The Fed, Inflation, and the Perfect Storm in Gold Miners

Executive Summary:

- Neither hopes of job creation nor fears of inflation (based on the massive expansion of the monetary base since late 2008) have thus far materialized.

- Total credit creation (i.e. money supply) during most of the last five years either shrank or barely grew despite massive growth in the monetary base.

- Nominal GDP (growth plus inflation) grows in response to total expansion of credit (both from the Fed and the banking system), not just the monetary base.

- How much excess money growth turns into inflation depends on trends in labor productivity.

- Money supply growth may actually accelerate as the Fed reduces Quantitative Easing if banks expand credit, as they are currently doing.

- Gold mining stocks have been pummeled as inflation fears based on the growth in the monetary base have failed to materialize.

- Gold prices have lost 1/3 of their value in the last couple of years.

Mining companies are in survival mode, selling gold, restructuring production costs, and we are likely to see industry consolidation.

- Short-term headwinds to the price of gold-mining stocks have been priced in while a likely rise in growth, inflation and a stock market correction are being ignored. This creates a tremendous investment opportunity at current prices.

We closed our last letter with a brief mention of the precious metals market and our interest in gold mining stocks. To reiterate:

“In financial matters, the best long-term protection (not necessarily always the greatest short-term profits) comes from owning undervalued assets. We are bargain hunters, not “gold bugs”. We do not subscribe to the religion that precious metals will always protect you in a financial crisis…Today the most hated shares in publicly traded markets are gold mining companies…Now that almost everyone has abandoned the belief that inflation will return, the opportunity posed by these shares is incredible. Over the last six months we have raised our exposure to gold mining companies to its highest level in almost two decades. We believe strongly that the Fed will succeed in raising inflation over the next decade.”

Five years ago the Federal Reserve embarked upon an experiment to create jobs by monetizing the record federal deficit. It was supposed to work like this:

Begin with a rapid expansion of the monetary base (essentially printing money). This expansion of the monetary base would then expand the money supply despite a dysfunctional banking system. This began during the financial crisis and certainly during the nadir, Fed intervention mitigated some of the negative effects of the banking crisis. Economic growth was expected to follow the monetary expansion enhanced by a wealth effect from inflating asset prices (stock, bond, and housing prices). Although it was recognized that higher consumer prices (inflation) might follow later on, the risk was seen as a necessary evil.

Unfortunately in retrospect, a strong case can be made that the Fed has failed to either create jobs or even generate a normal post recession recovery. The “wealth effect” had a huge impact on income distribution, but created few jobs. What is truly shocking is that the Fed didn’t even succeed in growing the money supply until a year ago.

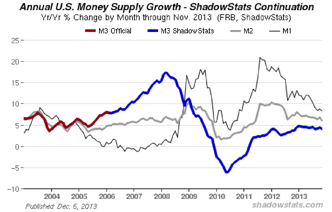

With a banking system in survival mode after the financial crisis unwilling and unable (due to regulatory and capital restrictions hoisted upon them) to distribute this expanded monetary base to the real economy, money supply growth remained disinflationary until two years ago rather than expanding at an inflationary pace as investors and the public expected. Only in the past year has monetary growth become mildly inflationary as banks have begun lending again. The chart below shows growth rates of three different measures of money supply: M1, M2, and M3 (the Fed no longer publishes M3 and broader measures). Over the very long-term all three measures tend to grow at similar average rates, but in the short-term the growth rates vary depending on what is going on in the banking system.

The concept of the “money supply” and how the Fed influences (not controls) it is widely misunderstood. M1 represents mostly cash and checking accounts, while each higher numbered “M” (i.e. M2, M3, etc) add additional components. Using the monetary base, M1, or even M2 simply doesn’t tell us much in an era of electronic money movement. While M1 is heavily influenced by the monetary base, the broadest (and by virtue, the best) measure of money supply we still have reliable estimates for is M3 (thanks to John Williams at Shadow Government Statistics). When M3 growth is decelerating (i.e. 2009), deflation is a real risk. Conversely when M3 growth is accelerating (i.e. 2007), inflation becomes a serious threat. The problem for forecasters is that money growth can take a long time to respond to changes in the economy or Fed policy while inflation can take a long time to respond to changes in money growth.

Pushing on a String? Or Pulling on a Rubber Band?

