upon a range of sources to help individual investors. I always find this to be a balanced and helpful source and I hope to contribute again this year.

- Demand data, not examples. Do we really care how many times a big market year was followed by another, going back to the Taft Administration? These are anecdotes disguised as data.

- Look for some reasoning based on economic fundamentals and data, not just vague opinions. In particular, ask if the analysis fits where we are in the business cycle.

To start your thinking,Andrew Thrasher suggeststhat we are just entering Stage 4.

I have a little more to suggest in the conclusion. First, let us do our regular update of the last two week's news and data.

Background on "Weighing the Week Ahead"

There are many good lists of upcoming events. One source I regularly follow is theweekly calendar from Investing.com. For best results you need to select the date range from the calendar displayed on the site. You will be rewarded with a comprehensive list of data and events from all over the world. It takes a little practice, but it is worth it.

In contrast, I highlight a smaller group of events, including some you have not seen elsewhere. My theme is an expert guess about what we will be watching on TV and reading in the mainstream media. It is a focus on what I think is important for my trading and client portfolios. Each week I consider the upcoming calendar and the current market, predicting the main theme we should expect. This step is an important part of my trading preparation and planning. It takes more hours than you can imagine.

My record is pretty good. If you review the list of titles it looks like a history of market concerns. Wrong! The thing to note is that I highlighted each topic the week before it grabbed the attention. I find it useful to reflect on the key theme for the week ahead, and I hope you will as well.

This is unlike my other articles at "A Dash" where I develop a focused, logical argument with supporting data on a single theme. Here I am simply sharing my conclusions. Sometimes these are topics that I have already written about, and others are on my agenda. I am putting the news in context.

Readers often disagree with my conclusions. Do not be bashful. Join in and comment about what we should expect in the days ahead. This weekly piece emphasizes my opinions about what is really important and how to put the news in context. I have had great success with my approach, but feel free to disagree. That is what makes a market!

Last Week's Data

Each week I break down events into good and bad. Often there is "ugly" and on rare occasion something really good. My working definition of "good" has two components:

- The news is market-friendly. Our personal policy preferences are not relevant for this test. And especially -- no politics.

- It is better than expectations.

The Good

Most of the recent news continues to be good.

What is fascinating is, the q4 '13 earnings warnings seem pretty dire, as CNBC has detailed, but the expected q4 '13 earnings growth rate for the SP 500 as a whole, is now projected to be 7.6% as of this week's "This Week in Earnings" published weekly by Thomson Reuters, which is the HIGHEST rate of expected earnings growth to start a quarter since q1 '12. The fact is q4 '13 will be quite robust when companies begin reporting in 2 weeks.

Our estimate for q3 '13 earnings growth of 7% – 8% was right on, and we now expect the 4th quarter of 2013 to be plus 10% by the time the 4th quarter is fully reported by mid-March '14.

- LA port traffic shows solid growth. (ViaCalculated Risk).

- Durable goods orders surprised on the upside. (ViaSteven Hansen).

- US oil production is surging – good news on the surface.James Hamilton explainswhy this will not necessarily translate into lower prices. Essentially, it is offsetting prior tight supplies and there is more demand from emerging markets.

- Q3 GDP was revised higher, to an annual rate of 4.1%. The biggest factor was increased consumer spending. Inventories still constitute a big component, whether by accident or design… a big question. Most analysts are now upping their estimates for Q4. (See analysis atCalculated Risk,Doug Short and Steven Hansen at GEI, andEd Yardenion inventories.)

- Initial jobless claims dropped. I am registering this as "good" but it is a complex and noisy story.Doug Short's fine analysis and chartshelp to clarify a complex story. See comparisons that help you navigate the seasonal adjustments and other noise. Meanwhile, here is a key chart:

The Bad

There has not been much bad news over the last two weeks. Feel free to suggest items in the comments

- Investment sentiment remains very bullish, generally viewed as a contrarian market indicator.Bespoke analyzes the AAII series, where bulls are over 50% for the first time since January.

- The Budget Deal may be overrated says Stan Collender in his5 myths story. The myths include some conclusions that I have featured here, so readers should take a look at what this former staffer and current consultant has to say. Over the last two years I have been more accurate than he has, but I always read his work with respect.

- High frequency indicators are still positive, but softer, according to New Deal Democrat. NDD's weekly commentary hasmoved to XE.combut it still includes a fine summary of important data you might otherwise miss. Some soft spots he cites this week are money supply growth (M2) which is below the desired economic trend and weakness in steel production. I always read the entire post, and so should you.

