I’ve often said that trying to stop a bull market has risks. It was certainly precarious to think this year’s run would end anytime soon.

By December 27, the S&P 500 Index climbed an astounding 31.86 percent in 2013.

Will stocks continue to climb in 2014? Odds are “very good,” finds BCA Research. According to historical data going back to 1870, there were 30 times when annual returns in domestic stocks climbed more than 25 percent. Of these, 23 experienced an additional increase, resulting in a mean of 12 percent, says BCA.

Thinking back to January 2013, investors had a very different frame of mind. While we recently talked about the year’s biggest stories in U.S. energy and gold, today, we recap our popular commentaries focused on the domestic market.

Dow to 14,000 … And Beyond? (February 5, 2013)

After January saw the best month in two decades for U.S. stocks, I wrote how sentiment was slowly improving as many uncertainties had been removed from the market. I gave three reasons to stay positive on equities:

- U.S. businesses and households were deleveraging

- New home sales were expected to increase

- Inflation was low

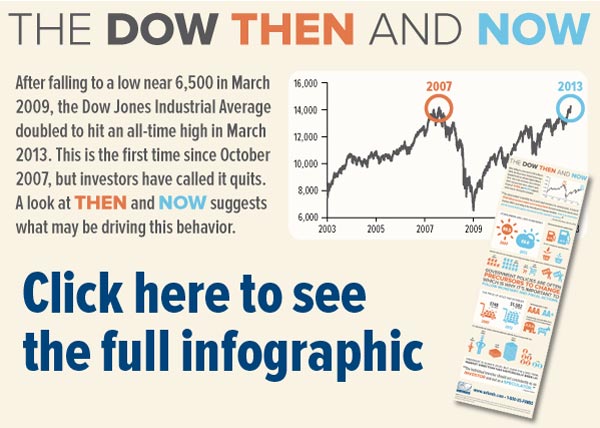

Dow, Now and Then (March 12, 2013)

It wasn’t long before the Dow was hitting highs, yet with elevated unemployment, dysfunction in Washington and ongoing negative news about the U.S. economy, we noted that investors weren’t celebrating. There were plenty of reasons for that: In an infographic that was retweeted by Jim Cramer, we visually compared the Dow, then and now.

Don’t Sell in May: Here are Reasons to Extend Your Stay (May 6, 2013)

By the end of April, we noted that formerly weaker areas of the market were gaining strength. From April 24 through May 3, health care, consumer staples, utilities and telecommunications sectors lagged, while energy, industrial and materials stocks were nearly the best performing areas of the market.

This turned out to be a significant inflection point in the market, with cyclical stocks gaining strength over the next several months. Read the article here.

click to enlarge

Don’t Miss This Golden Cross in Resources (November 4, 2013)

While investors were focused on the strengthening U.S. market, we noted improving indicators in other areas, including resources, Europe, and emerging markets. Notably, the global synchronized easing continued to take place along with improving purchasing managers index (PMI) number in many countries. Historically these factors bode well for commodities and commodity stocks. Read how you can “count on” PMIs here.

While many of these areas of the market were not as widely popular as U.S. stocks, we believed investors could benefit from being contrarian. Read the article now.

|

|

As we wrap up the year, the benchmark 10-year Treasury note’s yield rose above 3 percent, touching the highest level in more than two years. An increase in bond yields can be both good and bad. According to ISI, a bad increase in bond yields is related to tapering concerns. A good increase in bond yields is related to the economy strengthening. “The two are intertwined, so it’s difficult to know which is dominating. However, judging by the S&P, a Good Increase currently has the upper hand,” says ISI. Our focus on global PMI numbers as early indicators of economic strengthening relates to this view.

The “good increase” in Treasury yields means a return to a positive real interest rate environment which is, historically, a headwind for gold prices.

What do you think will be the biggest stories in the new year? We’d like to know your predictions, questions and resolutions for 2014. Email us at [email protected].