Economist and investor Lord Keynes suggested that there are times when Fed stimulus is about as effective as pushing on a string. I think a better analogy would be pulling on a rubber band. Until the rubber band stretches to the point where it overcomes the inertia of what is being pulled there is no movement. When that tipping point is reached, the pace of movement accelerates, often rapidly. The economy and inflation are being pulled (up or down) by the monetary policy of the Fed via a rubber band (the fractional reserve banking system). It can take a long time for the banking system to change directions when the Fed starts raising or lowering interest rates.

Recently, growth rates in the various money measures have converged. Money growth has started to become more dependent on the loan portfolios of banks and relatively less dependent on the Fed. For all those who have wondered why all this money growth hasn’t resulted in soaring inflation, the answer is twofold:

- Inflation only accelerates longafter money growth accelerates.

- Only in the last year or so has money growth accelerated to levels consistent with sustained growth rates in nominal GDP (the sum of real economic growth and inflation) above 4%.

However once monetary expansion shifts from the Fed to the banks, the Fed just like the rest of us will be reacting to rather than causing faster money growth. M3 growth exploded from 2005 through 2007 supporting the massive inflation in home prices that was morphing to other consumer prices while Fed rate hikes were slowing M1 growth to zero. After a couple years with apparently little effect, suddenly an invisible live was crossed and the housing bubble popped. Now after years of shrinking, the money supply is once again growing.

Productivity Distinguishes Growth From Inflation

While rapid monetary growth is a prerequisite to rising inflation, it isn’t the only factor. The percentage of nominal economic growth (real growth + inflation) that comes from inflation depends on worker productivity. During the past four years productivity growth has been at record lows (1% vs. 2.2% post WWII average) and has essentially flat-lined in the past year.

In the short-term, productivity is affected by the business cycle. When the economy stops contracting and starts expanding (at the bottom of the recession) productivity briefly soars because businesses can increase production without hiring anyone. Productivity declines a couple of years into the recovery because companies have to start paying up for skilled labor that has at that point become a scarce resource. Future productivity gains then depend on investment in new technology. Unfortunately, business investment in capital equipment (technology) over the last 5 years (as a percent of GDP) is at the lowest level of any five-year period in the last six decades. This reflects both where we are in the cycle as well as the recent dearth of investment. It will take years of catch up investment before productivity growth returns to even normal levels.

Low Productivity + Money Growth = Inflation

Near 5% money growth over the past year makes it reasonable to expect nominal GDP to accelerate from the 3-4% range it has remained recently. Over this period, sub 4% nominal GDP has meant sub 2% real growth and sub 2% inflation.

In the near-term, the absence of any serious potential for productivity growth implies inflation will consume the larger part of any increase in nominal GDP. Fears that the end of QE will represent a slowdown in money growth

are unfounded. QE supplied the banking system with tanker cars of the rocket fuel for future inflation that remains in storage. Until recently the dysfunctional banking system had its foot on the brake. All the money the Fed pumped into the bond markets never got levered up through the banking system into the money supply. Recently bankers have gently shifted their foot from the brake to the gas pedal. Bank earnings from accounting maneuvers of reduced provisions for loan losses and fee income from mortgage refinancings (that they sold to Fannie and Freddie) have been exhausted. Banks now need to expand lending to maintain profitability.

The Fed may be the most important single influence, but in an era of electronic banking, money supply is composed primarily of bank created credit. The main limitations to bank credit creation are:

- regulations on bank capital

- lack of excess reserves

- nominal economic growth

- and the willingness to lend

The concerted effort of banks to raise capital over the last few years has alleviated the first restriction, while the Fed’s balance sheet expansion has flooded the system with excess reserves. The combination of faster nominal GDP growth, excess bank lending capacity, and banks’ desperate need for new income virtually assures more lending and the faster money growth that comes with it. As in 2006 and 2007, the only way the Fed can control the rate of expansion is to shrink its balance sheet with higher interest rates. This, as always, will prove to be much more an art than a science. Actions by the Fed are arithmetic while the reactions in the banking system (both up and down) are exponential.

Make no mistake, despite all the fears of the Fed tapering QE, money growth will accelerate now that the banks are beginning to remember how much fun it is to sow their wild oats. Once the banks are cranked up, only aggressive Fed tightening (or a bursting credit bubble) can slow the process. Aggressive Fed easing may be politically acceptable, but aggressive Fed tightening won’t get support without a serious inflation scare.