- Dodd-Frank will be futile according to departing CFTC Commissioner Bart Chilton. He describes Wall Street's four-pronged strategy, the D.C. Quadra-Kill. (Defeat the bill, limit funding, negotiate on regulations, and litigate). William D. Cohan at Bloomberg has agreat story.

- Personal income growth has been disappointing. Steven Hansen has a good analysis, featuring this chart:

The Ugly

Holiday shopping SNAFU's. We still do not have the final verdict on the brick-and-mortar shopping season, but we know it wasaffected by calendar compressionand cold weather. The online experience was disappointing for many, as last-minute purchasesdid not arrive as promised. We still do not know the economic effect on retailers, who may have to issue some refunds. Or else!So saysSen. Richard Blumenthal.

Another disturbing retail story is the hacking of Target's credit card data. The immediate reaction was to limit some debit card transactions right during the shopping season. Target claims that the hackers cannot break the "strong encryption" of the pin data, but many are not taking any chances.Blumenthal, former Connecticut Attorney General, is weighing in on this issue as well, offering Congressional cooperation with the FTC.

Silver Bullet

I occasionally give the Silver Bullet award to someone who takes up an unpopular or thankless cause, doing the real work to demonstrate the facts. Think of The Lone Ranger.

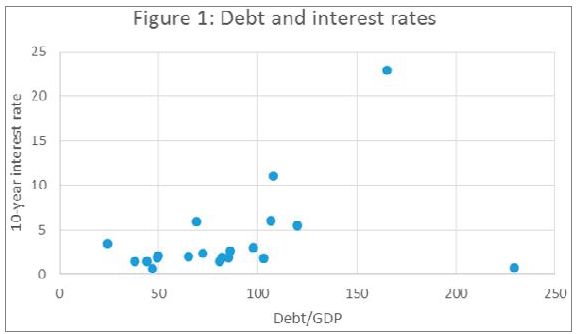

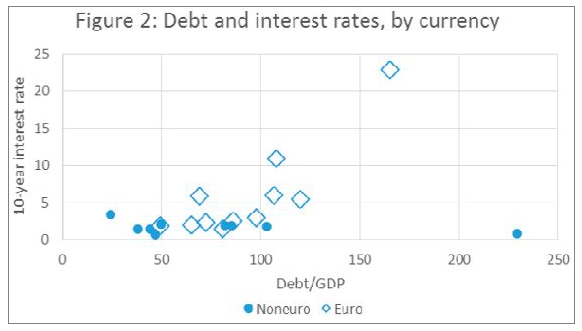

This week's award goes toPaul Krugman and John Lounsbury. While most of us are enjoying the holidays, John is reading Krugman papers from six weeks ago! I know that many readers just tune out anything from Krugman, but this is poor practice for investors. One of the key stories of the year has been the austerity debate and the flawed work of Rogoff and Reinhart – still continually cited by those who think you are uninformed. A key question is whether there is a debt "trigger point" that causes a decline in economic growth. Once again, I care as an investor, not as a voter – despite the politically charge that has been applied to the issue. So here are the facts in two charts.

The first shows the relationship with Japan as an outlier.

The second shows the members of the EU with a different marker.

See John's postfor the full explanation about why it helps to have your own currency.

The Indicator Snapshot

It is important to keep the current news in perspective. I am always searching for the best indicators for our weekly snapshot. I make changes when the evidence warrants. At the moment, my weekly snapshot includes these important summary indicators:

- For financial risk, the St. Louis Financial Stress Index.

- An updated analysis of recession probability from key sources.

- For market trends, the key measures from our "Felix" ETF model.

Financial Risk

The SLFSI reports with a one-week lag. This means that the reported values do not include last week's market action. The SLFSI has recently edged a bit higher, reflecting increased market volatility. It remains at historically low levels, well out of the trigger range of my pre-determined risk alarm. This is an excellent tool for managing risk objectively, and it has suggested the need for more caution. Before implementing this indicator our team did extensive research, discovering a "warning range" that deserves respect. Weidentified a readingof 1.1 or higher as a place to consider reducing positions.

The SLFSI is not a market-timing tool, since it does not attempt to predict how people will interpret events. It uses data, mostly from credit markets, to reach an objective risk assessment. The biggest profits come from going all-in when risk is high on this indicator, but so do the biggest losses.

Recession Odds

In 2014 I will have a new format for this section. It is important, but the changes occur slowly and require more highlights. Suggestions are welcome.