We wish you a joyous, healthy and prosperous New Year!

click to enlarge

Index Summary

- Major market indices finished higher this week. The Dow Jones Industrial Average rose 1.59 percent. The S&P 500 Stock Index gained 1.27 percent, while the Nasdaq Composite advanced 1.26 percent. The Russell 2000 small capitalization index moved ahead by 1.28 percent this week.

- The Hang Seng Composite rose 1.93 percent; Taiwan gained 1.50 percent while the KOSPI advanced 0.95 percent. The 10-year Treasury bond yield rose 11 basis points this week to 3.00 percent.

|

|

||

|

|

|

|

|

|

||

![[thumb]](/images/content_image/data/95/955a2fac7b18c99bd7f0d7ee0d2eac35.jpg)

![[thumb]](/images/content_image/data/f7/f78044f243b65d6575f78d904fffec0c.jpg)

![[thumb]](/images/content_image/data/92/9281126c4549d804b88a96fb1119a7be.jpg)

Domestic Equity Market

The S&P 500 Index experienced a broad based rally during this holiday shortened week. Cyclicals tended to outperform as investors confidence continues to build for continued economic improvement in 2014.

click to enlarge

Strengths

- The materials sector was the best performer this week, led by Alcoa, Cliffs Natural Resources and U.S. Steel, which all rose by more than 7 percent. News flow was generally quiet; this appeared to be more of a sector rotation story into cyclical areas of the economy.

- The telecom services sector was also strong this week as both AT&T and Verizon rose by more than 2 percent. There was continued speculation that Sprint would merge with T-Mobile, which also attracted investors to this sector.

- Cliffs Natural Resources was the best performer in the S&P 500 this week, rising 9.58 percent. While there was little company specific news, the stock had been heavily shorted and with expectations of better growth ahead it may have been short covering that led to this week’s move.

Weaknesses

- The utilities sector was the worst performer this week as Treasury yields continued to climb. The 10-year Treasury breached the psychologically important 3 percent level on Friday.

- Airlines and internet retailers underperformed this week. Delta was down 3 percent on Friday after a computer glitch allowed customers to purchase cross country tickets at a fraction of their value. Internet retailers and internet companies generally came under pressure Friday as shipping delays that prevented packages from arriving in time for Christmas left many companies in a public relations bind.

- Whole Foods Market was the worst performer in the S&P 500 this week, falling 4.37 percent. Food retailers underperformed this week without much news flow. The consumer staples sector lagged this week as a rotation into cyclicals continues.

Opportunities

- The current macro environment remains positive as economic data remains robust enough to give investors confidence in an economic recovery but not too strong as to force the Federal Reserve to aggressively change course in the near term.

- Money flows are likely to find their way into domestic U.S. equities and out of bonds and emerging markets.

- The improving economic situation could possibly drive equity prices well into 2014.

Threats

- A market consolidation could occur in the near term after such strong performance.

- Higher interest rates are a threat for the whole economy. The Fed must walk a fine line and the potential for policy error is potentially large.

- A lot of potentially good news is priced into the market and the economy will need to deliver to maintain the positive momentum in the market.

The Economy and Bond Market

Treasury bond yields moved higher this week, reaching the psychologically important 3 percent yield last seen in September. Yields appear to be moving higher in response to better economic data and a positive outlook for 2014. Stocks and bond yields have both been moving higher for the past two months as they are both responding to an improving economic outlook.

click to enlarge

Strengths

- Durable goods orders rose 3.5 percent in November which was well ahead of expectations and reinforces the strengthening economy story.

- Initial jobless claims fell back below the four-week average after spiking the prior two weeks.

- Canadian GDP rose 0.3 percent in October and 2.7 percent year-over-year.

Weaknesses

- Mortgage applications fell 6.3 percent last week, hitting a 13-year low as refinancing demand continues to slide with higher interest rates.

- Retail sales during the holiday selling season appear to have relied on heavy discounting to move goods. This is a counter point to the improving economy story.

