Absolute Return Letter: Squeaky Bum Time

”Smart people learn from their mistakes. But the real sharp ones learn from the mistakes of others.”

Brandon Mull, Fablehaven

The 2002-03 season in the English Premier League, which ended with Sir Alex Ferguson winning a seventh Premier League title, developed into a hectic battle between Manchester United and Arsenal. At the height of the race for the title, with only a few weeks left of the season, Sir Alex uttered the now famous words: “It's getting tickly now – squeaky bum time, I call it.”

Squeaky bum time describes very well my emotional state at the moment. Equity markets continue to set new highs, seemingly prepared to disregard economic fundamentals. I have never felt entirely comfortable when I struggle to rationalise investor behaviour and I am not alone. All over the world market pundits are busy declaring this rally the latest in a long string of market bubbles which have been doing the rounds over the past few years.

Meanwhile business partner and good friend Nick Rees has now left the Canary Islands on board a rowing boat set for Antigua in the Caribbean where they expect to arrive in late January (you can follow Nick’s progress here). If you click on the race tracker map, Nick is in the boat called Team Neas Energy (very kindly sponsored by our friends in Aalborg, Denmark). Ellen (Nick’s wife) posted this report (see here) over the weekend:

“At 5pm last night (Friday) Nick and Ed were on deck, Nick rowing, Ed eating dinner. They were having a good chat apparently! A freak wave described by Nick as ‘enormous’ reared up behind the boat. The wave knocked them out of the boat and it capsized to the side, but righted very quickly and the boys (who were wired onto their safety lines) were able to get back on board safely. Nick got back on the oars to try to continue rowing, and Ed went into the cabin – however another wave threatened to roll them again and Nick joined Ed inside. They were then rocketed forward at a terrifying 14.5knots by the waves.”

Squeaky bum time indeed!

How to spot a bubble

Back to the infamous bubbles. Not the sort of bubbles most of us enjoy at New Year but man made bubbles. Bubbles that are the product of irresponsible behaviour and greed. Bubbles that can destroy wealth in no time at all. There is a long history of deflated bubbles beginning with Tulipmania in the Netherlands in the 1630s1. When a bubble bursts, the typical monetary policy response is to flood the markets with liquidity. The 2008 occasion was no exception. Central banks all over the world provided, and five years later continue to provide, ample supplies of cheap money.

The results are there for everyone to see. Asset prices have rallied strongly as I pointed out in the November Absolute Return Letter. Yet rising asset prices, even rapidly rising asset prices, are not necessarily akin to a bubble. One must distinguish between what is sustainable and what is not. The Financial Times Lexicon defines an asset bubble this way:

“When the prices of securities or other assets rise so sharply and at such a sustained rate that they exceed valuations justified by fundamentals, making a sudden collapse likely - at which point the bubble bursts.”

Asset bubbles are not always easily identifiable. Alan Greenspan has been widely ridiculed for asking the following question:

“How do we know when irrational exuberance has unduly escalated asset values, which then become subject to unexpected and prolonged contractions?”

The man has a point, though. We can all spot the bubbles when using the rear-view mirror, but that is a luxury only available to academics and couch potatoes. Investors do not have the luxury of a rear-view mirror2. We need to make real time calls all the time and that is not always straightforward. A 1963 Ferrari 250 GTO changed hands back in October for no less than $52 million. Only four weeks ago a Francis Bacon painting fetched $142 million at an auction in New York. I feel very tempted to declare both of those transactions a product of irrational exuberance. Who in their right mind would pay those prices for unproductive assets? Yet I feel tempted to quote the age old Danish saying: “What do farmers know about pickled cucumbers?” I hope you get my point.