I feature the C-Score, a weekly interpretation of the best recession indicator I found,Bob Dieli's "aggregate spread." I have now added aseries of videos, where Dr. Dieli explains the rationale for his indicator and how it applied in each recession since the 50's. I have organized this so that you can pick a particular recession and see the discussion for that case. Those who are skeptics about the method should start by reviewing the video for that recession. Anyone who spends some time with this will learn a great deal about the history of recessions from a veteran observer.

I also feature RecessionAlert, which combines a variety of different methods, including the ECRI, in developing a Super Index. They offer afree sample report.Anyone following them over the last year would have had useful and profitable guidance on the economy. RecessionAlert has developed a comprehensive package of economic forecasting and market indicators. Theirmost recent reportprovides a market-timing update for those considering whether to "buy the dips."

Georg Vrba's four-inputrecession indicator is also benign."Based on the historic patterns of the unemployment rate indicators prior to recessions one can reasonably conclude that the U.S. economy is not likely to go into recession anytime soon." Georg has other excellent indicators for stocks, bonds, and precious metals atiMarketSignals. His most recent update revisits Albert Edwards's year-old prediction that the Ultimate Death Cross was imminent. Georg refuted the claim at the time, andnow takes a more complete look.

Unfortunately, and despite the inaccuracy of their forecast, the mainstream media features the ECRI. Doug Short hasexcellent continuing coverageof the ECRI recession prediction, now more than two years old. Doug updates all of the official indicators used by the NBER and also has a helpful list of articles about recession forecasting. Doug also continues to refresh thebest chart updateof the major indicators used by the NBER in recession dating. The ECRI approach has been so misleading and so costly for investors, that I will soon drop it from the update. The other methods we follow have proved to be far superior.

Readers should review myRecession Resource Page, which explains many of the concepts people get wrong.

Here is our overall summary of the important indicators.

Our "Felix" model is the basis for our "official" vote in the weeklyTicker Sense Blogger Sentiment Poll. We have a long public record for these positions. Over the last three months Felix has ranged over the full spectrum – twice! The market has been moving back and forth around important technical levels, driven mostly by news. The current values are now neutral. There are still many positive sectors, but few with real strength.

Felix does not react to news events, and certainly does not anticipate effects from the headlines. This is usually a sound idea, helping the trading program to stay on the right side of major market moves. Abrupt changes in market direction will send sectors to the penalty box. The Ticker Sense poll asks for a one-month forecast. Felix has a three-week horizon, which is pretty close. We run the model daily, and adjust our outlook as needed.

The penalty box percentage has increased dramatically, meaning that we have less confidence in the overall ratings.

[For more on the penalty box seethis article. For more on the system ratings, you can write to etf at newarc dot com for our free report package or to be added to the (free) weekly ETF email list. You can also write personally to me with questions or comments, and I'll do my best to answer.]

The Week Ahead

There is a little data –some important – in the holiday-shortened week.

The "A List" includes the following:

- ISM manufacturing (Th). Important concurrent economic indicator.

- Initial jobless claims (Th). Best fresh data on employment.

- Consumer confidence (T). Good read on both employment and consumer spending.

- Auto sales (F). Growing attention as recent increases fuel economic growth.

The "B List" includes:

- Pending home sales (M). Housing remains crucial for the 2014 economic outlook.

- Case-Shiller home prices (T). Slightly lagging data, but widely followed.

- Chicago PMI (T). Probably the best regional series for predicting the national number, out two days later.

The American Economic Association annual meeting will feature presentations by several Fed presidents and Chairman Bernanke. Some of these will occur on Friday and others on Saturday. There may also be advance copies available. With continuing quiet trading, some will try to squeeze out some fresh Fed news.

How to Use the Weekly Data Updates

In the WTWA series I try to share what I am thinking as I prepare for the coming week. I write each post as if I were speaking directly to one of my clients. Each client is different, so I have five different programs ranging from very conservative bond ladders to very aggressive trading programs. It is not a "one size fits all" approach.

To get the maximum benefit from my updates you need to have a self-assessment of your objectives. Are you most interested in preserving wealth? Or like most of us, do you still need to create wealth? How much risk is right for your temperament and circumstances?

My weekly insights often suggest a different course of action depending upon your objectives and time frames. They also accurately describe what I am doing in the programs I manage.

Insight for Traders

Felix has remained in neutral, although we are still mostly invested in the top two sectors. Felix's ratings have been in a fairly narrow range for several months. The rapid news-driven shifts are not the ideal conditions for Felix's three-week horizon. This week we see somewhat higher ratings, and many sectors in the penalty box. There are still two attractive sectors, and we may add to positions in the week ahead.