- China’s interbank lending rate spiked as year end funding needs created a cash crunch for some financial institutions. This has become an almost regular occurrence and raises questions around the health of some of China’s financial institutions.

Opportunities

- Despite recent conflicting commentary, the Fed continues to remain committed to an overall accommodative policy and is unlikely to raise interest rates in 2014.

- Key global central bankers remain in easing mode such as the European Central Bank, Bank of England and the Bank of Japan.

- There are many moving parts to the taper decision and while the Fed began the process it is very possible that tapering could be delayed if economic data slows.

Threats

- Inflation in some corners of the globe is getting the attention of policy makers and may be an early indicator for the rest of the world.

- Trade and/or currency “wars” cannot be ruled out which may cause unintended consequences and volatility in the financial markets.

- The recent bond market sell off may be a “shot across the bow” as the markets reassess the changing macro dynamics.

Gold Market

For the week, spot gold closed at $1,212.93, up $9.63 per ounce, or 0.80 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, rose 4.21 percent. The U.S. Trade-Weighted Dollar Index lost 0.27 percent for the week.

Strengths

- Platinum futures jumped the most in 10 weeks on speculation that a global economic rebound will boost demand for the metal used for pollution control devices in cars. Platinum reached a two-week high on Friday in the most active trading of the session. A recent Bloomberg survey shows the price of the precious metal is expected to rally to $1,650 an ounce in 2014 as consumption surpasses output. Demand exceeded supply this year by the most since 1999 and the continuation of the synchronized global economic recovery will likely lead to an even greater shortage in 2014.

- India's Commerce Ministry has asked to ease the restrictions on the import of gold, imposed by the Reserve Bank of India (RBI), in an effort to control the rising current account deficit. In a letter to Economic Affairs Secretary, Commerce Secretary S. R. Rao asked him to ``look into the matter'' and issue necessary instructions to the RBI for the removal of the anomaly. The move would relieve jewelers who have been reeling from the government induced gold import curbs. So far, the government has responded with a bid to relax some of the conditions currently imposed on the import of gold ore by refiners, with the aim of kick starting India’s waning gold refineries, which have been operating at only 25 percent of installed capacity. Official sources have argued that the nation’s current account deficit has compressed significantly since the introduction of the import curbs, and this can be read as a first step in reduci ng the import duty on gold in a calibrated manner.

- The German Bundesbank announced it has transferred 37 tons of gold back from New York and Paris to its Frankfurt vaults. Bundesbank President Jens Weidmann said the transfer was prompted by new a Bundesbank storage concept to hold gold in Frankfurt, and not because of concerns over its availability. However, Germany’s Federal court concluded in 2011 that the nation’s gold holdings overseas weren’t regularly checked, which prompted the initiation of plans to bring back a total 700 tons previously in deposit with the Fed and the Banque de France. As a Zero Hedge article points out, procuring physical gold seems to be a rather problematic and time-consuming process, as the Bundesbank is learning. It was almost exactly one year ago in mid-January, when the German central bank, in a shocking development expressing the bank's lack of trust in its central banking peers, announced that it would proceed with the repatriati on of 700 tons of gold held by its peers, only to learn it would take 7 years, or until 2020, to repatriate the full amount.

Weaknesses

- Gold is set to post its biggest annual loss in more than three decades as rallying U.S. equities and optimism about a synchronized global economic recovery lowered its safe haven appeal. The near 30 percent slump in 2013 ends a 12-year rally prompted by rock bottom interest rates and rapidly expanding central banks’ balance sheets. The mood remains bearish among generalists who expect prices to drop further next year. Several brokerages such as Goldman Sachs, BNP Paribas and Societe General have gold price targets below $1,150 in 2014. Physical demand, which climbed to peak levels this year, has shown it can provide support on the downside, but it has failed to drive prices higher. Silver is down just under 35 percent for the year, its worst annual performance since at least 1981.