When I look at Bitcoin, the chart screams ‘bubble’ to me but how do I value it? I am not smart enough to figure that out. In such a situation the wise move is no move. Another example: Central London property prices. Reasonably intelligent people declared London property to be in a bubble more than a decade ago. Meanwhile prices continue to rise. Is it a bubble? I don’t know, but I do know that as long as misguided politicians in France, Spain, Italy and Greece continue to make bad policy decisions that make their own citizens pack up and leave, London will continue to prosper (and price normal people out of the property market, but that is another story altogether). As long as there doesn’t seem to be any shortage of stupidity amongst the political elite in Europe, I will not bet against further price increases on central London property.

The DNA of the 2012-13 bull

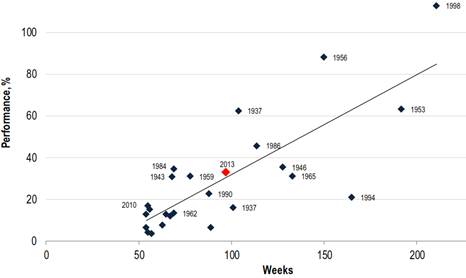

Now to the big question: Is there a bubble in global equity markets? That is what the rest of this letter is all about. Let’s begin by putting the current rally into a historical context. Chart 1 shows all uninterrupted S&P 500 bull runs since 1927 that have lasted 50 weeks or longer. Altogether there have been 25 of them and, contrary to what many seem to think, the 2012-13 rally is not an outlier. It has neither been exceptionally long, nor has it delivered outsized returns (yet), at least when compared to the other major bull runs.

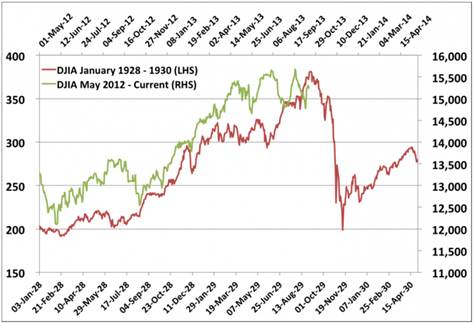

This hasn’t prevented many commentators from raising the red flag. Allow me to share a few examples with you (forgive me for the number of charts to come, but they often say more than thousands of words). One of the most popular charts on financial blogs in recent weeks compares the ongoing rally to the great bull market of the late 1920s which, as we all know, ended very badly (chart 2).

Chart 1: S&P 500 bull runs since 1927

Source: Ineichen Research & Management.

I am amazed to see how much value many investors assign to charts like these. What does chart 2 really tell you? As far as I can tell not much. For every chart that suggests a relationship, I can find two that contradict it. To me technical analysis is long on voodoo and short on substance (I may have lost a couple of thousand readers right there, but so be it).

Chart 2: The 2012-13 bull market vs. 1928-30

Source: http://allstarcharts.com/fair-compare-market-1929/

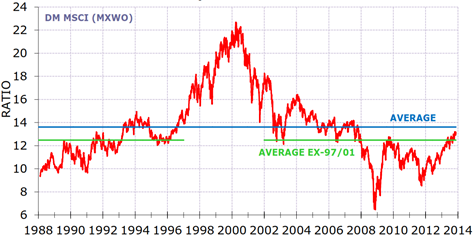

Another popular chart doing the rounds in recent weeks is the so-called Death Cross shown below (chart 3) which has been presented as ‘proof’ that global equity markets are on collision course with economic fundamentals.

Chart 3: Global equities vs. economic fundamentals (simplistic study)

Source: http://www.zerohedge.com/news/2013-11-22/behold-worlds-real-death-cross

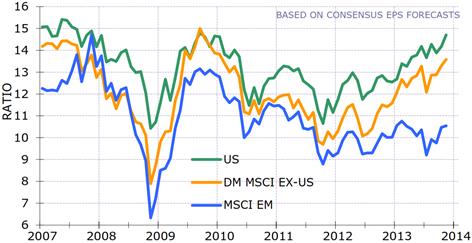

A more thorough analysis would reveal that the relationship between equity markets and economic fundamentals broke down a couple of years ago (chart 4). In fact, and as we shall see later, there is absolutely nothing unusual, let alone alarming, about such a disconnect. It is all about where we happen to be in the economic cycle.

