In addition to reducing the risk of a permanent loss of capital, the staying power of a company allows for capital to compound over long periods of time. While the defensive and less cyclical nature of many consumer staples companies indicates an ability to survive, most are able to invest only a portion of earnings at historical rates of return. Under such a scenario, the most shareholder friendly course is to return excess capital to shareholders in the form of dividends or stock buybacks. One company that closely adheres to this principle is Philip Morris International (PMI), the international cigarette manufacturer of brands such as Marlboro and L&M. Since PMI was spun off from its parent, Altria, in 2008, the company has bought back almost a quarter of its then shares outstanding in addition to paying out over 60% of earnings in the form of dividends. The stock price has nearly doubled.

Good Business

The cigarette industry enjoys many characteristics of a good business – high returns on capital, low capital intensity, strong brand loyalty, and unrivaled pricing power. Some might question the staying power of companies in this industry given the long-term declining trend. This broad generalization, however, fails to distinguish between a greater degree of volume deterioration in developed markets and flat to slightly positive trends in many emerging markets. Besides, volume is only one part of the equation. Cigarette manufacturers, including PMI, have taken substantial pricing action for many years, and a vast majority of their growth now comes from pricing. Since 2009, PMI has generated a positive annual pricing variance of $1.8 billion1 . As a percentage of revenue, this pricing action amounts to almost 6%. Yet, the average retail price for a pack of 20 PMI cigarettes is only $5.32 in developed markets and $1.41 in developing markets1. Compared to other consumables that compete for a customer’s wallet, cigarettes remain affordable, allowing room for further price increases.

The staying power of many businesses is stress-tested during extreme events such as a recession, industry consolidation, product obsolescence, shifts in customer preferences, and governmental action. Over the short-term, PMI is not immune to these pressures, but the company has proven to be surprisingly resilient over the long-term. More recently, during the great recession, cigarette industry volumes fell from flat to slightly negative in 2010 before recovering somewhat by 20121.

Finance theory states that the intrinsic value of a business is the sum total of the present value of its future cash flows. Therefore, we like businesses that generate copious amounts of cash while requiring minimal investment. Since its spin-off, PMI has converted almost a third of its revenues to cash flows from operations while utilizing only a tenth of those cash flows for capital expenditures1.

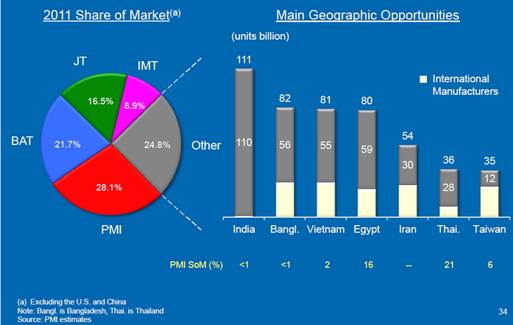

Growth Opportunities

While the staying power of a company does not usually depend on its growth rate, profitable growth of any business improves its ability to withstand challenging times. As value investors, we do not like to pay too much for growth but understand that it is part of the equation and would like to benefit from it, particularly if it comes with little or no incremental investment. Two such growth trends that are working in PMI’s favor include: population growth in emerging markets and a consumer shift towards the premium segment of the market where PMI dominates.

In addition, we believe PMI should gain from geographic expansion and further market penetration in many large markets of the world (see chart2 below). PMI may also benefit modestly from its joint venture with China’s only state-owned cigarette producer.

Another growth opportunity for PMI could arise from curtailment in illicit trade. The excessive nature of government taxes and the relative ease of production and transportation of goods make the cigarette industry a natural target for illicit trade. Such trade consists of selling copies of major brands and diverting products from regimes with lower taxation rates to those with higher rates. Illicit trade comprises almost 10% of global cigarette consumption. A mere 50% reduction could boost PMI’s operating income by $1.7 billion3 or more than 10%.

PMI believes that its biggest growth opportunity lies in the commercialization of E-Cigarettes and describes it as a ‘paradigm shift’. We are, however, generally wary of ‘paradigm shifts’ and always remind ourselves of how Coca Cola came to the brink of disaster with its launch of New Coke a quarter of a century ago. That said, not engaging in this newest segment of the industry is not an option for PMI as it could mean being left out of the race permanently.

Good Management

In a business environment plagued with excessive excise duties, regulatory restrictions, and potential for litigation, the need for an experienced and competent management team to sustain a company’s staying power cannot be overstated. PMI’s current management has a successful and long track record of dealing with the regulatory environment all over the world. We believe management should also benefit from its experience with the legal process in the United States, arguably the most litigious society on the planet. It is worth noting that so far not a single tobacco-related case against PMI has been finally resolved in favor of a plaintiff4. PMI’s management has shown exemplary leadership on the operational front as well by growing the company’s market share by over three percentage points and expanding its operating margin from an already impressive level of over 40%.

Good Price

As prudent and cautious investors, we want not only to evaluate our downside risk but also to set our expectations properly regarding the potential upside of an investment. PMI does not appear to us as a multi-bagger stock but most certainly meets two requirements for a successful investment – safety of principal and an adequate return.

The price paid for an investment is a critical component for each of these tests. Many good businesses run by able management teams demonstrate staying power but rarely do they sell at attractive prices. PMI’s current valuation appears undemanding for a business with strong competitive positions, reasonable growth prospects, and a high return on capital.

The views expressed are those of the analyst as of December 2013, are subject to change, and may differ from the views of other portfolio managers or the firm as a whole. These opinions are not intended to be a forecast of future events, a guarantee of future results, or investment advice.

1 Source: PMI Slides / Management Comments at Morgan Stanley Global Consumer Conference, November 2013, Company Website

2 Source: PMI 2011 Investor Day Presentation, Company Website

3 Source: PMI 2012 Investor Day Presentation, Company Website

4 Source: PMI SEC Filings Form 10K (2012)

© Diamond Hill Investments

© Diamond Hill Capital Management