- Jaguar Mining Inc., the operator of two Brazilian gold mines, filed for bankruptcy protection in Canada as it tries to restructure its debt. Jaguar started proceedings under the Companies’ Creditors Arrangement Act in Ontario, with the aim to reduce total pro forma debt via a recapitalization; reduce projected annual cash interest payments; and invest approximately $50 million of new equity raised through current holders of the company's convertible notes.

- On December 23rd, Detour Gold Corp. announced an unplanned mill shutdown. According to the announcement, the processing plant was shut down on December 17 due to mechanical issues with the pre-leach thickener system. Further inspection found structural damage to the torque cage. Management estimates that the processing plant will restart prior to year end. Credit Suisse analysts believe the unplanned shutdown will result in a fourth quarter gold production miss, which will roll over and cause the company to miss its already lowered full year 2013 production guidance of 240-260 thousand ounces. In addition, Credit Suisse warns to remain cautious around consistency of the mining rate to keep pace with the mill, grade reconciliation and recovery rates, and longer term, the economic viability of the low grade tail of reserves.

Opportunities

- The metals analysts at J.P. Morgan think it is easy to look at the cost of new mines and conclude that current prices are unsustainable. In addition, JPM analysts assert that on Wall Street the question of future inflation is a when, and not if, proposition. With central banks around the world still printing money at a furious pace, a debasement of the value of their currencies is forthcoming. As a result, the J.P. Morgan team thinks now is the time to look hard at gold and silver as hedges, especially given the golden opportunity created by the recent downturn in prices. The motivation is that contrarian investing has paid off big for patient investors, and it can pay off even bigger when the whole world is negative on the asset class, such as gold at present time. Just a few short years ago major homebuilders traded in the single digits, while banks and brokerage firms got clobbered in 2008. The recovery in those sectors has paid off handsomely. Wit h gold, once inflation finally kicks in after years of currency printing, the patient gold investor may again have his day in the sun.

- Capital Economics argues the precious metal could come back into favor in 2014. “The consensus is that the price of gold will grind lower in 2014, at best, as the support from loose U.S. monetary policy gradually weakens,” said Julian Jessop, head of commodities research at the firm. “In contrast, with investor sentiment already so heavily negative, our view is that the risks for the coming year are firmly skewed to the upside.” According to Jessop, the latter half of 2013 suggests the worst of the slump may be over. Indeed, during this period, gold prices staged a partial recovery, rising to $1,400 before dropping back to current levels around $1,200. Jessop added that that next year, a re-emergence of eurozone instability, and the Fed's continued asset purchase program, could work to boost gold prices. Although the Fed has announced a small taper, it will still be pumping large amounts of stimulus into the e conomy through most, if not all, of 2014. “We are happy to reiterate our view that the price of gold will revisit $1,400, at least, in 2014, and probably go higher,” Jessop concluded.

click to enlarge

- Metal and crop prices are poised to rebound in 2014 as accelerating economic growth boosts demand, according to a Bloomberg story. Average annual prices for 15 of 23 non-energy commodities from aluminum to sugar will be higher than now, according to estimates from as many as 26 analysts compiled by Bloomberg. Corn, silver and gold dropped the most in 2013. “It’s a good time to come into commodities,” said James Paulsen, the Minneapolis-based chief investment strategist at Wells Capital Management, which oversees about $340 billion of assets. “This is the first time in the recovery that we’ve had simultaneous positive and accelerating growth in the U.S., Europe, Japan and the emerging world all at the same time. Economic growth may not be enough to end the slump. Silver, after posting the biggest loss of any precious metal, will rise as much as 28 percent in 2014 to $25 an ounce on spot markets, according to the median of 40 es timates. Gold will gain 20 percent to $1,450, based on 59 estimates. On the bearish side, Jeffrey Currie, Goldman’s head of commodities research in New York said there will be “significant” declines through next year for iron ore, gold, soybeans and copper. He added that gold will slide to $1,110 an ounce in 12 months.