Chart 4: Global equities vs. economic fundamentals (detailed study)

Source: Minack Advisors

Another very popular chart, showing an apparent link between the expansion of the Fed’s balance sheet (i.e. QE) and the rise in U.S. equity prices, has been marketed recently as Perhaps the only chart that matters (chart 5).

Unless one digs a little bit deeper, it is easy to get carried away when looking at charts like these, but digging deeper is precisely what the good people at Minack Advisors have done and their findings are quite interesting. If QE was solely responsible for the re-rating of equities that has taken place, one would expect a strong correlation between P/E ratios and the size of central banks’ balance sheets throughout the post-crisis period (i.e. from early 2009); however, P/E ratios actually contracted during the first two years of QE (chart 6). In other words, QE alone does not explain the recent bull-run.

Chart 5: QE vs. equities

Now, before you jump to conclusions, do not for one second think I am about to do a Hugh Hendry (Hugh, CIO of Eclectica Asset Management and a long-standing bear, threw the towel in the ring a few weeks ago and turned bullish for the first time in years). I cannot possibly do what Hugh Hendry did because I was already bullish. Having said that, many more will do what Hugh Hendry has just done. The recent rally is still not widely embraced. Many investors continue to be deeply suspicious about the underlying economic reality and for good reasons, I might add. See for example this article in the FT.

Chart 6: QE vs. equity market valuation

Source: Minack Advisors

The beauty of financial alchemy

Talking about having good reasons to be suspicious, take a look at chart 7, courtesy of Bill Gross and PIMCO. Even a casual look at the chart suggests that the chickens may still come home to roost. U.S. corporates are desperately trying to deliver earnings growth when measured on a per share basis even if the underlying earnings trend is flat to negative. The primary tool to achieve such magic is obviously stock buy-backs. A whopping $1 trillion (+/-) is spent every year on buyback programmes in the U.S. just to keep the show on the road.

Chart 7: The art of financial alchemy

Source: PIMCO, Bianco Research

There are potentially two dynamics at work here. The first one is straightforward – the economic cycle. Perhaps chart 7 is telling us that the U.S. economy – and more broadly the global economy - is not quite as robust as U.S. corporates want us to believe. The second one is more complex and has to do with how national income is divided between labour and capital.

For many years it was a relatively stable relationship. 65% of national income went to labour with the balance going to the owners of the capital3. As recently as 10-12 years ago that was still the case. Then things started to change and labour’s share has been under pressure ever since. Today labour receives just short of 60% of national income.

The reason I bring this up in the context of chart 7 is that there are signs that labour’s share of total income may have begun to mean revert with labour again taking a larger share of national income which, if sustained, will put corporate profits under pressure in the years to come. It is still early days, but it’s worth a separate discussion which I will revert to in one of the next Absolute Return Letters.

Bubble or no bubble?

In the meantime, let’s try and get back to the central question in this month’s letter – bubble or no bubble? In order to answer that question we need to look at some valuation charts. Chart 8 doesn’t provide much comfort for the bulls. Four different valuation metrics lead to more or less the same conclusion – U.S. markets are significantly overvalued although not yet at levels seen at the peak of the secular bull market in 2000.

Chart 9 which measures the aggregate valuation of all developed markets paints a quite different picture. There is nothing to suggest that valuations are in any way excessive. Even when adjusting for the lofty days of the late 1990s (the green line in chart 9), global equity markets appear only to be very modestly overvalued.

Chart 8: Different valuation metrics applied to the U.S. market

Source: Advisor Perspectives (see here).

Our suspicions are confirmed when we compare U.S. equity valuations to those of other markets (chart 10). It is obvious from this chart that the strong bull-run in U.S. markets has opened up a significant valuation gap, in particular vis-à-vis emerging markets. One should also remember that European corporate earnings are depressed at present, sending valuations higher so, on a cyclically adjusted basis, European equities look much more attractively priced than their U.S. peers.

