Part 2: US Private Sector Making Good Progress

This three-part series examines the life cycle of a debt crisis and looks at where the US, UK and eurozone are in the recovery process. This second post looks at where the US stands in the deleveraging process. Part 1 explained the phases of a debt crisis, while Part 3 will focus on why the UK and eurozone lag the US in balance-sheet repair.

When it comes to recovering from a debt crisis, the bottom line is that private-sector balance sheets must be repaired so that normal growth can resume and government revenues can be restored. In Part 1 of this series, we saw a model illustration of how this works, divided into three distinct phases. Here, we see how this has worked in practice in the US from 2000 to present.

Rapid deleveraging in the financial sector

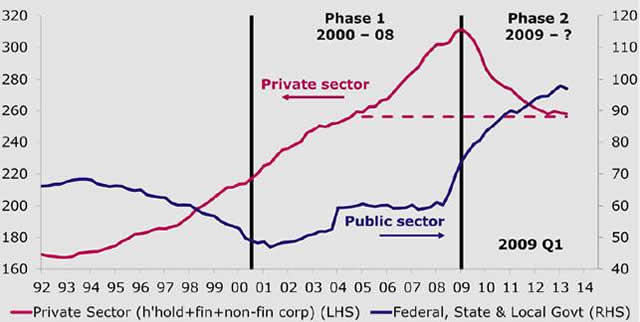

As the chart below illustrates, 2000 to 2008 represents Phase 1 of the crisis, when the bubble was inflating. In Phase 2, the US has seen rapid private-sector deleveraging and a simultaneous rise in the ratio of public-sector debt to gross domestic product (GDP). Phase 3 — when private-sector balance sheets are repaired and normal growth resumes — has not yet occurred. The red private sector line is measured by the axis on the left-hand side (LHS) and the blue public sector line is measured by the axis on the right-hand side (RHS).

Phase 2 Debt Ratios to GDP: Private Falls, Public Rises

Source: Thomson Datastream. Data as of July 31, 2013.

Source: Thomson Datastream. Data as of July 31, 2013.

The financial sector especially has deleveraged rapidly, following the bankruptcy of investment bank Lehman Brothers in September 2008.

- Banks, shadow banks and other financial institutions have sold or written down assets, reduced wholesale money market borrowings and shrunk their balance sheets.

- Banks have also raised capital — partly in response to government and regulatory requirements — while the Federal Reserve (Fed) provided liquidity through quantitative easing.

In fact, the decline in financial sector debt accounts for two-thirds of the decline in the reduction of the private sector’s ratio of debt-to-GDP. Deleveraging by the household sector accounts for the other one-third.

Strikingly good progress in US

Unlike the financial sector, the nonfinancial corporate sector didn’t need to reduce its debt ratio because it hadn’t levered up from 2003 to 2008. The private sector’s debt-to-GDP ratio has declined overall from 310% to 255%, equivalent to the level in 2004.1 This decline amounts to winding back half of the leveraging up of the private-sector debt ratio between 2000 and 2008.1 By comparison with other economies caught up in the debt “bubble and burst” process, this is strikingly good progress.

A recent slowing in the pace of deleveraging reflects two forces:

- Financial sector deleveraging is slowing.

- Nonfinancial corporations are renewing their leveraging up.

While US households continue to deleverage, the government’s debt-to-GDP ratio has risen from 60% in 2008 to 98% in the first quarter of 2013, and fell marginally to 97% during the second quarter as a result of spending cuts mandated by the Congressional sequester.1

Why does the US lead?

Faster recovery in the US compared with the UK and eurozone is attributable not so much to fiscal policy as to bank policy. US banks are in better shape because the Troubled Asset Relief Program systemically injected government capital to repair balance sheets of the largest US banks. The result has been a modest, but slow, increase in lending since 2011. In addition, the US housing market has been performing strongly, with large institutional cash buyers boosting rental housing. But signs of weakening in the housing sector have begun to appear.

If US private-sector balance sheets continue to heal — ahead of the UK and the eurozone — we’ll likely see gradual resumption of normal, self-sustaining real GDP growth over the next three to five years, which, in turn, would signal the need for gradual interest rate normalization by the Fed.

1 Source: Thomson Datastream. Data as of July 31, 2013.

The information provided is for educational purposes only and does not constitute a recommendation of the suitability of any investment strategy for a particular investor. Invesco does not provide tax advice. The tax information contained herein is general and is not exhaustive by nature. Federal and state tax laws are complex and constantly changing. Investors should always consult their own legal or tax professional for information concerning their individual situation. The opinions expressed are those of the authors, are based on current market conditions and are subject to change without notice. These opinions may differ from those of other Invesco investment professionals.

|

NOT FDIC INSURED |

MAY LOSE VALUE |

NO BANK GUARANTEE |

All data provided by Invesco unless otherwise noted.

Invesco Distributors, Inc. is a US distributor for retail mutual funds, exchange-traded funds, institutional money market funds and unit investment trusts. Van Kampen Funds Inc. is a sponsor of unit investment trusts. Both entities are wholly owned, indirect subsidiaries of Invesco Ltd.

© 2013 Invesco Ltd. All rights reserved.