The Perfect Storm in the Gold Mines

This lag between the creation of money and the growth of the money supply has created an exceptional opportunity. In recent years investors have consistently interpreted aggressive Fed policies as an expansion of the money supply, when it was not. No group of investors has misread the inflation landscape worse than investors in precious metals. Precious metals soared prior to the financial crisis in expectations of higher inflation ignoring the fact that the Fed was in fact trying to restrict credit growth (that was actually a good call for a while because M3 money supply was expanding rapidly, but then ignored the fact the Fed was holding on to the rubber band, slowing M1 growth to zero). The screams from precious metal advocates about the Fed’s post crisis expansion of the money supply never ceased despite the fact money supply shrank for two years (the blue line below 0 in the chart) and until recently remained at disinflationary levels. If you really believe that excessive money growth is the primary source of inflation, you shouldn’t worry too much about inflation until the money supply starts growing.

The persistent lack of the inflation they feared resulted in a panicked exodus from exchange traded funds like GLD (as well as related gold mining shares and funds that invest in them) driving the price of gold and related investments ever lower. Compared with their highs a couple of years ago, gold prices have lost 1/3 of their value, while mining shares have lost 2/3 of their value. Amazingly, mining shares are trading at the prices they were trading in 1994 when gold was selling at 1/3 of current prices! Admittedly it costs more to extract gold today, but I see this unloved sector of the market as a potential (please forgive the pun) Gold Mine.

Until the introduction of exchange traded funds like GLD (whose sole asset is physical gold), mining stocks generally tracked the price of gold. Physical gold offers perceived protection against financial Armageddon and threats to privacy and confiscation that financial holdings like GLD, mutual funds, and mining stocks lack. Certainly, if you live in an unstable place like Syria or Egypt, those benefits are very real. In flawed, but relatively stable developed economies, metals related financial holdings offer similar protection from current devaluations but are infinitely more liquid. Liquidity is important because buying, selling, and storing individual holdings of physical gold is expensive and gold prices don’t move in a straight line.

Although we would like to outsmart other investors over every investment horizon, our short-term track record can occasionally be dismal. Our long-term track record is dramatically better because we excel at recognizing the obvious. We do most of our buying when asset prices are depressed and most of our selling when asset prices are inflated. The markets almost always move farther than we expect which causes us some temporary pain, but this approach has paid off well over time.

Focusing on the obvious, markets are cyclical. The S&P 500 is trading at all time highs while gold mining shares are trading at decade lows. In a sluggish but stable economy with falling gold prices and no perceived risk of inflation, gold mining shares are the asset class most despised by the investment community. Naturally we see this as an incredible opportunity. These stocks go through phases where they track common stocks almost perfectly, as well as phases where they move in polar opposite directions. Both of those characteristics are apparent in the chart below showing the historical performance of the Fidelity Gold Fund (FSAGX) in comparison with US common stocks as represented by the S&P 500 over the past 25 years (I selected FSAGX for the chart because it has a much longer history than exchange traded funds like GDX).

A few things jump out.

- First, if you can stomach periodically losing half your portfolio value in a couple of years, common stocks have been a much better “buy and hold” investment than mining shares.

- Second, you don’t avoid that volatility by buying and holding mining stocks instead.

- At times both mining shares and common stocks may be either expensive or cheap and may even move in the same direction. When one group is very elevated (currently common stocks) relative to the other (mining stocks are cheap) it becomes pretty obvious where the big risks and where the big opportunities are.

These disparities don’t happen by accident. They reflect excessive focus on recent experience. Recently gold prices have suffered the perfect storm. Low inflation, economic stability, a modest rise in interest rates, and competition from a soaring stock market for investor dollars have left the miners supremely unloved. Mining companies benefit or suffer from rising gold prices for obvious reasons. But unlike physical metals as an investment, these companies generate income when the price of gold goes sideways. Stock prices in general and mining stocks in particular almost always reflect the human tendency to expect recent conditions to extend indefinitely into the future, despite history that shows a relentless series of cycles.

