Float Research Bubble Watchers Should Set Their Sights on Corporate Bond Market

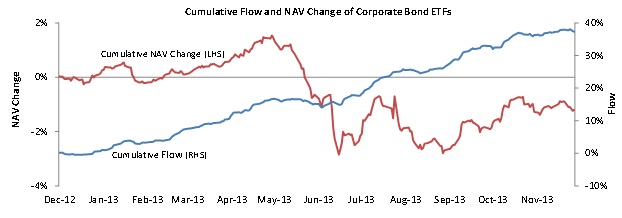

Insatiable Appetite for Corporate Debt Despite Poor Performance. Corporate Bond ETFs Issue Staggering $21.6 Billion (27.5% of Assets) Year-to-Date.

We have read a lot of chatter about bubbles in recent months. We think investors looking for bubbles will find the credit markets a lot more bubbly than the equity markets. Investor appetite for corporate bonds—particularly investment-grade corporate bonds—is seemingly insatiable despite near record low yields and persistently poor performance.

Corporate bond ETFs posted steady inflows in the past year even though the average fund delivered a net price decline in this period. Most recently, Corporatebond ETFs issued $641 million (0.8% of assets) in the past month and $6.2 billion (7.9% of assets) in the past three months. The year-to-date inflow now totals a staggering $21.6 billion (27.5% of assets). It is amazing how eager investors are to lend money to companies at pathetically low yields.

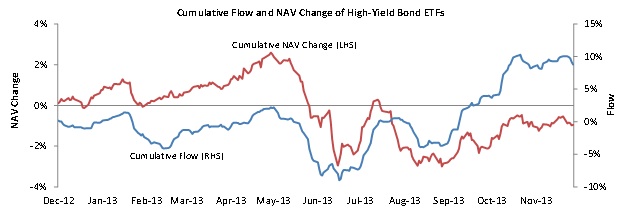

Enthusiasm was much cooler for high-yield debt than for investment-grade debt in the past year. While inflows into High-Yield bond ETFs picked up to $4.0 billion (11.4% of assets) in the past three months, the year-to-date inflow amounts to a mere $3.3 billion (9.4% of assets).

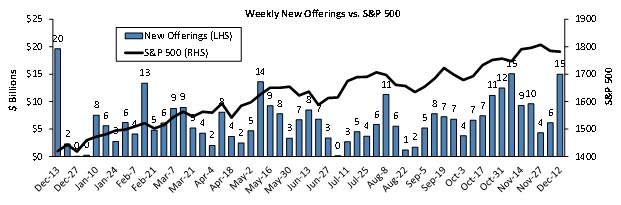

Post-Thanksgiving Share Selling Frenzy Piles Pressure on Stock Market. Underwriters Set to Dump Almost $10 Billion in New Shares into Market on Wednesday and Thursday.

Contrary to what journalists want us to believe, Wednesday's sell-off probably had far more to do with a spike in corporate share selling than it did with the Washington budget deal; the rumored nomination of Stanley Fischer to be Federal Reserve Vice Chairman; or our perennial favorite, 'disappointing earnings.' Underwriters are scrambling to unload as much as they can before the new offering calendar's winter snooze. All else being equal, the more new shares underwriters sell, the less money is left in the checking accounts of stock market intermediaries to buy existing shares.

The 'white shoes' already pumped out $4.6 billion from Friday through Tuesday, and Dealogic reports that a whopping $6.5 billion is scheduled for Wednesday—led by big IPOs for Hilton Hotels ($2.5 billion) and Aramark ($900 million) and secondaries for Pinnacle Foods ($550 million) and SeaWorld Entertainment ($550 million)—and $2.3 billion is scheduled for Thursday—led by a follow-on for Darling International ($900 million) and an IPO for CheniereEnergy Partners LP Holdings ($700 million). Add some more overnight deals, and new offerings should easily hit our upfront estimate of $15 billion this week, which would be the highest level this year.

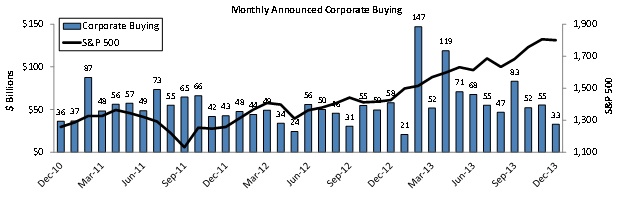

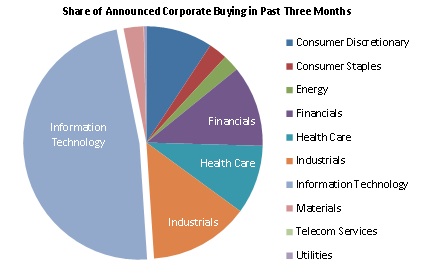

Corporate Buying Extremely Concentrated: Information Technology Firms Account for 48% of Corporate Buying Announced in Past Three Months.

Companies have continued to announce plenty of float shrinklate this year as stock prices have chugged higher. Announced corporate buying has topped $50 billion in all but two complete months this year.

What these aggregate totals mask is that corporate buying has become more and more concentrated. Information Technology companies accounted for 48% of the corporate buying announced in the past three months. This strength is the key reason we are long Information Technology in our sector model portfolio.

No other sector accounts for even 15% of corporate buying, and the sectors with the next largest shares are Industrials (14%), Financials (11%), and Health Care (10%). Note that corporate buying has been very low in both consumer sectors, particularly in Consumer Staples.

This communication is a publication of TrimTabs Asset Management. It should not be regarded as a complete analysis of the subjects discussed. All expressions of opinion reflect the judgment of the authors as of the date of publication and are subject to change. Information presented does not involve the rendering of personalized investment advice. Content should not be construed as an offer to buy or sell, or a solicitation of any offer to buy or sell the securities mentioned herein. Performance results for investment indexes and/or categories, generally do not reflect the deduction of transaction and/or custodial charges or the deduction of an investment-management fee, the incurrence of which would have the effect of decreasing performance returns. All information is based on sources deemed reliable, but no warranty or guarantee is made as to its accuracy or completeness. Past performance may not be indicative of future results. Therefore, no investor should assume that the future performance of any specific investment or investment strategy will be profitable or equal to past performance levels. All investment strategies have the potential for profit or loss. Changes in investment strategies, contributions or withdrawals, and economic conditions, may materially alter the performance of an investor’s portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment or strategy will be suitable or profitable for an investor’s portfolio.

© AdvisorShares