Threats

- Barrick Gold Corp. agreed to sell its Plutonic mine in Western Australia to Northern Star Resources for A$25 million as it tries to cut costs and focus on its most profitable operations. The total purchase consideration appears to be less than half of the lower range estimated by a Seeking Alpha contributor drawing from recent comparable transactions. According to the same report, the Plutonic mine has been in operation since 1990 and has yielded 5.24 million ounces in its mine life so far. The mine has consistently produced around 100,000 ounces per year and has a history of reliable resource to reserve conversion. Similarly, Rio Tinto Group, the world’s second- largest mining company, is considering selling its stake in the massive Alaskan Pebble copper-gold project as it cuts costs across its businesses. In our view, these announcements continue to demonstrate the atrocious market timing performance of major producers who are only compelled to apply financial restraint and divest assets at rock bottom valuations, while increasing capital spending and acquisitions near market peaks, all to the detriment of shareholders.

- According to David Rosenberg of Gluskin Sheff, wage inflation is a key source of upside risks to growth in 2014, and that is not on the radar screen. The recent Beige Book had abundant anecdotal evidence highlighting job shortages on high-skill trades. Rosenberg estimates that out of the 115 million people currently employed in the private sector, roughly 40 million of them are going to be reaping the benefits of a higher stipend. With the Fed still consumed with deflation fears, and job firings already 20 percent below 2007 levels, Rosenberg argues that inflation is likely to surprise to the upside. In such an environment, gold is likely to regain strength on the basis of its hedging qualities. In addition, the areas of consumer spending that showed the greatest positive sensitivity to periods of rising wage growth include jewelry and electronics; sectors that may provide incremental demand for both gold and silver.

- A Financial Times article this week speaks to the crisis of confidence in the mining sector. According to the report, the number of new mining listings in Canada, where roughly 70 percent of all mining equity finance is raised, plunged fuelled by a steep decline in metal prices. Up until the end of November, 62 companies had listed on the Toronto Stock Exchange or the TSX venture exchange, compared with 129 by the same point in 2012 and more than 200 in both 2009 and 2010. The amount of equity raised in Toronto has also fallen from $10.3 billion in the whole of 2012 to just $6.5 billion by the end of November. Almost half of this year’s total to date came in November when Barrick Gold, raised $3.1 billion of fresh equity.

Energy and Natural Resources Market

Strengths

- Crude oil (West Texas Intermediate) finished the weak higher as well as implied demand in the U.S. remains strong and drove prices near two-month highs of $100 per barrel.

- The CRB Raw Industrials Index broke out to an eight-month high as global economic indicators continue to point towards expansion.

- Metals prices have been strong in December with copper prices gaining three percent this week to $3.44 per pound and hit an eight-month high price. Zinc prices also rallied for a fourth straight week and have broken out to nine-month highs.

Weaknesses

- After closing at a multiyear high price earlier in the week, natural gas futures in New York eased about one percent this week as expectations of milder weather weighed on prices.

- The U.S. Farmland Price Index compiled by Creighton University weakened to 47.0 this month, indicating the first contraction since December 2009 amid recent concerns of asset bubbles forming in the farming sector following a period of heavy investment in land and equipment. "This is the first time in four years that the farmland-price index has moved below growth neutral," Creighton Economist Ernie Goss said. A reading above 50 indicated expansion while below 50 marks a contraction. The index stood at 54.3 in November and compares with 82.5 in December 2012. The apparent decline in farmland prices reflects a similar decline in confidence amongst U.S. farmers, who until recently enjoyed a boom period, bolstered by record crop prices and a surge in exports.