Mining Stocks

Mining stocks are buffeted by all the factors that affect the prices of both precious metals and common stocks, but are affected uniquely by the behavior of the companies and industry itself. In many ways miners are like banks. Both have a history of bad management in good times and they seem to only get their act together when stuff starts hitting the fan. Also like banks, miners are essentially in the business of creating money. When you create too much money, the value of the money goes down. When you create too little money, the value of the money goes up. Both banking and mining earnings are amplified by leverage. Banks are highly levered on borrowed money, while gold mining profits are highly levered to the price of gold. Unlike the banks, miners don’t have the government standing by to bail them out. But when the government bails out the banks, currency depreciation pushes up inflation and boosts metal prices.

It should be obvious from the chart that there is no simple relationship between the price of common stocks and mining stocks. The extreme cyclically of both makes a compelling argument that very short-term cycles dramatically impact the price of both of these very long-term assets. We try to distinguish between cyclical factors like interest rates and more permanent considerations like the outperformance of common stocks over very long periods of time. Over very long periods of time, stocks will always outperform mining stocks simply because of “survivorship bias”.

Despite bankruptcies, consolidation, etc, gold mining companies are always going to be gold mining companies. As a sector, sometimes they make money, sometimes they lose money. The S&P 500 on the other hand is constantly changing. Companies in expanding industries are replaced by companies in declining industries for purposes of the index. This “invisible hand” of free market capitalism gives the S&P 500 index a very long-term upside bias beyond inflation that will never be present in mining stocks as a sector. Over years or even decades, mining stocks can however present much better opportunities than common stocks. I believe that one of those opportunities is now.

Just before the financial crisis we exited a major position in gold mining stocks (that we acquired following the internet bubble). Leading up to the crisis M3 money growth was highly inflationary but the Fed was resisting that growth so the rubber band got stretched very tight by late 2007. Since the financial crisis we’ve taken a couple of minor short lived mining stock positions in expectation that aggressive Fed policies would result in faster money growth. The money growth never happened. Only in the past year has the pace of money growth picked up sufficiently to potentially create a serious resurgence of inflation.

Anatomy of a Perfect Storm

Central banks may set the stage for inflation, but when it comes to buying or selling gold they seem to follow the manic behavior of the public. Central banks were net sellers of gold year after year prior to 2010 (when gold prices rose from $250 to $1200 per ounce). Suddenly central banks reversed course and started buying heavily in 2011-2012 (accumulating gold at prices between $1200 and $1900 per ounce). Turning a profit must seem less urgent when you can print money legally. Now that gold prices have retreated back to the current $1200-$1300 cost of production, central banks are reducing their purchases (on track to be reduced 34% in 2013). This year it seems likely central bank selling was triggered by prior knowledge that India (the world’s largest consumer of gold) was planning to restrict gold sales to the public (central banks are not subject to insider trading rules).

It pays big hedge fund investors to have connections that give them a sense of any policy change being considered by central banks. No one should be surprised that George Soros and John Paulson dumped huge gold related positions on the market early this year when central banks started reducing their gold purchases. Gold plummeted to prices that attracted retail gold buyers in India (and motivated us to start buying gold mining shares). Record levels of gold buying in India triggered a short-lived rebound in gold prices. The buying ended, and price dropped further when the Indian Central Bank effectively barred gold imports. Who would have guessed??

Of course the mania of gold buying a few years back wasn’t lost on the management of gold miners at a time they could borrow money cheaply. They borrowed money and began acquiring and expanding mines that appeared profitable at record gold prices a couple of years back. As that production came on line, gold prices fell. Mining management may leave a lot to be desired, but they are not complete idiots. Most major miners still kept a lot of that cash handy for emergencies (unlike the banks in 2009). That’s why despite the plunge in both metals prices and profitability we don’t see headlines about mining companies going bankrupt. The better run companies have already managed to slash their cost of production and over the next year many of the high cost mines will be closed, slashing global gold production. In the short-term the miners are their own worst enemy. Their attempts to maintain profitability with record gold production in 2013 are in large part a reason gold prices are so low. Going forward, reduction of gold production and a stable cost structure with the industry bode well for profitablility.

In the very short-term, the combination of soaring broad stock prices and plummeting gold stock prices has created additional downward pressures for tax reasons as we approach year-end. Investors with substantial taxable profits are looking to offset them by taking tax losses on their gold related positions. The wash sale rule prevents them from buying those positions back until after 30 days. Barring some unrelated development, tax related selling is likely to maintain downward pressure on metals and mining prices through year-end.