Insight for Investors

I review the themes here each week and refresh when needed. For investors, as we would expect, the key ideas may stay on the list longer than the updates for traders. Each week I try to highlight something special for the long-term investor.

I try to refresh the concepts and ideas each week, emphasizing the best themes from my reading. My overall recommendations do not change as rapidly – nor should they. I am considering some format changes for next year, helping to highlight the specific new recommendations.

One of my major themes for the year has been the "great rotation" from bonds to stocks. This has three aspects:

- Bond yields are so low;

- Bond prices have fallen, leading to absolute losses for conservative investors;

- Stocks have surged.

This should not have been a surprise for those paying attention. It is just getting started. As he often does, Josh Brown captures the main theme inthis post about the rotation. He is quoting the chief market strategist at ConvergEx Group:

In short, the trade in 2013 has been out of munis and gold, and into the world's stock markets. Look a little deeper, and the headline becomes "Mutual fund buyers are finally back". Just 2 years ago the U.S. mutual fund investors were net sellers of financial assets, to the tune of ($27.5 billion). The year 2012 saw them tiptoe back, with positive flows of $117.6 billion, but still redeeming stocks for bonds. This year inflows are $164 billion with two weeks or so remaining and substantially all of that into stocks.

This rotation is just getting started. Our own themes are the same, but I will also do a "year ahead" preview pretty soon.

Here is a summary of our own current recommendations for the individual investor.

- Headlines. The challenge for investors is to distinguish between the major trends and the short-term uncertainty. The main themes are not related to headlines news, even though sentiment may drive market fluctuations. Do not be seduced by the idea that you can time the market, calling every 10% correction. Many claim this ability, but few have a documented record to prove it. Most who claim past success are using a back-tested model. Please seeThe Seduction of Market Timing.

- Risk Management. It is far better to manage your risk, specifically considering therole of bonds and the risk of bond mutual funds. As I emphasized, " You need to choose the right level of risk!" Right now, it is the most important question for investors. There is plenty of "headline risk" that may not really translate into lower stock prices. Instead of reacting to news, the long-term investor should emphasize broad themes.

- Bond Funds are Risky. Investors have been surprised at the losses, which will continue as the long end of the interest rate curve moves higher. You need to have the right mix of stocks to benefit from a rising rate environment.

- Stepping in gradually. If you are completely out of the market, you are not alone. Consider buying dividend stocks and selling calls against them. This strategy has been working great both for our clients and for many readers. (Thanks for the email responses!) This will work in a sideways market. You can also buy some stock in the sectors with the best P/E ratios.

And finally, we have collected some of our recent recommendations in anew investor resource page-- a starting point for the long-term investor. (Comments and suggestions welcome. I am trying to be helpful and I love feedback).

Final Thought

It would be silly to predict the market in the final week of the year, with tax trading and window dressing in the first two days, and "new" positions in the last two.

My general sense is that many are still looking for an entry point. I was impressed (negatively) bya Barron's columnistthis week. After noting the 2-1 odds that stocks would be higher (which I have already suggested that you ignore) he emphasizes the 33% chance of a decline. OK.

Then he dredges up a list of warmed-over worries that might resurface. OK.

This is all true, and might happen. But get the final stanza:

Still, the biggest risk to the U.S. could be the gift that has topped our wish list for years: a much stronger economy, which could ignite inflation and force the Fed to hike interest rates sooner than expected. It's getting hot out there: Sales of durable goods and new homes have been much stronger than forecast.

While the Fed's favorite inflation gauge, the PCE deflator, remains stuck near 1%, the GDP price index rose at an annual rate of 2% during the third quarter, suggesting inflation might be running higher than policy makers expect, says Michael Shaoul, CEO of Marketfield Asset Management.

Should that prove the case, the Fed's plan to gently reduce its bond-buying, which will start next month with a $10 billion taper, would be thrown into disarray. The pace of the taper would have to increase, and an interest-rate hike could come quickly. "Everyone wakes up, the Fed is miles behind the curve, and everything needs to be torn up," Shaoul says. "That's when you go through a 1994- or 1987-style adjustment."

In other words, on the one hand there are a lot of economic risks. If these are avoided and things get better, the Fed will bring it to a swift end.

I strongly recommend that investors ignore pundits whose analysis has no provision for "buy."

Originally posted at Jeff's blog:A Dash of Insight

© New Arc Investments