Looking Back 40 Years, What Can We Learn About This Current Corporate Debt Market?

I recently wrote a blog post detailing the potential opportunity in municipals as it has historically rebounded after a negative total return. Accordingly, I have been asked if this pattern was representative in the investment grade corporate arena.

Before I detail the results, and as with the analysis on the municipal arena, there are some caveats to extrapolating these past results for future results. First, of the 40 years of data available, only 10 years of that data was during a secular bear market while the remaining 30+ years occurred during a secular bull market. This is not a small variable; however, it does provide us with where potential movements may be headed even in regard to the current market. Perhaps the biggest contingency to take into consideration is coupon, which is the largest component of return over the long haul when investing in fixed income. In fact, the coupon for the investment grade corporate index was 6.46% in 1973, while it is 4.64% currently. The all-time high on the index measured annually was 9.66% in 1985, while the current reading is the all-time low. This simple fact alone should dictate that even if history were to repeat itself, it may do so in direction and not magnitude.

As Mark Twain said, “history doesn’t repeat itself, but it does rhyme.”

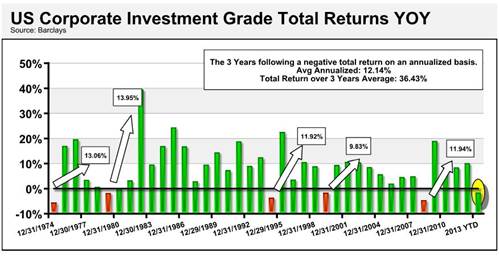

As you can see, the three years following a negative total return in the Barclays US Aggregate Investment Grade index has some startling results. The average annualized return following a negative total return in a calendar year has averaged 12.14% or a total return over the same time frame of 36.43%.

While it may be hard to take the leap of faith of moving into the debt markets considering the immense amount of headline risk, Federal Reserve tapering risk, interest rate risk and credit risk, we should also remember the classic mantra of the markets: buy low sell high. One way to begin to narrow down the possible opportunities to do this is to look at areas that have already been oversold or in which institutional investors may have already moved out. According to the Global Fund Manager survey from Merrill Lynch, energy, commodities, bonds and emerging markets are the most under-owned asset classes.

Though it would be difficult to call for any similar returns to the five events measured over the last 40 years, it still should be something that investors keep in mind as the look for rebalancing portfolios and to balance out the component of multiple contingencies within portfolios.

This commentary is for informational purposes only. All investments are subject to risk and past performance is no guarantee of future results. Please see the disclosures webpage for additional risk information. For additional commentary or financial resources, please visit www.aamlive.com/blog.

© Advisors Asset Management