As of now gold prices have retreated to between $1200 and $1300 per ounce (the perceived current average global cost of production) and forecasts of even lower prices feed the rumor mills. Miners are insuring their own survival and protecting profits by scheduling closure of high cost mines, restructuring operations and other costs, and selling lots of gold. One of the largest mining companies, Barrick Gold Corporation, recently issues shares to pay down some of their debt. The current moves are expensive and untimely, but Barrick claims to have reduced their own costs to around $900/oz (Disclosure: We own Barrick (NYSE:ABX) in personal and client accounts).

Despite these short-term negatives that have depressed stock prices in the mining sector, many positives still emerge. The most obvious being that the markets are focused on all these negatives and they are already reflected in the prices of the miners. Although some future industry consolidation seems likely, no one is talking about bankruptcies. Low gold prices are driving record consumption. Despite the restrictions in India that have raised gold prices 25% above world market prices, consumption remains high. Chinese gold imports are at record levels. Even after a substantial monthly decline, gold purchases were over 60% higher than a year ago. Recent gold consumption exceeds production but gold sales by ETFs like GLD and central banks have created a temporary glut on the world market. Closure of high cost mines will reduce future production that will almost certainly create a shortage at these consumption levels. Ultimately all those fundamentals are positive at current depressed prices, but not the big payoff.

A big payoff is likely to come for the depressed gold sector when the stock market gets its next major setback. Additionally and possibly the most important factor of all is that inflation is poised to rise, just when the markets have become convinced it has been banished forever.

As Baron Rothchild admonished investors centuries ago, “Buy when the blood is running in the streets”. In 2009 blood was running on Wall St. It was a great time to buy and we did. A year or two ago, blood was running in a housing market still flooded with foreclosures and short sales. It was a great time to buy and I advised in this newsletter to do so. Now blood is running in the mining sector. We may still be a few months away from the end of this crisis, but buying these stocks could just turn out to be a “Gold Mine.”

Clyde Kendzierski

Chief Investment Officer

Unless otherwise indicated, investment opinions expressed in this newsletter are based on the analysis of Clyde Kendzierski, Managing Director and Chief Investment Officer of Financial Solutions Group LLC, an investment adviser registered with the California Department of Corporations. The opinions expressed in this newsletter may change without notice due to volatile market conditions. This commentary may contain forward-looking statements and FSG offers no guarantees as to the accuracy of these statements. The information and statistical data contained herein have been obtained from sources believed to be reliable but in no way are guaranteed by FSG as to accuracy or completeness. FSG does not offer any guarantee or warranty of any kind with regard to the information contained herein. FSG and the author believe the information in this commentary to be accurate and reliable, however, inaccuracies may occur.

Investors should consider the charges, risks, expenses, and their personal investment objectives before investing. Please see FSG’s ADV Part 2A containing this and other information. Read it carefully before you invest.

Past performance is a poor indicator of specific future returns. It, however, may be useful in your evaluation of how FSG performs in different market environments. Investors have the ability to achieve results similar to benchmark indices by investing in an index fund or Index-tracking ETF, typically with lower fees.

Past performance of any security is not a guarantee of future performance. There is no guarantee that any investment strategy will work under all market conditions.

There is no guarantee that the investments mentioned in this commentary will be in each client's portfolio.

This material is intended only for clients and prospective clients of the FSG.It has been prepared solely for informational purposes and is not an offer to buy or sell or a solicitation of any offer to buy or sell any security or other financial instrument, or to participate in any trading strategy.

S&P 500 Index is an unmanaged, market value-weighted index of 500 stocks generally representative of the broad stock market.

This material does not provide individually tailored investment advice. It has been prepared without regard to the individual financial circumstances and objectives of persons who receive it. The strategies and/or investments discussed in this material may not be suitable for all investors. No mention of any security or strategy should be taken as personalized investment advice or a specific buy or sell recommendation. Please contact FSG to discuss your specific financial situation and suitability.

It is always the intention of FSG to minimize any negative effect on clients. Our success in that effort, however, is subject to unanticipated market conditions. Consequently, past performance does not guarantee future returns

Copyright © 2013, Financial Solutions Group LLC. ALL RIGHTS RESERVED. FSG is not liable for any actions taken in reliance on information contained herein.

www.financial-solutions-group.com