Chart 9: Valuation of equities in developed markets (two year forward P/E)

Source: Minack Advisors

The real opportunity set seems to lie in emerging markets, though. Once global economic growth re-accelerates, EM equities are likely to come back into favour, and much of the valuation gap could and should disappear as a result.

In a bubble-like environment investors rarely distinguish between good and bad. We saw it in the late 1990s when low quality dot com companies were bid up to ridiculous valuations and we saw it again in the housing bubble in the mid naughties when investors forgot about the golden rule of property investments – location, location, location. When I look at investor behaviour today, I see the opposite. Most, if not all, investors, are highly selective and approach markets with a great deal of scepticism.

Chart 10: A growing valuation gap

Source: Minack Advisors

Our friends at Sanford Bernstein ran an interesting chart for me which partly supports my argument. Investors have not yet fully embraced this rally. They have invested in a ‘cowardly’ fashion, focusing on defensive, low beta stocks rather than more aggressive, often cyclical, high beta stocks (chart 11). If history provides any guidance, there will be a shift to more cyclical, higher beta names, before this rally is well and truly over.

Chart 11: Price-to-Book Valuation - High vs. low beta stocks

Source: Sanford Bernstein. MSCI Developed Markets, Jan. 1980 – Nov. 2013.

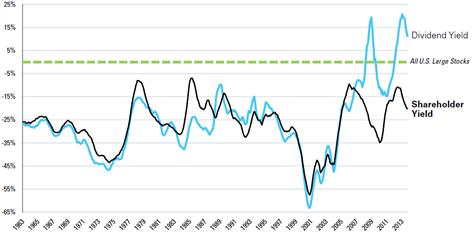

Chart 12 provides further insight into what it is investors have actually been chasing in the recent rally. As one can see, stocks with the highest dividend yields have become quite expensive, even if valuations have come back down somewhat more recently. It is almost unheard of for the highest yielding stocks to trade at a premium to the large cap universe, but they do now and have done for a little while.

Now, any company wanting to return capital to investors can choose to do so through dividends or alternatively through share buy-backs. The black line in chart 12 (shareholder yield) combines share repurchases and dividends. As one can see, investors have not taken buy-backs to their hearts in the same way they have rewarded the highest yielding companies. The answer, I believe, lies in the relentless appetite for yield which is a direct function of the changing demographic landscape with millions of baby boomers worried about how to fund their retirement.

Chart 12: Valuation discount – top quintile yield vs. U.S. large cap

Source: O’Shaughnessy Asset Management. Valuations based on trailing 12 month P/E ratios.

The typical equity cycle

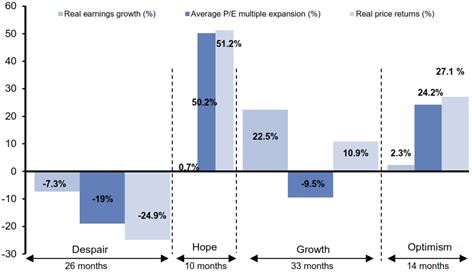

It is time to re-visit one of the issues I discussed in the early parts of this letter – should we worry that the link between equity markets and economic fundamentals seems to have broken down? Peter Oppenheimer, European Equity Strategist, produced an interesting chart in a recent research report, which casts some light on this question. Looking at economic cycles since 1973, he divides the equity cycle into four phases – despair, hope, growth and optimism (chart 13).

Chart 13: Phases of the ‘typical’ equity cycle

Source: Goldman Sachs Global Investment Research. Europe ex. UK. Based on economic cycles back to 1973.

Peter argues, and I am inclined to agree, that we are coming to the end of the hope phase which is the part of the equity cycle where returns are the highest. In the next phase - the growth phase – returns are likely to be much more modest and largely a function of the companies’ ability to convert the accelerating economic momentum into rising corporate earnings. You will also note from chart 13 that, in the growth phase, P/E multiples actually contract somewhat, yet earnings growth more than compensates for that, leaving investors with a positive, albeit relatively modest, return. It is only in the final phase of the equity cycle (optimism) that investors tend to get carried away and build in unrealistic expectations which they subsequently pay dearly for in the despair phase.

