“Good news is good again.”

It would be hard to attribute that statement to any one media source or Wall Street analyst, since the sentiment was rampant on Friday after the release of the better-than-expected Nonfarm Payrolls Report. The seasonally adjusted gain of 203,000 jobs in November versus an expectation of around 185,000, and the resultant dip in the unemployment rate to 7.0%, generated a Friday market rally few observers anticipated.

Why? The answer is obvious. Market pundits have come to love the “good news is bad news” (and vice versa) mantra adopted for close to a year as it pertains to increasing or decreasing the chances of the Federal Reserve scaling back on bond purchases. They were more than a bit surprised by the ferocity of Friday’s market rally, the biggest one-day gain in several weeks, with the Dow posting a 1.3% move higher. This came on the heels of an unusual losing streak for 2013 – five straight down days for the Dow and S&P.

Friday’s market gains were not quite enough to continue an impressive eight-week winning streak for the DJI and SPX, as they fell 0.4% and 0.1%, respectively, on the week. The NASDAQ managed to put in a very modest weekly gain of 0.1%.

There were a few cynics still out there, however (this author included), who think there may have been some other factors at work on Friday other than pure optimism over the positive jobs data. Let’s look at some of the evidence, starting with the five-day pullback coming into Friday which saw the S&P drop over 30 points from peak to trough, or just about 2%.

Now this may have just been a case of the market working off an overbought condition, as new all-time market highs were being set almost on a daily basis for the Dow and S&P. Nevertheless this relatively small but sharp selloff came in the face of a raft of positive economic reports prior to Friday which handily beat consensus: ISM manufacturing, construction spending, auto sales, ADP employment, GDP, factory orders, October new home sales and jobless claims.

Yes, there were a few misses thrown in during the week, including the ISM non-manufacturing report, but by and large it was a strong streak of positive economic data, which was met with either market indifference or some modest selling. One of the strongest positive market moves of the week, in fact, came shortly after the release of the weaker-than-expected ISM non-manufacturing data, as the “bad news is good” theme continued to hold form and the Dow rallied 80+ points off Wednesday’s early lows.

So, what changed Friday to have ostensibly good news actually being treated as good news? Yes, the jobs report was accompanied by the surprisingly positive University of Michigan consumer sentiment data, but this came out well after the jobs report had set the uptrend for the day.

Those cynics are pointing to the overall employment situation, which continues to show little improvement in the status of the long-term unemployed and the labor force participation rate. And this can rather easily be tied to statements in the past from Janet Yellen, who will be taking over the reins of the Federal Reserve upon Ben Bernanke’s departure in January 2014. Yellen has taken great pains to express the point of view that she is far less concerned with headline jobs and employment numbers than truly seeing some improvement in what is increasingly becoming viewed as “structural” employment issues plaguing rather large segments of the population.

Let’s pull out just two statements from the Bureau of Labor Statistics’ press release issued on Friday:

“The number of long-term unemployed (those jobless for 27 weeks or more) was essentially unchanged at 4.1 million in November. These individuals accounted for 37.3 percent of the unemployed.”

“The civilian labor force rose by 455,000 in November, after declining by 720,000 in October. The labor force participation rate changed little (63.0 percent) in November.”

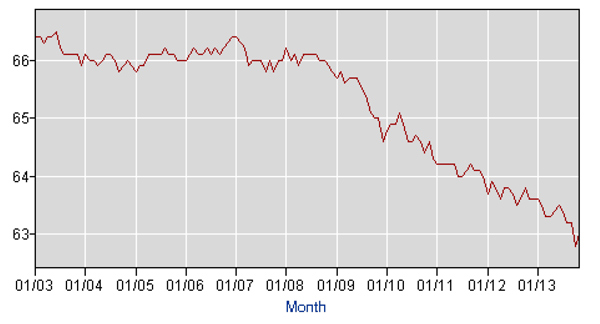

Source: Bureau of Labor Statistics, December, 2013 Labor Force Participation Rate: Adults Age 16+

So, the labor force participation rate remains at essentially a 35-year low. And despite the lowest unemployment rate in the five years since this weak labor market recovery began, it is estimated by most economists that it will still take four to six years to reach pre-recession employment levels at the current rate of job creation.

This is good news? No, frankly, it is not. And it serves to support the point of view that while some symbolic tapering may occur sometime over the next three Fed meetings, under the Yellen Fed, indeed, tapering will likely not mean real interest rate tightening for quite some time to come. And, the truth of the matter is that Friday’s jobs report contained just enough good and bad news to qualify as what some are calling a “Goldilocks” report, not too strong and not too weak. This might be a better explanation of what really drove Friday’s rally.

The next big media focus will be on the odds of a “DecTaper,” which Bloomberg is handicapping at somewhere in the 30-35% range and Bill Gross of PIMCO said Friday had 50/50 odds. From where we sit, does it really matter whether a minor “taper” comes in December, January, or March? Sure, it is interesting to watch the business networks trot out guest after guest with their opinions. But when one follows an active portfolio management approach, as we do here at Flexible Plan Investments, Ltd., our focus is on managing actual market performance, not in speculation on what might happen.

So, we will leave the question of whether good news is now good for the markets to the further analysis of others. But personally, I will continue to be rooting for the “good news” of some real improvement in those structural employment issues.

All the best,

David

© Flexible Plan Investments