The Impact of the Great Recession and Federal Reserve Accommodation on Households

The latest release of macro data came out today from the Fed Flow of Funds report generated by the Federal Reserve. We monitor this with great anticipation so as to measure possible direction changes or momentum of a current direction. There are a myriad of data points, however, a few select charts should continue to raise confidence in the direction of the economy and, at worst, a liquidity-driven backstop to maintain consumption at minimum agreeable levels.

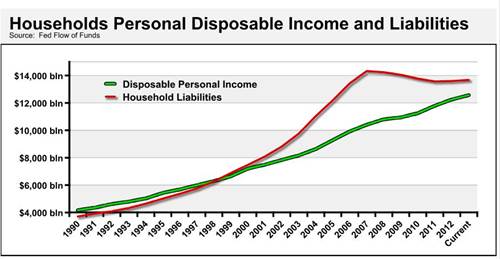

The first is the comparison of household disposable income and total liabilities. With the low interest rate environment curtailing interest rate charges and energy now in a renaissance period, disposable income has actually continued to grow despite the recession. Debt levels though are still below the 2007 peak levels.

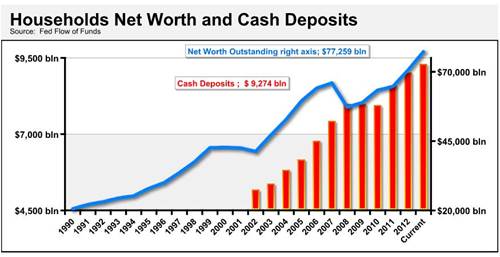

Perhaps the most profound chart is the one designating total deposits and net worth that are at all-time highs. This may be the real “Bernanke Put” in the economy.

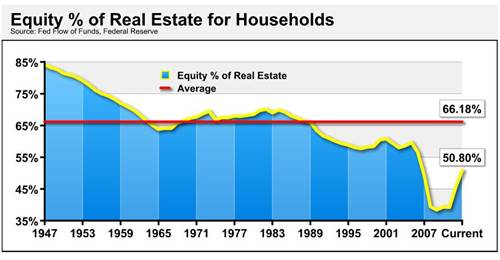

The “households net worth and cash deposits” chart – or the “duh” chart, as I like to call it – is the recovery in the housing market as evidenced by the percentage of equity in real estate that just breached the 50% level, where it has been since 2006. Notice it is still well below the average over the past 65+ years. There is still quite an amount of room to recover to get to the long-term average or even a more reasonable level average over the last 30 years of close to 58%.

The “equity % of real estate for households” chart is one we call the “replenishment rate” which measures the percentage of net worth to disposable income.

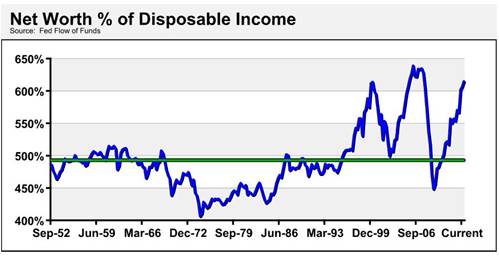

*The green line in the chart above represents the average

Interpreting the “net worth % of disposable income” chart will depend greatly on your anxiety level and bull or bear market slant. The last two times this multiple hit over 600% was March 2000 (six months prior to peak in S&P 500 before correcting) and June 2005. The market continued to grow from June 2005 for the next 25 months, during which it averaged 13.4% annually until October 2007.

For further clarity on whether the numbers are telling us the results from March 2000 or June 2005 are closer to what the metric is telling us now and the impact on the markets, consider that percentage of corporate equities and mutual fund shares were 27.6% of total net worth in March 2000 and 20.5% in June 2005. This could be interpreted that there was a larger share of net worth being invested in equities in 2000 versus 2005. The current level needs to be blended over the last few quarters of 2013 since this data is heavily adjusted as time goes on. By blending the entire 2013 levels, we come to a rough level of 23%.

The last condition that needs to be considered is timing of breaching the 600% levels. The March 2000 level preceded a recession by 12 months and followed the last recession by nine years…clearly “long in the tooth.” June 2005 preceded a recession by 30 months (2.5 years) and followed the last recession by roughly 41 months or approximately 3.5 years.

Now that we have qualified the many viewpoints this last chart could detail, the question is, what does it mean to us? We continue to see growth in the domestic equity markets for a multitude of reasons, least of which is the lack of supply that seems to dominate the trading. Between buy backs and fewer companies listed as detailed by following article on Yahoo! Finance, The Stock Market is ‘Shrinking,’ Despite Record-High Indexes. We also see aggressive GDP prints relative to recent history, large hoards of cash on banks, corporations and consumers’ balance sheets and an anchored Fed Funds Rate for the foreseeable future, as points in favor of continued growth despite the significant run up over the last four years.

This commentary is for informational purposes only. All investments are subject to risk and past performance is no guarantee of future results. Please see the disclosures webpage for additional risk information. For additional commentary or financial resources, please visit www.aamlive.com/blog.

© Advisors Asset Management