Opportunities

- The United States’ average daily oil production is on track to surge by one million barrels per day this year, the biggest one-year jump in the nation’s history, according to federal data. The country has pumped an average of 7.5 million barrels of crude per day in 2013, up from 6.5 million barrels per day in 2012. That breaks last year’s record, when oil production jumped by 837,000 barrels per day between 2011 and 2012. The U.S. Energy Information Administration projects that oil production will jump by another one million barrels per day in 2014, largely buoyed by drilling activity in Texas’ Eagle Ford Shale and Permian Basin regions, as well as North Dakota’s Bakken Shale. The Gulf of Mexico also is seeing a boost, with oil production expected to grow to 1.4 million barrels per day in 2014, up by 100,000 barrels. The data is evidence of the astonishingly rapid turnaround in the nation’s energ y story. Oil production declined in 29 of the 40 years between 1971 and 2011. In total, oil production fell by about 40 percent during that time, from 9.5 million barrels per day in 1971 to 5.6 million barrels per day in 2011. While the U.S. oil boom has sparked conversation of energy independence, Americans consume about 18 million barrels of liquid fuels per day, far more than is produced domestically. Still, the production surge has caused oil imports to drop considerably. The nation shipped in an average of 7.9 million barrels per day of crude in September, the most recent period for which import data is available. That’s a significant drop from the peak in 2005, when the nation imported an average of 10.1 million barrels per day.

- China’s fixed-asset investment in road and waterway infrastructure is estimated to hit 1.53 trillion yuan in 2013, an increase of 5.56 percent from the previous year, said Yang Chuantong, Minister of Transport, at a conference on Friday. According to the minister, China is expected to complete construction of 8,260 kilometers of new expressways, and rebuild 339 kilometers of expressways and 28,600 kilometers of national and provincial trunk highways in 2013. The country will also rebuild 210,000 kilometers of rural roads, complete construction of 110 berths of 10,000 deadweight tonnage and bigger tonnage, and add and renovate 289 kilometers of fairways in the year.

Threat

- Indonesia's production of metal ores is expected to fall "drastically" due to a ban on unprocessed mineral exports set to begin in January, a government official said, as there is insufficient smelting capacity to absorb the volumes of base metal ores the country produces. From January 12, mining companies must process their ore before shipping it overseas under a measure which aims to boost the value of exports from Indonesia, the world's top exporter of nickel ore, thermal coal and refined tin. "Ore production will fall drastically next year due to this ore export ban," Sukhyar, the country's newly appointed director general of coal and minerals, told reporters in Jakarta on Friday.

Emerging Markets

Strengths

- The recent PMIs in Europe, where data showed growth in the eurozone’s manufacturing sector was at the highest in 31 months, were a big relief and showed the recovery is back on track. The upturn means that, over the final quarter, businesses saw the strongest growth since the first half of 2011, and have now enjoyed two consecutive quarters of growth. It is not surprising then that Germany's DAX ended this week at an all-time high, while France’s CAC index and Italy’s MIB index closed near 52-week highs. The confirmation of the recovery and subsequent equity market outperformance bode well for emerging Europe stocks as we head into the new year.

click to enlarge

- After the People’s Bank of China open market operation on Tuesday, 7-day Shanghai Interbank Offered Rate (SHIBOR) stabilized at 5.067 percent on Friday, and the Shanghai Composite Index rose 1.4 percent.

- China’s economic growth this year is likely to come in at 7.6 percent, above the government’s 7.5 percent target, a report by the State Council was cited by the official Xinhua News Agency.

- China will issue licenses for mobile virtual networks, which will benefit internet social network and messaging operators.

- China property inventory stands at 11.1 months equivalent of sales, below the seven-year average of 11.5 months. The sector net asset value (NAV) discounts, price to earnings multiple, and price to book ratios are all down one standard deviation, which bodes well for a stock price rebound.

- Guangdong province may cancel administrative intervention on home purchases from next year, though it seems the local government has since backed away a little from this and says it will follow instructions from the central government in Beijing.

- Thailand current account surplus rose to $2.3 billion in November driven by a sharp drop in imports which was down 9.3 percent year-over-year.

- Taiwan kept its benchmark rate unchanged at 1.875 percent for 10-day loans due to low inflation.

- Singapore November inflation ticked up to 2.6 percent as expected.