Goldman’s research is based solely on European data. One might argue that the U.S. is well in to the growth phase and thus closer to the exit point than most other markets. I wouldn’t disagree with such an observation.

Conclusion

Being closer to the exit point does not, however, imply bubble behaviour. Yes, there are signs of excesses creeping back in to the markets. The FT ran a piece on asset-backed securities recently which should worry everyone (see here) and, yes, covenant light loans are yet again on the rise (see here); however, I do not see much in terms of the classic signs of bubble behaviour – excess leverage, taxi drivers giving you his stock pick de jour, etc. etc. It is, after all, the most unenthusiastic rally I have ever experienced.

One of the key reasons for the apparent lack of enthusiasm is the widely held view that interest rates will begin to rise before long. Some disagreement exists as to when and by how much, but one has to look really hard to find dissenters who are prepared to take the view that interest rates could indeed fall further. I should add ‘before they rise’ because ultimately they will rise. I think we all know that. However, one important lesson learned from Japan is that it is the ‘when’ that we may get so horribly wrong. With current inflation trends in mind, it is not beyond comprehension that we could see 10-year bond yields hit 2% before we touch 4%. One lesson I learned many moons ago is never to underestimate the markets’ insatiable appetite for inflicting maximum damage.

On the other hand, should interest rates begin to normalise, going to say 4-5% on the 10-year bond, I wouldn’t be overly concerned about that either, as long as it happens in an orderly fashion. Chart 14 shows the correlation between interest rates moves and equity returns. As one can see, in the past, upwards moves in interest rates have only hurt the stock market when rates have been north of 5%.

Chart 14: The bond vs. equity sweet spot

Source: JP Morgan

Nor am I troubled about all the tapering talk. Financial markets took a bit of a knock back in May and June following Bernanke’s comments on 22 May which markets were completely unprepared for. Now, almost seven months later, the necessary expectation adjustments are largely behind us, and tapering will most likely turn out to be a non-event.

Having said that, we are not out of the woods yet, economically speaking. We will have to face many challenges over the next several years yet, on the margin, things are getting better and, as long as that is the case, the stock market is likely to respond in kind, even if the easy money has been made at this point.

For all those reasons I remain a cautious bull.

Niels C. Jensen

16 December 2013

© Absolute Return Partners LLP 2013. Registered in England No. OC303480. Authorised and Regulated by the Financial Conduct Authority. Registered Office: 16 Water Lane, Richmond, Surrey, TW9 1TJ, UK.

Important Notice

This material has been prepared by Absolute Return Partners LLP ( ARP). ARP is authorised and regulated by the Financial Conduct Authority in the United Kingdom. It is provided for information purposes, is intended for your use only and does not constitute an invitation or offer to subscribe for or purchase any of the products or services mentioned. The information provided is not intended to provide a sufficient basis on which to make an investment decision. Information and opinions presented in this material have been obtained or derived from sources believed by ARP to be reliable, but ARP makes no representation as to their accuracy or completeness. ARP accepts no liability for any loss arising from the use of this material. The results referred to in this document are not a guide to the future performance of ARP. The value of investments can go down as well as up and the implementation of the approach described does not guarantee positive performance. Any reference to potential asset allocation and potential returns do not represent and should not be interpreted as projections.

1 I am sure there are bubbles that predate Tulipmania, but that is considered to be the first widely documented asset bubble.

2 There is at least one exception to this rule. In my younger days, before moving to London, I worked for a Danish bank. The head of our group was notorious for telling everyone who cared to listen what we should have done yesterday. When he turned 40 we gave him a rear-view mirror for his birthday.

3 The numbers quoted here are based on U.S. data. Numbers from other countries vary somewhat in absolute terms, but the trend has been universal. All over the world, labour has lost share to the capital owners.

© Absolute Return Partners