Weaknesses

- Russia December Manufacturing PMI reading of 48.8 was the lowest in 4 years. Business conditions for manufacturers shows continued deterioration with the index contracting from 49.4 in November. A drop in export demand led to stagnation in new factory orders and revives the manufacturing growth concerns in the BRIC (Brazil, Russia, India, China) nations, according to HSBC. The index has now deteriorated for five out of the past six months.

- Reserve Bank of India chief Rajan announced the central bank had decided to keep rates on hold for a second month, even before the consumer price and retail inflation data for November were released. During the bank’s last meeting, the RBI surprised investors by keeping interest rates on hold despite data showing consumer prices in posted their biggest annual rise on record of 11.24 percent, while wholesale inflation hit a 14-month high.

- Auto makers with Japanese joint ventures may see their stock price retreat temporarily after the Japanese Prime Minister Abe ignited controversy by worshipping at the Yasukuni shrine.

- Private consumption in Thailand fell 2.4 percent on a year-over-year basis and 1.2 percent month-over-month in November. Private investment also dropped 7.87 percent year-over-year and 0.6 percent month-over-month. Manufacturing production fell 10.6 percent year-over-year, due to a high base last year.

- Singapore November industrial production was up 4.0 percent versus the market estimate of 5.3 percent.

- China industrial enterprises above designated size saw profit growth of 9.7 percent year-over-year in November, 5.4 percent lower than in October dragged by declining profits at state-owned enterprises.

- Taiwan November export growth stopped in November, while import growth was a negative 0.5 percent.

Opportunities

- The Bundesbank president and ECB Governing Council member Jens Weidmann said Friday in an interview that the ECB should hike interest rates if inflation risks rise in the eurozone. He pointed out that keeping rates low for an extended period of time could negatively affect eurozone economies' reform policies and added that low inflation pressures don't give a license for arbitrary monetary easing. His view seemed to reinforce the view that the European recovery is well in its tracks and can sustain a rate hike. As a result, the euro rallied, providing for an interesting case in the needed export driven growth economies of Central and Eastern Europe.

- International Monetary Fund (IMF) Managing Director Christine Lagarde said the budget deal reached in Washington and the Federal Reserve’s plan to taper its bond buying should increase confidence about the future. The IMF said it is preparing to bolster the outlook for developed economies for 2014. As a result, all 10 industry groups in the Emerging Markets Index rose on the expectation that external demand from a synchronized expansion in developed markets will drive a recovery in lagging emerging markets.

click to enlarge

- As shown in the chart above, China's demand for civilian helicopters is set to grow. Helicopters are now purchased for land and sea logistics. With vast land and long sea shorelines in China and a growing economy, the ownership of civilian helicopters is deemed to catch up with developed countries.

Threats

- Turkey stocks dropped, as the lira tumbled with foreign investors selling the nation’s debt on concern the political instability will worsen. In addition, European Union Enlargement Commissioner Stefan Fule said he was concerned by “the removal of a large number of police officers from their duties” and urged Turkey to “take all the necessary measures to ensure that allegations of wrongdoing are addressed without discrimination.” The EU warning threatens Turkey’s ambitions of joining the common market once again, following the condemnation by EU officials of Erdogan’s treatment of the protests that engulfed the country last summer.

- Russia’s Gazprom, the world’s biggest natural gas producer, announced its dividend will likely miss analysts estimates by about 25 percent as output stalls. The state-controlled company has failed to restore pre-recession output levels. In addition, the company’s profit margins suffered when Gazprom agreed to retroactive discounts for some European clients. Most recently, with the signature of a pact to normalize relations between Russia and Ukraine, Gazprom will be required to provide gas to Ukraine at subsidized prices, which are likely to add pressure to the already stressed profit margins.

- Continued political uncertainty has further dampened consumption and demand in Thailand. With the recent postponement of the February 2014 election, the market may continue to see short-term volatility. Nevertheless, a declining price/earnings multiple will prepare the market for a rebound.

© US Global Investors